Client win with Nissay AM puts Triton in focus

Nissay Asset Management Corporation has selected Virtu Financial (VIRT) Triton execution management system to handle multi asset trading across global markets after running a comprehensive vendor review against other trading platforms.

The decision centers on Triton software capabilities, including support for equities, ETFs, futures, options, FX, and fixed income. It also reflects Nissay AM priorities around workflow efficiency, analytics, and integration across domestic and ex Japan trading desks.

See our latest analysis for Virtu Financial.

Virtu’s recent Nissay AM win arrives as the share price trades at US$42.52, with a 90 day share price return of 23.96% and a 3 year total shareholder return of 150.92%. This points to strong longer term momentum despite short term swings.

If you are interested in other potential opportunities around market infrastructure and trading technology themes, it is worth scanning the 35 AI infrastructure stocks

With shares at US$42.52, trading about 7% below the average analyst price target and with an estimated intrinsic discount of roughly 51%, you have to ask: is Virtu still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 297% Overvalued

According to a widely followed narrative, Virtu Financial’s fair value sits at $10.71, far below the last close of $42.52, which sets up a very different picture from many current price signals.

VIRT "stock ticker name" or better known as Vertiv Holdings. Is one of them companies, that is continually making Global Headlines. Any company let alone with a Positive Cash Flow of 302%+, is one that should be talked about. VIRT is a AI Financial Service Company. This little firm has integrated AI and algorithm trading into their system. VIRT is currently rated a Strong Buy, and honestly is at a Perfect Price for Long Term Investments. Why is this? Today after reporting a successful Earnings Report. Their shares plummeted after Bulls sold for the short Profit. This means now, it is at its new lowest bottom. This is because their report, posted a positive outcome and results showing that now it is definitely a way undervalued company. In just this year, they have climbed over 100%. Then add in them constantly making headlines, that add the votality for major runs. We are not getting paid for any of these articles. We are freelance, but when we see a good company that is honest and growing. Well make our report. You heard this from The Daily Investors.

The narrative from DailyInvestors leans on very strong cash flow, upbeat earnings commentary, and a future profit multiple that implies a much lower fair value than the current price. It hinges on specific assumptions for revenue trajectories, margins, and the cost of capital that sharply compress the implied upside most traders might infer from recent returns. Want to see exactly which profit and valuation inputs pull the fair value down so far below $42.52, and how they build to $10.71 as the anchor.

Result: Fair Value of $10.71 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story can break if revenue contraction of 10.77% persists, or if user assumptions on profit margins and a future P/E of 15.99x prove too optimistic.

Find out about the key risks to this Virtu Financial narrative.

Another angle on value: earnings multiple vs fair value signals

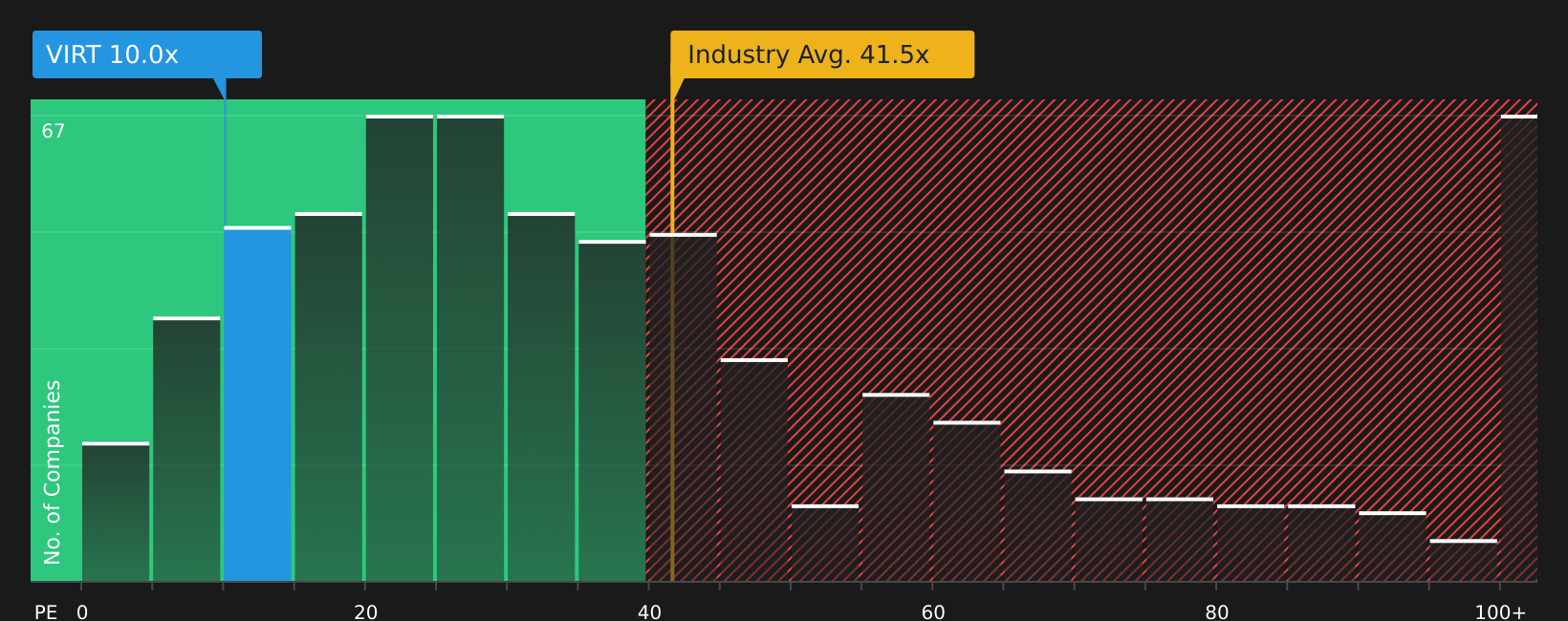

The user narrative leans on a fair value of $10.71, yet current P/E tells a very different story. At 8.4x earnings, VIRT trades well below its peer average of 19.8x, the US Capital Markets industry at 30.8x, and even below an estimated fair ratio of 15.3x. That gap suggests the market is either heavily discounting execution and forecast risks or offering a potential mispricing. Which explanation do you find more convincing?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages on value and risk here, so consider acting while sentiment is divided and test the numbers yourself with our breakdown of 5 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that fit your goals better, so use the Simply Wall Street Screener to compare options confidently.

- Spot potential bargains early by scanning screener containing 25 high quality undiscovered gems before they land on everyone else's radar.

- Prioritise resilience by checking 64 resilient stocks with low risk scores that aim to keep overall portfolio risk in check.

- Focus on dependable financial footing by reviewing companies in the solid balance sheet and fundamentals stocks screener (39 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com