- This article examines whether United Parcel Service is currently a bargain or a value trap at its recent share price by exploring what the market price might be implying about the stock.

- The shares recently closed at US$94.80, with returns of a 1.1% decline over 7 days, an 18.2% decline over 30 days, a 6.2% decline year to date, a 7.6% decline over 1 year, a 42.8% decline over 3 years, and a 31.4% decline over 5 years, which may have influenced how investors think about both opportunity and risk.

- Recent coverage has focused on United Parcel Service as a major player in global parcel delivery and logistics, with attention on how its network and operations fit into a changing e-commerce and supply chain backdrop. This context helps frame why some investors are reassessing what they are willing to pay for the stock today.

- On Simply Wall St's valuation checks, United Parcel Service currently scores 5 out of 6. The rest of this article will walk through how different valuation approaches arrive at that view and will also point to a more complete way to think about value at the end.

Find out why United Parcel Service's -7.6% return over the last year is lagging behind its peers.

Approach 1: United Parcel Service Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of future cash that a business can return to shareholders and discounts those cash flows back to today, aiming to convert a long stream of future dollars into a single present value per share.

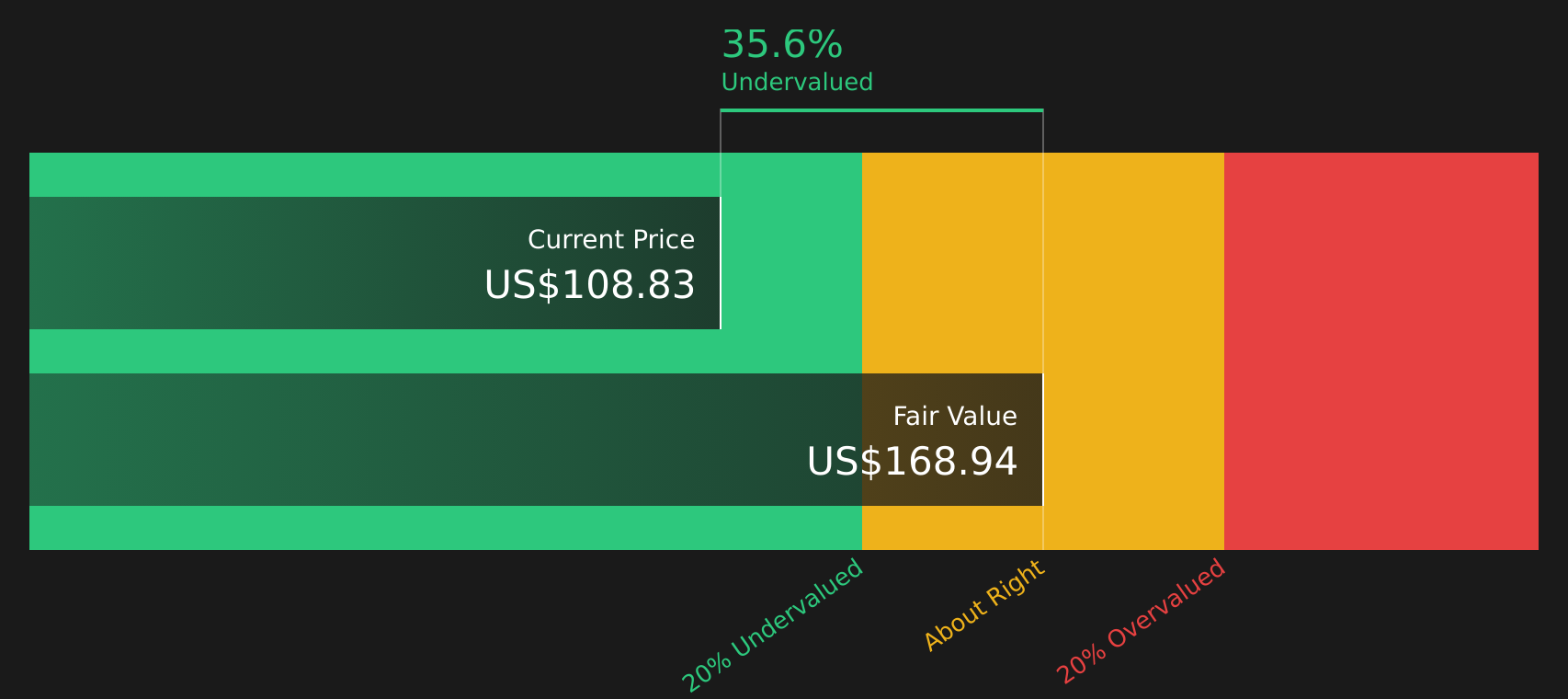

For United Parcel Service, the model used is a 2 Stage Free Cash Flow to Equity approach, based on recent free cash flow of about $4.27b. Analyst inputs and Simply Wall St extrapolations project free cash flow rising to $7.59b by 2029, with a series of annual forecasts between 2026 and 2035 that are discounted back to today to reflect risk and the time value of money. All figures here are in US$.

Putting those projected cash flows together, the DCF output suggests an intrinsic value of about $168.53 per share. Compared with the recent share price of $94.80, this implies the stock trades at a 43.7% discount to that estimated value, which points to a meaningful gap between price and this particular cash flow model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests United Parcel Service is undervalued by 43.7%. Track this in your watchlist or portfolio, or discover 62 more high quality undervalued stocks.

Approach 2: United Parcel Service Price vs Earnings

For a profitable company, the P/E ratio is a useful yardstick because it ties the share price directly to the earnings that support it. In simple terms, the higher the growth investors expect and the lower the perceived risk, the higher the P/E they are usually willing to pay as a “normal” or “fair” multiple.

United Parcel Service currently trades on a P/E of 14.46x. That sits slightly below the Logistics industry average of about 15.39x and well below the peer group average of 21.98x. On the surface, that gap might look like an opportunity, but peer and industry comparisons alone do not adjust for the company’s specific earnings profile and risk characteristics.

Simply Wall St’s Fair Ratio for United Parcel Service is 22.53x. This is a proprietary P/E estimate that reflects factors such as the company’s earnings growth profile, profit margins, risk characteristics, industry, and market capitalization. Because it blends these elements, the Fair Ratio can be more informative than a simple comparison with sector or peer averages. With the current P/E of 14.46x sitting below the Fair Ratio of 22.53x, the P/E approach points to the shares being undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your United Parcel Service Narrative

Earlier it was mentioned that there is an even better way to understand valuation, and on Simply Wall St that comes through Narratives. These let you attach a clear story about United Parcel Service to the numbers you see, so you connect your view of its revenue, earnings and margins to a forecast and then to a Fair Value that you can compare with the current price.

In practice, a Narrative is a concise explanation of what you think is really going on at the company and what that means for the future. The platform then turns that story into explicit assumptions, such as revenue growth, profit margins, discount rate and future P/E, and calculates a Fair Value that updates automatically when new earnings, news or guidance arrive.

For United Parcel Service, one investor on the Community page might build a cautious Narrative around sustainability issues, higher costs and internal headwinds and land at a Fair Value near US$84.58. Another might focus on cost efficiencies, healthcare growth and network automation and arrive closer to US$132.37. Seeing those side by side helps you decide whether the current market price looks high or low relative to the story you find more convincing.

For United Parcel Service however, here are previews of two leading United Parcel Service Narratives:

🐂 United Parcel Service Bull Case

Fair value: US$95.21

Valuation gap: about 0.4% above the recent US$94.80 share price

Revenue growth assumption: 1.75%

- Focuses on the "Efficiency Reimagined" program, including facility closures, automation and shifting volume away from Amazon to reshape the network and cost base.

- Highlights a heavier use of long term debt and cost cuts, alongside new products and partnerships, as tools to manage near term financial pressure.

- Flags labor and governance tensions and softer recent profitability, while still seeing room for higher margins and earnings if the overhaul delivers on management’s goals.

🐻 United Parcel Service Bear Case

Fair value: US$84.58

Valuation gap: about 10.8% below the recent US$94.80 share price

Revenue growth assumption: 0.61%

- Points to trade policy uncertainty, nearshoring and e commerce competition as headwinds for parcel volumes, pricing power and international profitability.

- Emphasizes higher costs tied to sustainability requirements, automation investments and a unionized workforce as constraints on margins and earnings.

- Frames the share price as rich relative to a cautious earnings path, unless revenue, margins and the assumed 18.0x future P/E all hold up against these pressures.

Do you think there's more to the story for United Parcel Service? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com