Why Advanced Drainage Systems Stock Is Drawing Attention Now

Advanced Drainage Systems (WMS) is drawing fresh attention after a recent pullback, with the stock showing a 22% decline over the past month and an 11% decline over the past 3 months.

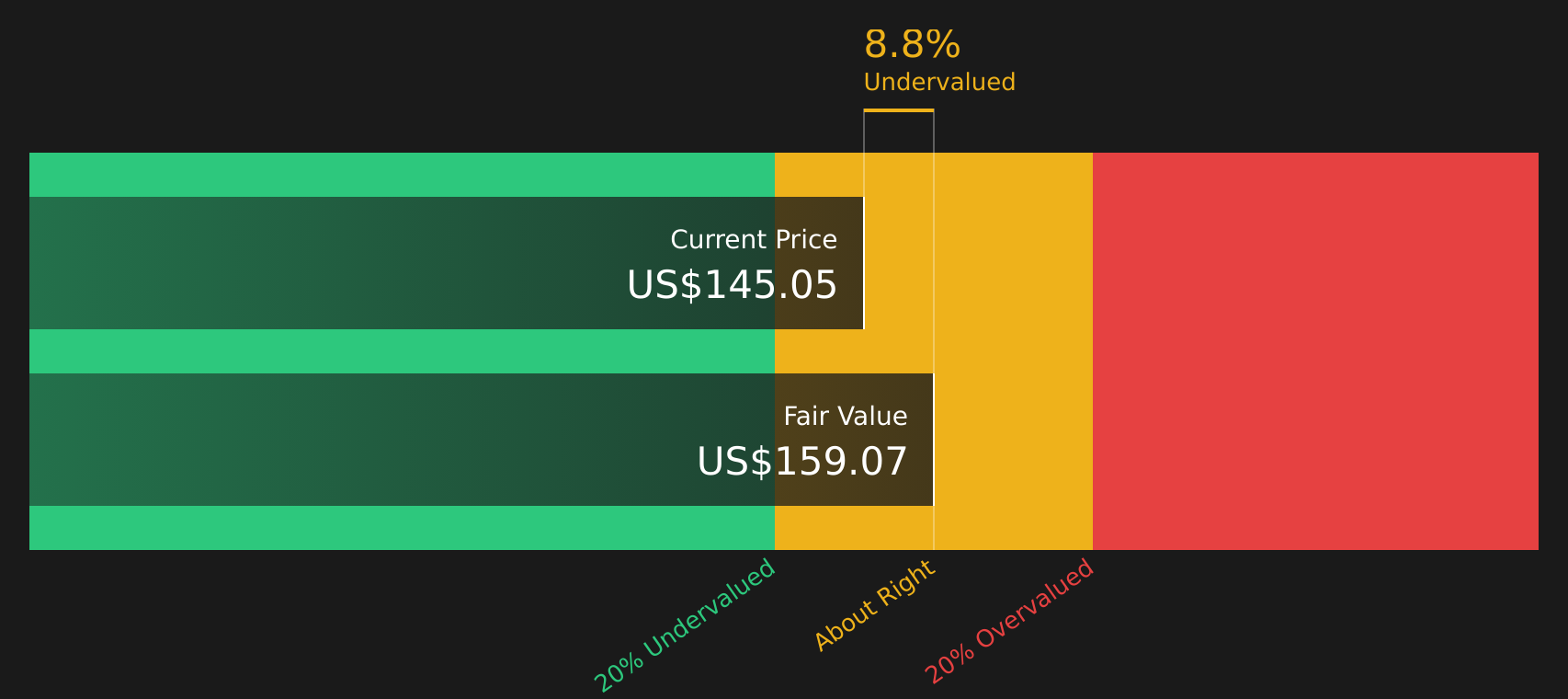

See our latest analysis for Advanced Drainage Systems.

The recent 22% one-month share price pullback has followed a much stronger period, with the 1-year total shareholder return of 23.26% and 3-year total shareholder return of 59.83% still indicating earlier momentum that has cooled in the short term.

If you are weighing Advanced Drainage Systems against other opportunities, this could be a good moment to scan the market using a focused screener for infrastructure related plays such as 26 power grid technology and infrastructure stocks

So, with the share price pulling back while 1 year and 3 year returns remain positive and the stock trading below the average analyst price target, is this a fresh entry point, or is the market already pricing in future growth?

Most Popular Narrative: 32.7% Undervalued

At a last close of $132.70 versus a narrative fair value of $197.20, the current price sits well below what the most followed model suggests.

Continuous expansion of the Allied Products and Infiltrator segments, both of which command higher margins and are growing faster than the core Pipe business, is shifting product mix toward higher profitability, resulting in improved EBITDA margins and long-term earnings power.

Curious what earnings path, margin profile, and future P/E this narrative is leaning on. The assumptions are punchy, tightly argued, and far from conservative.

Result: Fair Value of $197.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on steady construction demand and favorable resin costs; any prolonged softness or material inflation would quickly test those optimistic earnings and P/E assumptions.

Find out about the key risks to this Advanced Drainage Systems narrative.

Another Angle on Value: Cash Flows Paint a Different Picture

While the analyst based fair value of $197.20 suggests upside, the Simply Wall St DCF model points the other way, with an estimate of $111.66. On that view, the recent $132.70 price looks rich, not cheap. Which set of assumptions feels more realistic to you?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Advanced Drainage Systems for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 61 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of cautious assumptions and earlier momentum might leave you undecided. Move quickly, review the underlying data, and weigh the 3 key rewards.

Looking for more investment ideas?

If you stop with just one stock, you risk missing out on other opportunities that might fit your goals even better, so keep your watchlist working for you.

- Target potential bargains by scanning companies that combine quality fundamentals with attractive pricing using the 61 high quality undervalued stocks.

- Focus on resilience by checking out stocks that pair lower risk profiles with steadier characteristics via the 67 resilient stocks with low risk scores.

- Hunt for underfollowed names by reviewing a screener containing 26 high quality undiscovered gems that may not yet be on most investors' radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com