- Earlier this week, Hartford Insurance Group reported a very strong quarter, with revenue rising 6.7% year on year and results significantly ahead of analyst expectations compared with peers.

- What stands out is that Hartford delivered the biggest analyst estimate beat among its sector group, underscoring how its recent performance contrasts with many competitors.

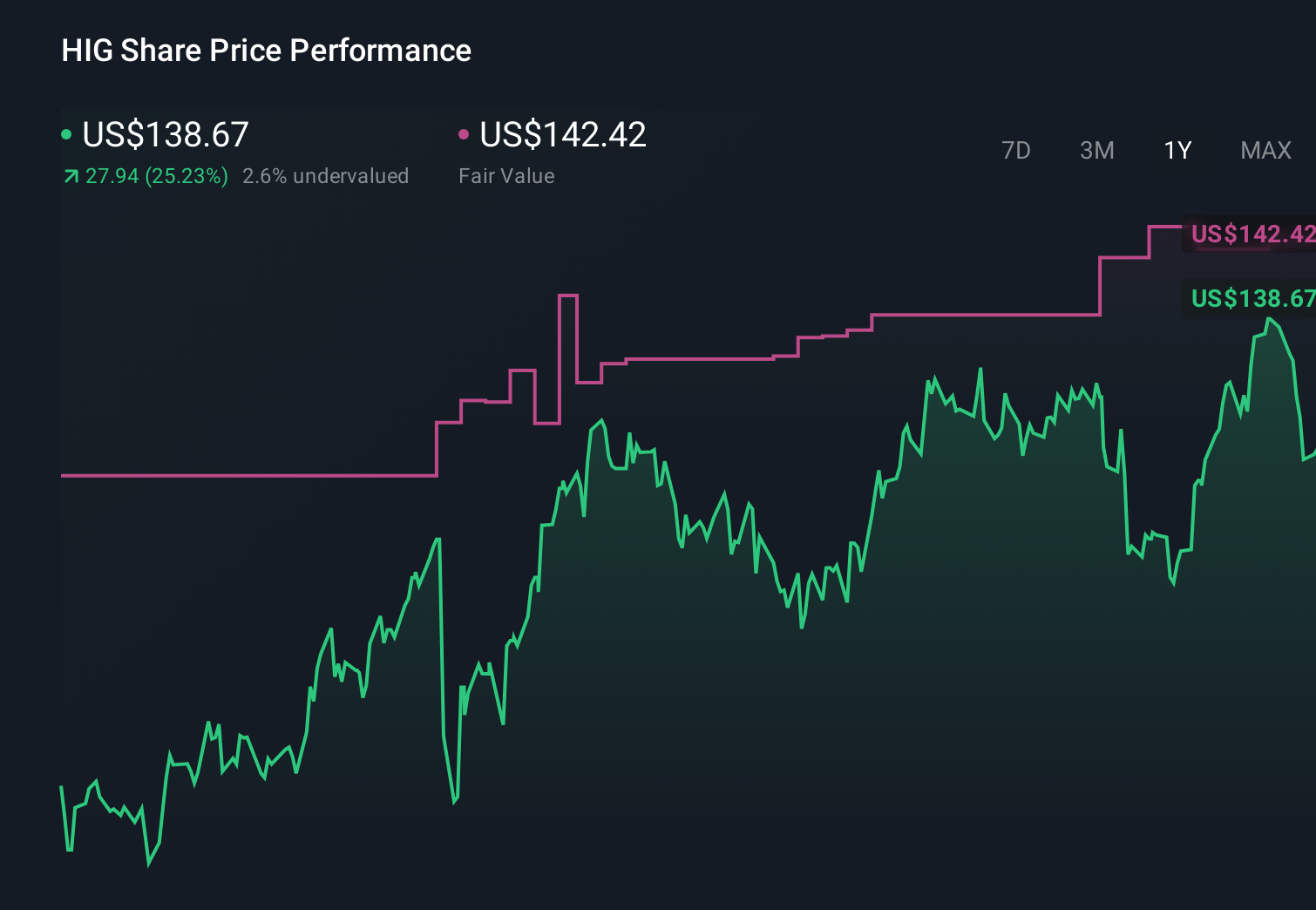

- Now we’ll explore how this strong revenue growth and earnings beat may influence Hartford’s existing investment narrative and key assumptions.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Hartford Insurance Group Investment Narrative Recap

To own Hartford, you generally need to believe it can keep pairing disciplined underwriting with technology driven efficiency, while managing catastrophe and regulatory risks. The latest 6.7% revenue increase and sector leading earnings beat reinforce the near term catalyst around pricing and margin strength, but they do not remove the biggest current risk that a single severe catastrophe season or regulatory setback could quickly pressure earnings.

The recent opening of Hartford’s new technology hub in Columbus, Ohio, with about 75 AI and cloud focused employees, ties directly into this quarter’s outperformance by supporting the catalyst of better underwriting, claims handling and cost control. If these investments continue to support efficiency and pricing execution, they may help offset some of the pressure from competitive markets and evolving regulatory demands.

But while recent results were strong, investors should still pay close attention to the risk that elevated catastrophe losses could...

Read the full narrative on Hartford Insurance Group (it's free!)

Hartford Insurance Group's narrative projects $32.5 billion revenue and $4.1 billion earnings by 2029. This requires 4.6% yearly revenue growth and about a $0.3 billion earnings increase from $3.8 billion today.

Uncover how Hartford Insurance Group's forecasts yield a $150.85 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently place Hartford’s fair value between US$136 and about US$333.70, reflecting very different views on its potential. Against that backdrop, Hartford’s recent earnings beat puts extra focus on whether its underwriting and pricing discipline can keep offsetting catastrophe and regulatory risks, so it is worth comparing several of these perspectives before deciding how the story fits into your own expectations.

Explore 5 other fair value estimates on Hartford Insurance Group - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hartford Insurance Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Hartford Insurance Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hartford Insurance Group's overall financial health at a glance.

No Opportunity In Hartford Insurance Group?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 26 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com