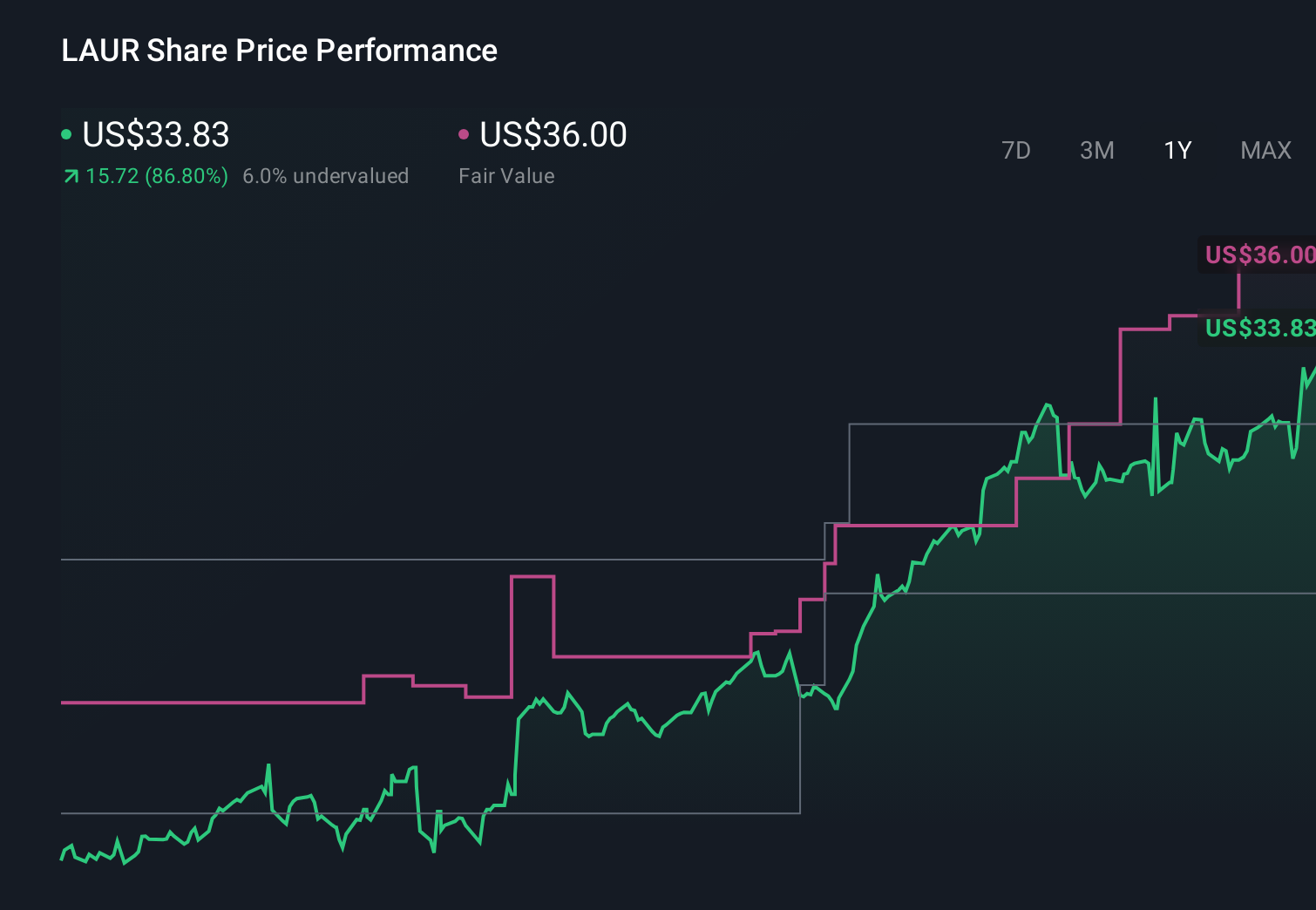

- Laureate Education recently reported a strong quarter, with revenue and EPS ahead of analyst expectations, continued investment in new campuses and digital and AI capabilities, and over US$200 million returned to shareholders via share repurchases, while CFO Richard M. Buskirk sold 61,803 shares but retained the majority of his stake.

- Despite delivering the fastest revenue growth among peers and emphasizing ongoing business momentum, Laureate Education issued the weakest full-year guidance update in its group, raising questions about how its growth investments and capital returns balance against its outlook.

- We’ll now examine how the earnings beat, alongside significant share repurchases, might influence Laureate Education’s existing investment narrative and risk profile.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Laureate Education Investment Narrative Recap

To own Laureate Education, you need to believe its campus expansion and digital and AI investments in Mexico and Peru can keep paying off while country risk, FX swings, and enrollment mix shifts stay manageable. The latest earnings beat and sizable buybacks support that thesis, but the relatively cautious full year guidance makes near term execution on new campuses and enrollment the key catalyst, and heightens focus on the risk that growth spending does not translate into the expected returns.

The expanded US$400 million share repurchase authorization, alongside over US$200 million already deployed, is central here. It tightens the link between cash generation and shareholder returns at a time when guidance is the weakest in its peer group. For investors, that combination puts extra weight on upcoming enrollment trends in Mexico and Peru, and on how much earnings resilience Laureate can sustain if tuition mix or FX moves start to work against it.

Yet beneath the strong recent quarter, investors also need to watch the risk that heavy campus investment meets softer than expected enrollment or pricing power in...

Read the full narrative on Laureate Education (it's free!)

Laureate Education's narrative projects $2.0 billion revenue and $343.9 million earnings by 2028. This requires 8.4% yearly revenue growth and about a $89.7 million earnings increase from $254.2 million today.

Uncover how Laureate Education's forecasts yield a $39.58 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue near US$1.9 billion and earnings above US$330 million by 2028, which contrasts sharply with today’s cautious guidance and suggests their thesis of faster digital growth and margin expansion may need to be revisited in light of the latest results.

Explore 4 other fair value estimates on Laureate Education - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Laureate Education research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Laureate Education research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Laureate Education's overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com