Ituran Location and Control (ITRN) saw movement in recent trading, with the share price closing at US$50.95. Investors are weighing its recent returns and its core telematics business mix across services and products.

See our latest analysis for Ituran Location and Control.

That 1 day share price return of 2.38% and 7 day share price return of 1.11% sit against a 30 day share price return of 6.15% and a 90 day share price return of 17.45%, while the 1 year total shareholder return of 43.79% and 3 year total shareholder return of 176.36% point to momentum that has built over time rather than just in recent sessions.

If this kind of performance has you thinking about what else is moving, it could be a good moment to broaden your search with the 20 top founder-led companies

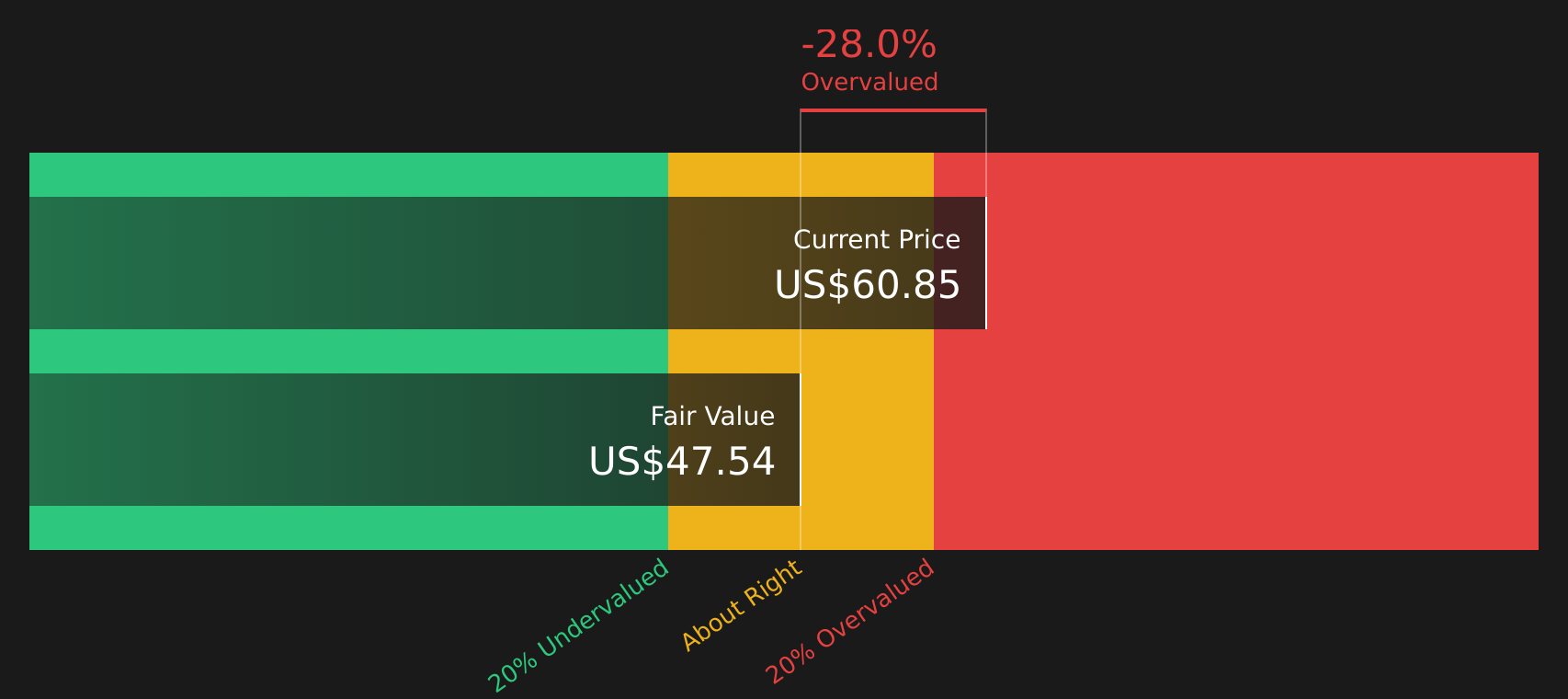

With Ituran Location and Control trading at US$50.95 and sitting roughly 19% below the current analyst price target, the key question is whether the stock still offers upside or if the market is already pricing in future growth.

Most Popular Narrative: 16% Undervalued

At a last close of $50.95 against a narrative fair value of about $60.67, the current pricing sits below what the most followed narrative suggests is reasonable, with that view built on recurring telematics demand, earnings quality and updated analyst work.

Bullish analysts see an expanding total addressable market for telematics and stolen vehicle recovery services, which they view as supportive of higher fair value assumptions over time.

They highlight recurring revenue potential from subscription like services as a key pillar for earnings quality and visibility, which they see as helpful for justifying higher valuation multiples.

Curious what sits behind a higher fair value and richer earnings multiple, yet still points to undervaluation? The narrative leans on specific growth rates, margin assumptions and a tighter discount rate story that are only clear when viewed together.

Result: Fair Value of $60.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can change quickly if subscriber growth falls short of projections or if lower margin OEM contracts have a greater impact on overall profitability.

Find out about the key risks to this Ituran Location and Control narrative.

Another Way To Look At Value

While the narrative fair value points to upside, the SWS DCF model tells a cooler story. Ituran Location and Control at US$50.95 is sitting slightly above its estimated future cash flow value of about US$50.71, which raises the question of how much margin of safety you really have here.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ituran Location and Control for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 61 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing both upside arguments and caution flags in this story, it makes sense to check the numbers yourself and move quickly to form your own view with the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

Once you have formed a view on Ituran Location and Control, do not stop there. Broad, thoughtful idea sourcing can make a real difference over time.

- Target steady compounders by reviewing companies in the 61 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect their strengths.

- Protect your downside first by scanning the 69 resilient stocks with low risk scores for businesses that score well on balance sheet strength and risk checks.

- Get ahead of the crowd by checking the screener containing 25 high quality undiscovered gems where smaller, under followed companies with solid metrics might be waiting for attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com