Kinsale Capital Group (KNSL) is drawing fresh attention after its focus on hard to place, high risk insurance produced 21.2% annual net premium expansion over two years and 43.9% yearly earnings per share growth.

See our latest analysis for Kinsale Capital Group.

The recent focus on hard to place, high risk policies comes after a tougher period for investors. A 1 year total shareholder return of 30.99% decline contrasts with a 5 year total shareholder return of 101.83%, which still points to meaningful longer term gains.

If this shift in sentiment has you thinking about where else growth and risk are being priced, it could be worth scanning 20 top founder-led companies for fresh ideas beyond the usual names.

With Kinsale trading at US$335.28, and sitting on an implied 21% gap to analyst targets and a 40% intrinsic discount estimate, are you looking at an undervalued specialist insurer, or is the market already baking in its future growth?

Most Popular Narrative: 18% Undervalued

At a last close of $335.28 against a narrative fair value of about $407.33, the current price sits below what the consensus model implies. This puts the spotlight on how analysts see growth, margins and risk playing out from here.

The analysts have a consensus price target of $407.33 for Kinsale Capital Group based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $450.0, and the most bearish reporting a price target of just $312.0.

Curious what sits behind that valuation gap? Revenue growth assumptions, margin compression and a richer future earnings multiple all feed into this fair value story. The exact mix of these inputs, and how they compound over time, is where the narrative really gets interesting.

Result: Fair Value of $407.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that gap can close quickly if competition in commercial property and catastrophe-exposed homeowners continues to pressure premiums and leaves losses running hotter than pricing.

Find out about the key risks to this Kinsale Capital Group narrative.

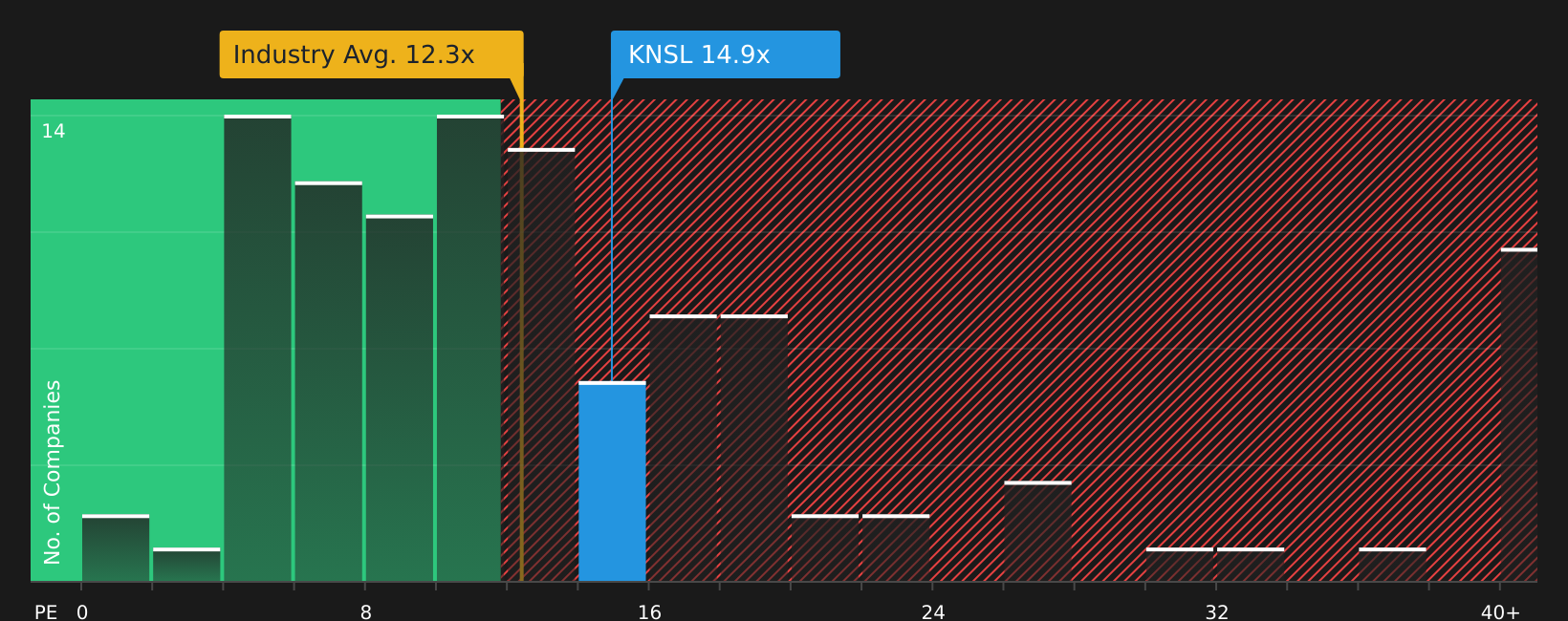

Another View: What The P/E Says

While the SWS DCF model sees Kinsale trading about 39.5% below its estimated fair value, the P/E picture is less generous. At 15.4x earnings, the stock sits well above both the US Insurance industry average of 10.9x and peer average of 8x, compared with a fair ratio of 11.7x that the market could move toward. That sort of premium can either shrink quietly over time or correct quickly, so which outcome do you think the current price is setting you up for?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

After all this, are you leaning bullish or cautious on Kinsale? The key is to move quickly, check the numbers yourself, and weigh the 3 key rewards.

Looking for more investment ideas?

If Kinsale has sharpened your focus, do not stop here. Broaden your watchlist with other high conviction ideas that fit your risk and return preferences.

- Target quality first by scanning companies with strong fundamentals through the solid balance sheet and fundamentals stocks screener (39 results).

- Spot potential value gaps by reviewing the 61 high quality undervalued stocks before prices adjust.

- Build a steadier income stream by weighing opportunities in the 12 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com