In the last week, the United States market has remained flat, though it has risen by 16% over the past year with earnings expected to grow annually at the same rate. In this environment, identifying stocks with strong fundamentals and growth potential can offer investors opportunities to uncover hidden treasures in a dynamic market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Morris State Bancshares | 1.94% | 4.43% | 2.90% | ★★★★★★ |

| Security Federal | 17.59% | 5.51% | 0.13% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Union Bankshares | 374.44% | 1.11% | -7.71% | ★★★★★☆ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Pure Cycle | 5.42% | 9.36% | -2.03% | ★★★★★☆ |

Here we highlight a subset of our preferred stocks from the screener.

Liquidity Services (LQDT)

Simply Wall St Value Rating: ★★★★★★

Overview: Liquidity Services, Inc. operates as a provider of e-commerce marketplaces and auction listing tools with a market capitalization of approximately $933.21 million.

Operations: Liquidity Services generates revenue primarily from its Retail Supply Chain Group (RSCG) at $324.61 million, followed by GovDeals at $89.15 million, and the Capital Assets Group (CAG) at $40.93 million. The Machinio & Software Solutions segment contributes $20.93 million to the total revenue.

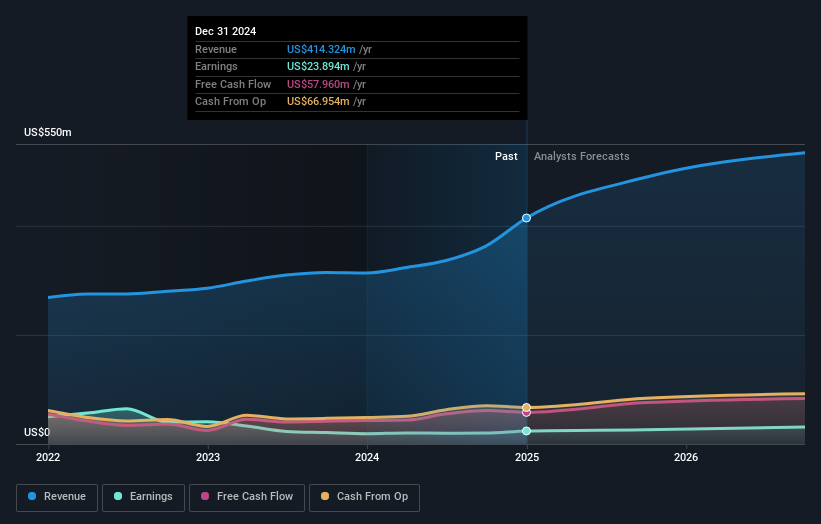

Liquidity Services, a nimble player in the commercial services sector, has demonstrated robust performance with earnings growth of 24.6% over the past year, outpacing the industry average of 10.9%. The company is debt-free and boasts high-quality earnings, contributing to its perceived value at 57.5% below estimated fair value. Despite a dip in sales from US$82.82 million to US$77.35 million year-over-year for Q1 2026, net income rose from US$5.81 million to US$7.49 million, with diluted EPS climbing from $0.18 to $0.23, indicating solid profitability amidst strategic board changes and no recent share buybacks.

- Unlock comprehensive insights into our analysis of Liquidity Services stock in this health report.

Examine Liquidity Services' past performance report to understand how it has performed in the past.

Global Industrial (GIC)

Simply Wall St Value Rating: ★★★★★★

Overview: Global Industrial Company operates as an industrial distributor of various MRO products in the United States and Canada, with a market capitalization of approximately $1.21 billion.

Operations: Global Industrial generates revenue primarily through its Industrial Products Group, which reported $1.38 billion in sales. The company's market capitalization stands at approximately $1.21 billion.

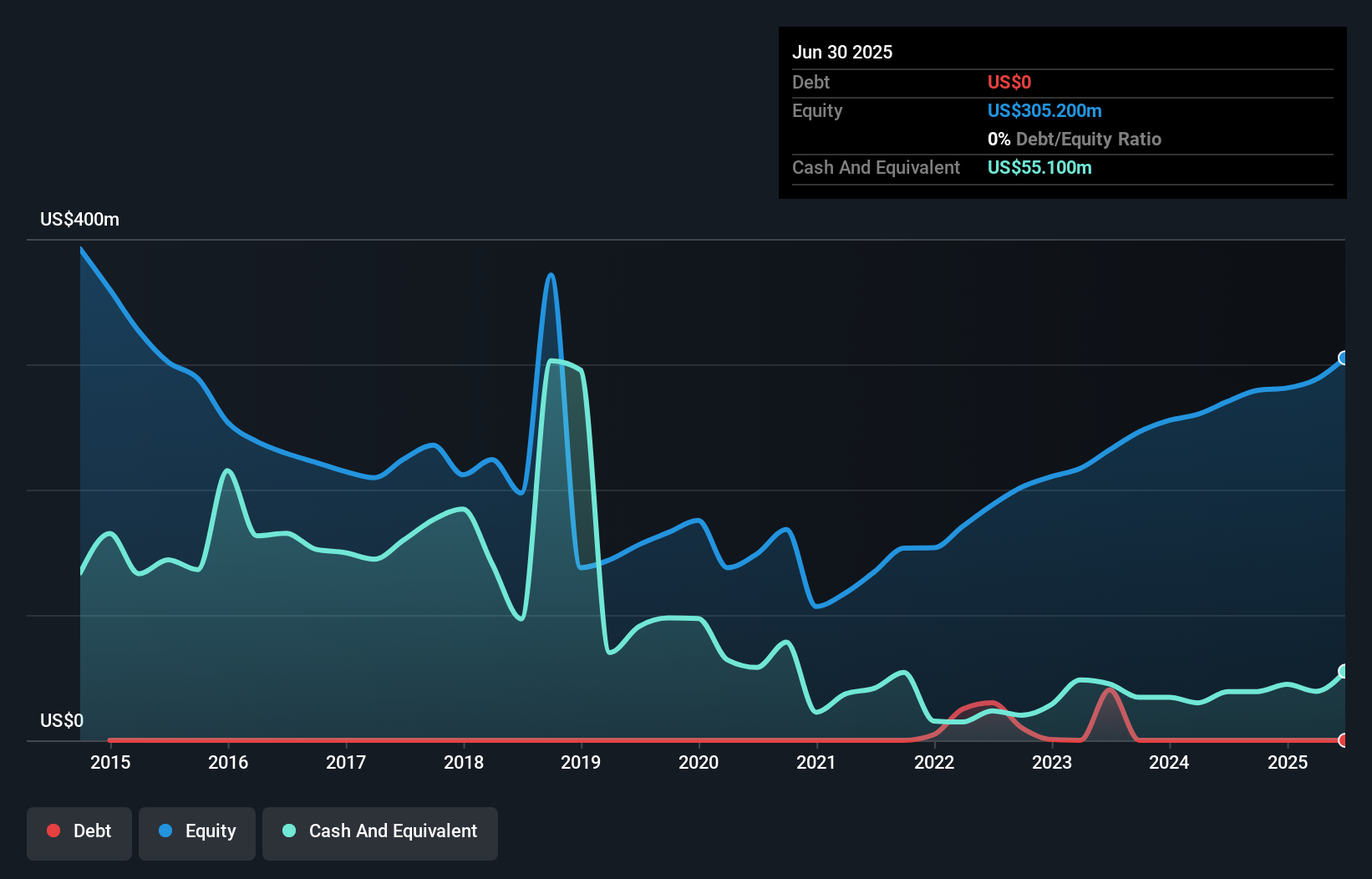

Global Industrial, a nimble player in the trade distributors sector, is capturing attention with its robust financial health and strategic initiatives. With zero debt and a free cash flow of US$124.7 million as of September 2023, it stands on solid ground financially. The company recently reported a net income increase to US$72.1 million for 2025 from US$61 million the previous year, alongside an earnings per share rise to US$1.85 from US$1.57. As it enhances customer relationships and expands product offerings in MRO supplies, Global Industrial is poised for growth but must navigate rising costs and potential economic headwinds.

Bristow Group (VTOL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Bristow Group Inc. offers vertical flight solutions to offshore energy companies and government agencies across several countries, with a market capitalization of approximately $1.33 billion.

Operations: The company generates revenue primarily from offshore energy services, accounting for $990.48 million, followed by government services at $379.44 million. Gross profit margin is a key financial metric to consider when evaluating its performance.

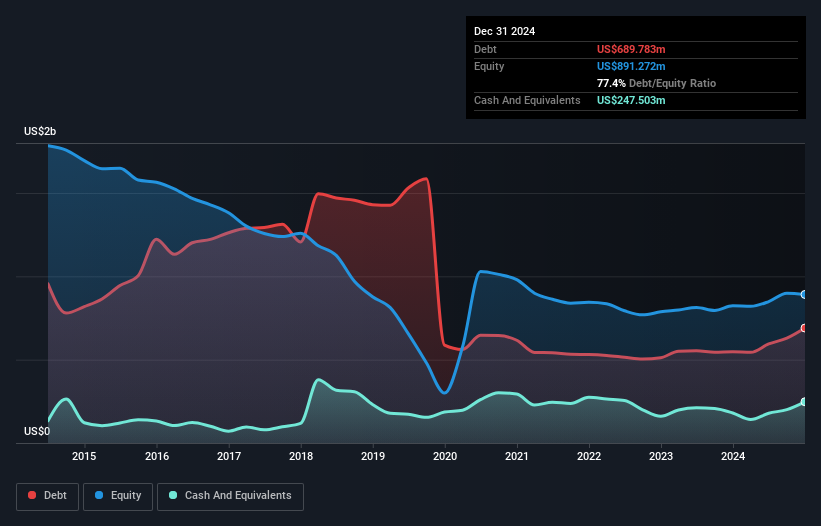

Bristow Group, a notable player in the aviation sector, has shown impressive financial performance with earnings growing 36.2% over the past year, significantly outpacing the Energy Services industry's negative growth of 33.1%. The company's interest payments are well covered by EBIT at a ratio of 5.1x, indicating solid financial health. With net income reaching US$129 million for the full year ending December 2025 and basic earnings per share rising to US$4.47 from US$3.32, Bristow demonstrates robust profitability. Despite insider selling in recent months, its strategic expansion into new markets and investment in next-gen aircraft technology position it favorably for future growth prospects.

Make It Happen

- Navigate through the entire inventory of 321 US Undiscovered Gems With Strong Fundamentals here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com