Cadence Design Systems (CDNS) extended its collaboration with NVIDIA, integrating NVIDIA’s accelerated computing stack more deeply into Cadence’s AI driven design and agentic AI tools across semiconductor, automotive, aerospace, energy and life sciences workflows.

See our latest analysis for Cadence Design Systems.

The latest collaboration news lands after a softer share price patch, with the 90-day share price return of 10.52% and year to date decline of 8.40% contrasting with a 1-year total shareholder return of 5.65%, and a 5-year total shareholder return of 117.25% that points to stronger long run compounding.

If Cadence’s AI push has your attention, it can be useful to see what else is shaping the theme. You can start with 65 profitable AI stocks that aren't just burning cash

With the shares down over the past quarter despite an expanded NVIDIA partnership and ongoing AI ambitions, the key question for investors is whether Cadence is on sale today or if the market already prices in future growth.

Most Popular Narrative: 17.5% Undervalued

Cadence’s most followed narrative assigns a fair value of $344.64 per share, which sits above the last close of $284.32 and frames the recent pullback as an entry point according to TibiT.

My financial model (2024A to 2030E) identifies a critical shift in the company's financial profile. While historical revenue growth clocked in at ~14% CAGR, I am modeling a more conservative 10 to 12% revenue growth going forward. However, the investment case relies on a massive expansion in profitability.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue pace and profit margins are baked into that fair value, and how they tie into a premium future earnings multiple? The full narrative lays out a step by step financial roadmap that links growth, margins and valuation into one cohesive story, so you can see exactly what needs to go right.

Result: Fair Value of $344.64 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can still be knocked off course, especially if U.S. China export restrictions hit the roughly US$680m China revenue or if valuation multiples compress sharply.

Find out about the key risks to this Cadence Design Systems narrative.

Another View On Valuation

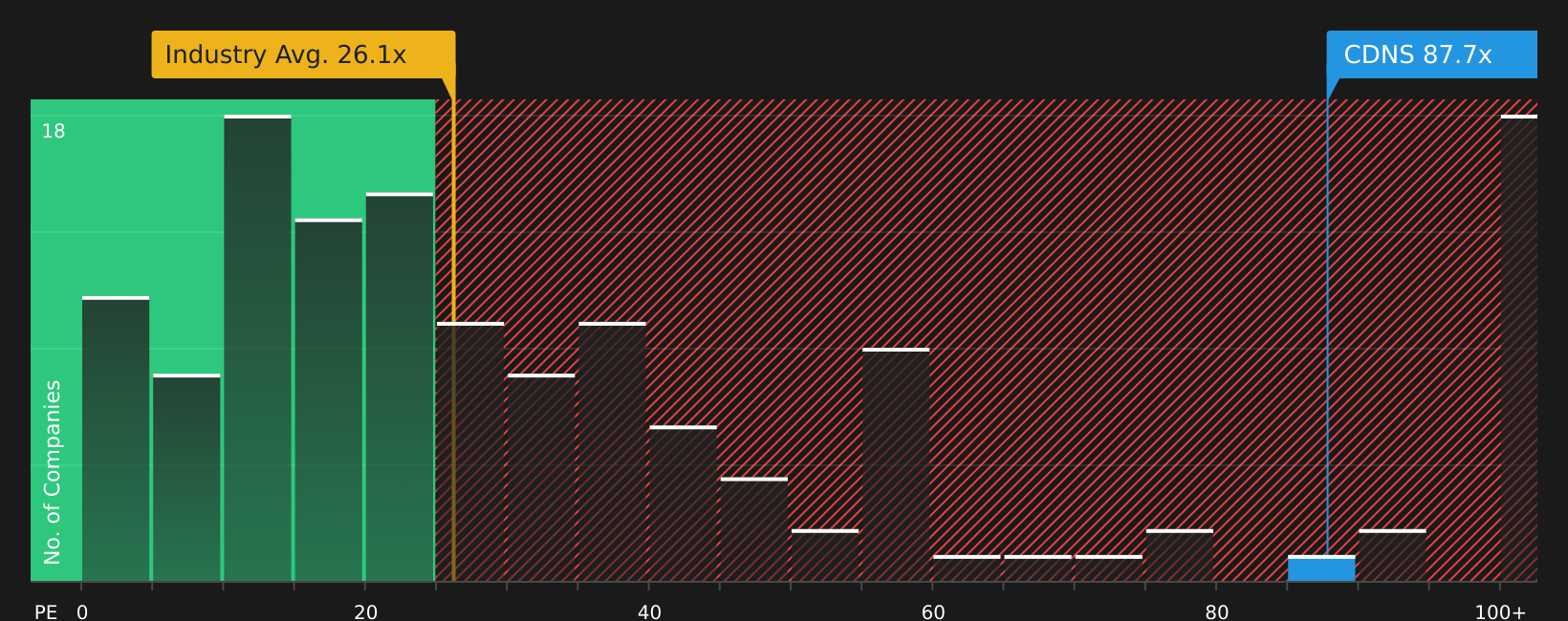

The first fair value of $344.64 paints Cadence as 17.5% undervalued, but the market’s own pricing tells a tougher story. The current P/E of 70.8x sits far above the US Software average of 28.3x, peer average of 39.5x and a fair ratio of 39.4x, which suggests meaningful valuation risk if sentiment cools.

For a closer look at what this gap could mean if the market gravitates back toward that fair ratio over time, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment split between rich multiples and long term potential, it can help to move quickly and stress test the numbers yourself against the 3 key rewards

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that fit your style even better, so put a few more ideas through your own filter.

- Target value focused opportunities by scanning 58 high quality undervalued stocks that pair quality fundamentals with attractive pricing.

- Prioritise resilience by reviewing 73 resilient stocks with low risk scores that score well on financial strength and volatility.

- Hunt for early stage upside by exploring the 30 elite penny stocks with strong financials that still show stronger balance sheets and cash generation than most peers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com