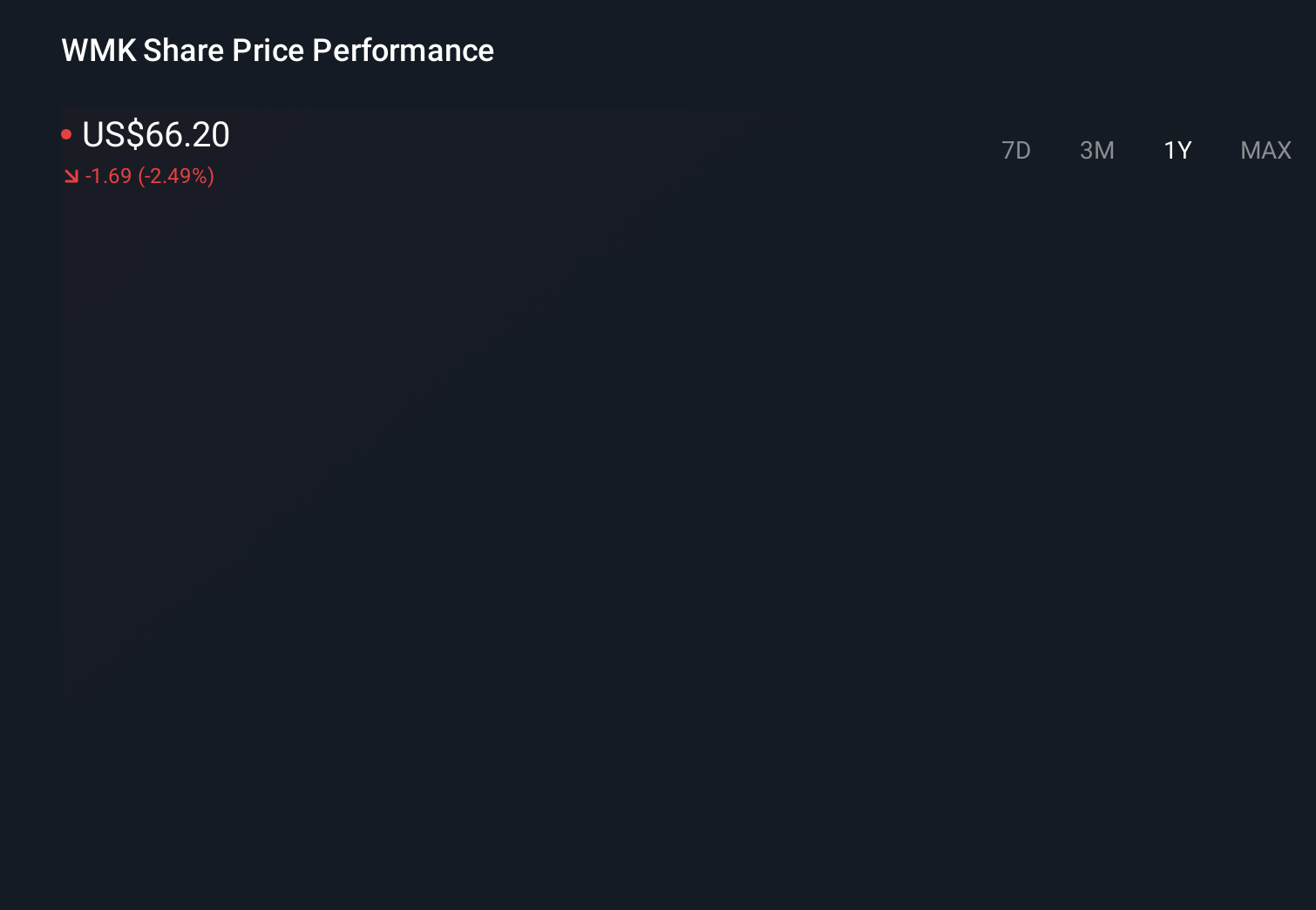

- In March 2026, Weis Markets, Inc. reported past fourth-quarter and full-year 2025 results, with sales rising to US$1,289.88 million for the quarter and US$4,939.37 million for the year, while net income softened to US$31.96 million and US$93.69 million respectively.

- The company’s higher revenue but lower net income and earnings per share, alongside the completion of a long-running share repurchase program, highlighted a trade-off between growth and profitability.

- We’ll now examine how the combination of rising sales and declining earnings shapes Weis Markets’ investment narrative for investors.

Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

What Is Weis Markets' Investment Narrative?

To own Weis Markets today, you need to believe in a steady, regional grocer that can translate dependable sales into healthier profits over time. The latest results reinforce that tension: full-year revenue pushed up to about US$4.96 billion, but net income eased back to US$93.69 million and margins slipped, and the long-running buyback quietly wrapped up without fresh support for earnings per share. With the share price soft over the past month, the March 2026 earnings do not radically reset the short term story, but they do sharpen the focus on cost control, execution under a seasoned management team and the impact of any further delay in SEC filings. The unchanged dividend points to continuity, while the key risk is that weaker profitability becomes more than a one year blip.

However, one risk is that softer earnings and filing delays hint at deeper operational pressures. Weis Markets' share price has been on the slide but might be up to 39% below fair value. Find out if it's a bargain.Exploring Other Perspectives

Explore 2 other fair value estimates on Weis Markets - why the stock might be worth 28% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Weis Markets research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Weis Markets research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Weis Markets' overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 58 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com