Financing move and product launch put Waters in focus

Waters (WAT) has drawn fresh attention after announcing a $3.5b senior notes offering through Augusta SpinCo Corporation, alongside the launch of its ARES-G3 Rheometer for faster, higher quality testing.

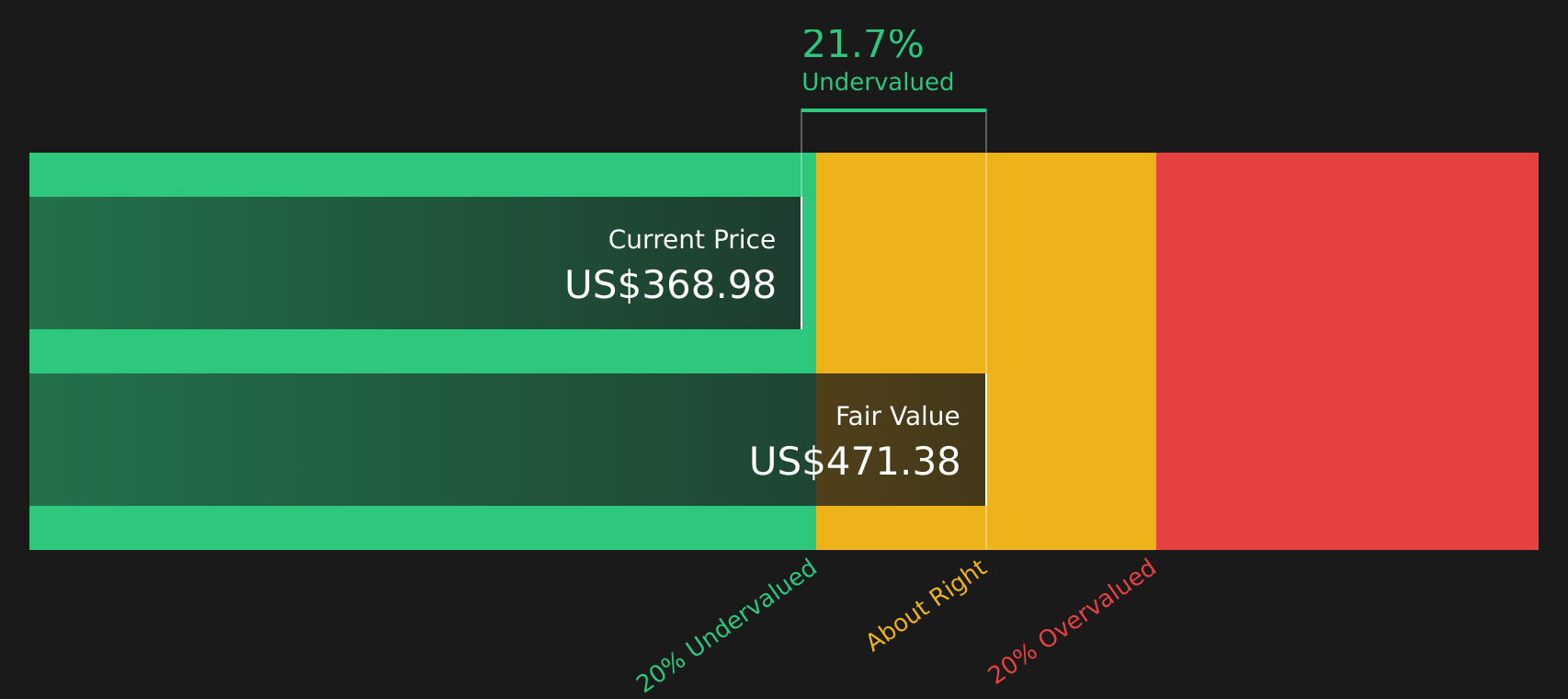

See our latest analysis for Waters.

At a share price of $301.92, Waters has seen short term weakness, with a 30 day share price return of 9.42% and a 90 day share price return of 21.54%. The 1 year total shareholder return of 18.07% contrasts with modest gains over three and five years, suggesting momentum has recently faded even as financing moves and product launches keep the story in focus.

If this financing update has you reassessing your watchlist, it could be a good moment to see what else is moving across 36 healthcare AI stocks

With shares giving back ground over the past year even as revenue and net income growth remain positive, the key question is whether Waters now trades at a discount to its fundamentals or if the market is already pricing in future growth.

Most Popular Narrative: 24.1% Undervalued

At a last close of $301.92 versus a narrative fair value of $398.05, the most followed view frames Waters as materially undervalued, with that gap tied to ambitious growth and profitability assumptions rather than short term trading swings.

Broadened revenue streams, recurring sales, and operational efficiencies position the company for stable margins and robust long-term earnings growth.

Execution risks from major acquisitions, weak end markets, margin pressures, and insufficient platform innovation could constrain earnings growth and threaten long-term competitiveness.

Want to see what sits behind that earnings push and margin story? The narrative leans on rapid top line expansion, shifting mix, and a premium future earnings multiple.

Result: Fair Value of $398.05 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat narrative could quickly shift if the BD integration underdelivers on planned synergies, or if funding softness in academic and pharma discovery markets persists.

Find out about the key risks to this Waters narrative.

Another view on valuation

The SWS DCF model paints a different picture to the upbeat narrative. On this view, WAT at $301.92 sits below an estimated future cash flow value of $429.62, which still points to undervaluation but rests on long range cash flow assumptions rather than the current earnings multiple. Which lens do you trust more for a complex story like this?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With mixed signals on value and sentiment, this is the moment to look through the numbers yourself and move quickly to shape your own view using the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one company, you risk missing opportunities that better match your goals, so put a few alternatives on your radar today.

- Spot potential value opportunities before the crowd by scanning 58 high quality undervalued stocks that pair solid fundamentals with attractive pricing signals.

- Prioritize resilience and sleep easier at night by focusing on 73 resilient stocks with low risk scores built to weather a range of market conditions.

- Add potential future standouts to your radar by running the screener containing 25 high quality undiscovered gems and seeing which quieter names still show strong fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com