- Wondering whether ArcBest at around US$94.60 is offering value right now or asking too much of future expectations? This article breaks down what the current price could be telling you.

- The share price has moved 10.1% over the last 7 days, while the 30 day return stands at a 10.0% decline and the 1 year return is 29.7%, with 22.6% year to date.

- Recent news coverage has focused on ArcBest as a transportation and logistics player in a sector that often reacts quickly to shifts in freight volumes, pricing and customer demand. These themes give helpful context when you look at the mix of short term pullbacks and longer term returns in the share price.

- ArcBest currently holds a valuation score of 3/6. The next sections will break that down across different valuation methods, then finish with a broader way to think about what the stock might be worth.

Approach 1: ArcBest Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes projections of a company’s future cash flows and discounts them back to today, to estimate what the business might be worth right now.

For ArcBest, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve months Free Cash Flow is about $38.19 million. Analyst inputs and extrapolated estimates point to projected Free Cash Flow of $198.03 million in 2026 and $287.60 million in 2028, with further projections extending out to 2035. All of these figures are in $ and are below $1b, so they remain in the millions range.

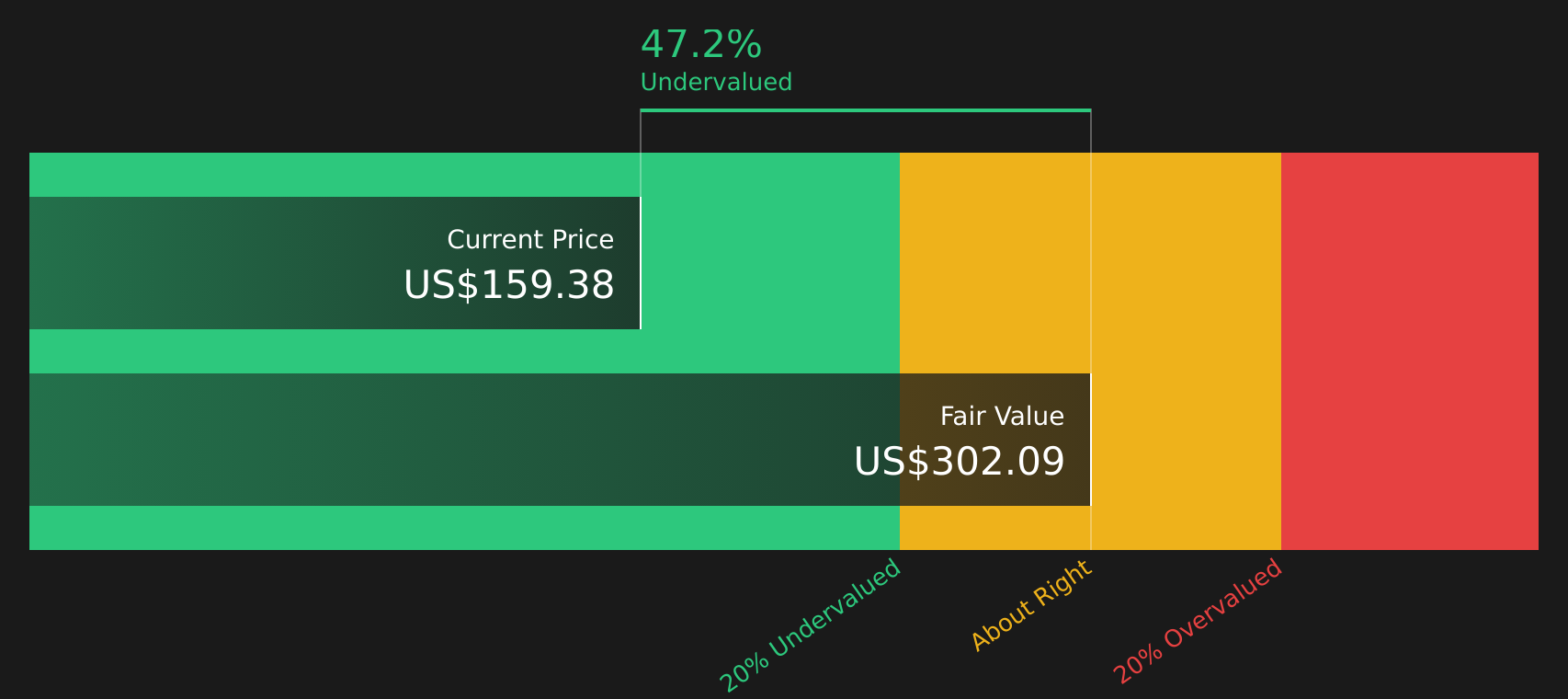

Aggregating and discounting these projected cash flows results in an estimated intrinsic value of about $387.56 per share. Versus a current share price around $94.60, the DCF indicates ArcBest is trading at a 75.6% discount to this intrinsic value, which screens as materially undervalued within this framework.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ArcBest is undervalued by 75.6%. Track this in your watchlist or portfolio, or discover 59 more high quality undervalued stocks.

Approach 2: ArcBest Price vs Earnings (P/E)

For a profitable company like ArcBest, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings, since it links directly to the business the company is already generating today.

A “normal” or “fair” P/E usually reflects how the market views a company’s growth potential and risk. Higher expected growth or lower perceived risk can justify a higher P/E, while lower growth or higher risk tends to align with a lower P/E.

ArcBest currently trades on a P/E of 35.10x, which is similar to the Transportation industry average of about 34.14x and sits below the peer average of 75.13x. Simply Wall St’s Fair Ratio for ArcBest is 26.25x. This Fair Ratio is a proprietary view of what ArcBest’s P/E might be given its earnings growth profile, industry, profit margins, market cap and specific risks.

Compared with a simple industry or peer comparison, the Fair Ratio aims to give a more tailored reference point because it explicitly weighs ArcBest’s own characteristics rather than treating all companies in the group as equal. With the current P/E at 35.10x and the Fair Ratio at 26.25x, the shares screen as overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your ArcBest Narrative

Earlier it was mentioned that there is an even better way to understand valuation, and Narratives offer that by letting you attach a clear story about ArcBest’s future revenue, earnings and margins to a forecast and a Fair Value, then compare it with the current price so you can decide whether the stock fits your own view.

On Simply Wall St’s Community page, Narratives are available as an easy tool used by millions of investors. There, you can see that one ArcBest bull might back a Fair Value around US$123.17 based on higher revenue, margins near 3.6% and a future P/E near 18x. A more cautious view might sit closer to US$81 with revenue closer to US$4.5b, margins around 3.8% and a future P/E near 12x. This shows how different stories and assumptions can reasonably lead to very different estimates.

Because Narratives update when new earnings, news or analyst targets arrive, you are not locked into a static model. Your chosen ArcBest Narrative keeps evolving so you can quickly see when your Fair Value has moved closer to or further away from the market price and decide whether that still matches your expectations.

For ArcBest however we will make it really easy for you with previews of two leading ArcBest Narratives:

Fair value in this bullish Narrative: US$123.17 per share

Discount to this fair value versus the recent US$94.60 price: about 23.2% undervalued

Revenue growth assumption: 6.38% a year

- Backs ArcBest to use its AI driven tools, digital quote engine and automation to cut structural costs and widen margins compared with slower moving logistics peers.

- Sees stickier small and mid sized business customers and tax incentives supporting higher quality revenue, better pricing power and room to reinvest in technology.

- Anchors on bullish analyst work that points to earnings of US$176.2m by 2029 and a future P/E of about 18x to arrive at a fair value of roughly US$123 per share.

Fair value in this bearish Narrative: US$81.00 per share

Premium to this fair value versus the recent US$94.60 price: about 16.7% overvalued

Revenue growth assumption: 4.87% a year

- Focuses on risks from automation, reshoring and new freight tech platforms that could let shippers bypass traditional carriers and pressure ArcBest on price and volume.

- Flags higher regulatory, labor and fleet modernization costs as potential headwinds for margins and free cash flow over time.

- Uses a lower analyst price target of US$72, more modest earnings expectations by 2028 and a future P/E near 13x to argue that upside from current levels could be limited.

Both Narratives use the same raw building blocks, just arranged around different expectations and risk weights. Your next step is to decide which story feels closer to your own view of ArcBest, then pressure test the revenue, margin and P/E assumptions before letting either of them influence how you think about the stock at around US$94.60.

Curious how numbers become stories that shape markets? Explore Community Narratives

Do you think there's more to the story for ArcBest? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com