- In March 2026, Walker & Dunlop, Inc. announced it had arranged a US$350 million aggregation debt facility with JPMorgan Chase Bank for a self-storage REIT platform backed by a joint venture between Centerbridge Partners and Reframe Holdings, anchored by six seed assets across diverse US metropolitan areas.

- This facility underscores Walker & Dunlop’s role as an arranger and advisor on large-scale, institutional real estate financings, highlighting its reach across both capital markets and equity structuring for specialized property platforms like self-storage.

- We’ll now examine how arranging this US$350 million self-storage debt facility may influence Walker & Dunlop’s investment narrative and growth drivers.

This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

Walker & Dunlop Investment Narrative Recap

To own Walker & Dunlop, you need to believe in its ability to convert real estate deal flow into consistent, fee-based earnings despite interest rate and volume headwinds. The new US$350 million self-storage facility reinforces its capital markets and advisory capabilities, but does not materially change the near term catalyst of improving transaction volumes or the key risk that higher or volatile rates could continue to weigh on origination and margin performance.

Among recent announcements, the Seventeenth Amendment to Walker & Dunlop’s warehousing credit facility with PNC Bank stands out alongside this self-storage mandate. Extending the facility to March 1, 2027 and expanding temporary advance capacity sit squarely within the same theme as the JPMorgan transaction: positioning the company with flexible balance sheet support so it can participate when debt placement and refinancing activity improves.

Yet investors should be aware that the combination of weak recent profitability, a high dividend payout, and sensitivity to interest rate conditions means...

Read the full narrative on Walker & Dunlop (it's free!)

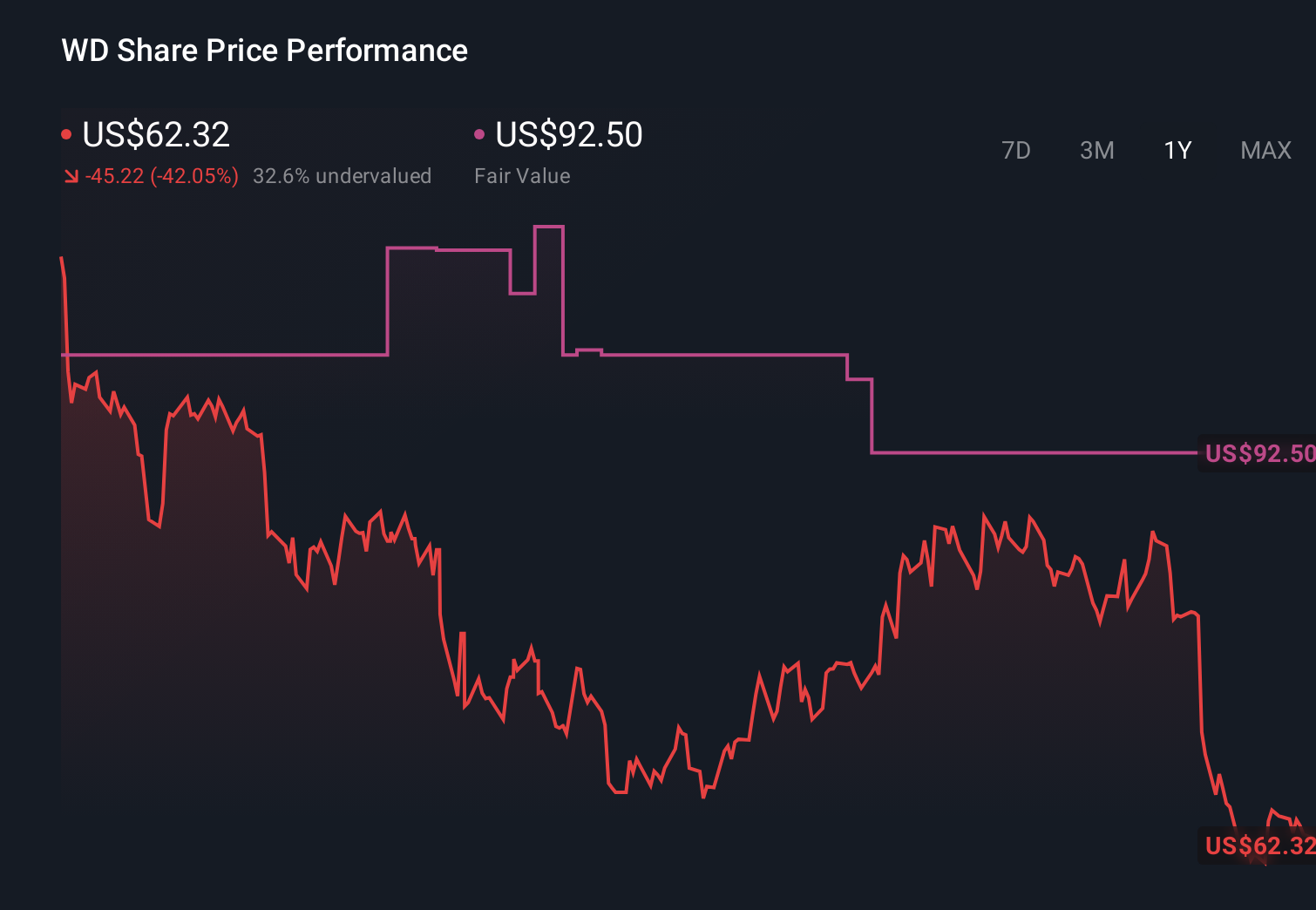

Walker & Dunlop's narrative projects $1.5 billion revenue and $233.2 million earnings by 2028. This requires 11.2% yearly revenue growth and a $125.4 million earnings increase from $107.8 million today.

Uncover how Walker & Dunlop's forecasts yield a $67.50 fair value, a 52% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates span roughly US$33 to US$68 per share, showing how far apart individual views can sit. Against that backdrop, you should weigh how Walker & Dunlop’s reliance on commercial real estate transaction volumes and interest rate conditions might influence its ability to turn advisory mandates into sustainable earnings over time.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth 25% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com