- Huntington Ingalls Industries recently secured ratification of new collective bargaining agreements at its Ingalls Shipbuilding division, granting union-represented workers an immediate 18% or higher base wage increase and extending contracts through March 8, 2031.

- This historic wage deal, coupled with HII’s broader workforce development push, signals a long-term commitment to labor stability, skills growth, and production throughput across its shipyards.

- We’ll now examine how this long-term wage agreement and expected improvements in workforce retention influence Huntington Ingalls’ investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Huntington Ingalls Industries Investment Narrative Recap

To own Huntington Ingalls, you need to believe that large, long-cycle U.S. Navy programs and a steadily improving industrial base will keep the order book and cash flows resilient, even as costs fluctuate. The historic Ingalls wage deal appears most relevant in the near term to margin risk and execution: it may pressure labor costs, but it also directly supports HII’s key short term catalyst of hitting throughput and delivery targets.

The recent commencement of 128 graduates from Newport News Shipbuilding’s Apprentice School underscores how the wage agreement sits within a broader workforce development effort aimed at supporting that throughput goal. While the long term financial impact of higher wages versus better retention is uncertain, pairing richer contracts at Ingalls with a growing skilled pipeline at Newport News may help HII address one of its most persistent execution challenges.

However, against this positive workforce story, investors should still weigh how wage inflation could interact with already tight shipbuilding margins and...

Read the full narrative on Huntington Ingalls Industries (it's free!)

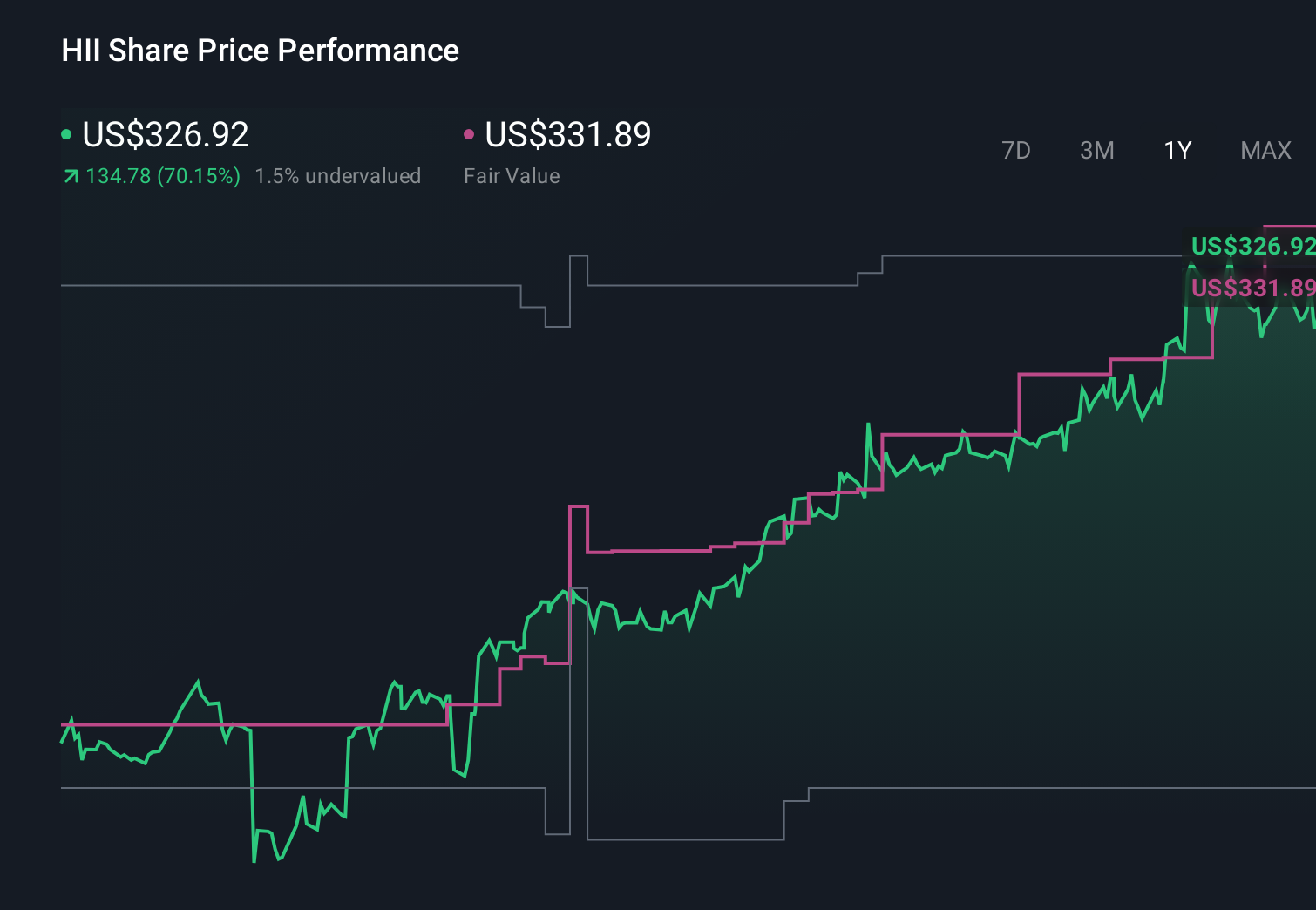

Huntington Ingalls Industries' narrative projects $13.6 billion revenue and $785.0 million earnings by 2028. This requires 5.4% yearly revenue growth and a $260.0 million earnings increase from $525.0 million today.

Uncover how Huntington Ingalls Industries' forecasts yield a $403.00 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue of about US$13.3 billion and earnings near US$767 million by 2028, and compared with concerns about demographic labor headwinds they may now see this wage deal very differently, so it is worth understanding how far opinions can spread before deciding which story you think fits best.

Explore 6 other fair value estimates on Huntington Ingalls Industries - why the stock might be worth as much as 14% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Huntington Ingalls Industries research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Huntington Ingalls Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Ingalls Industries' overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com