- Hilton Grand Vacations has opened Tradimo Kyoto Gojo, its first property in Kyoto and third in Japan, offering 63 one-bedroom suites near Kyoto Station and key cultural districts.

- The company is pairing this physical expansion with a partnership with the Kyoto Tourism Board and local nonprofits to support sustainable tourism and community initiatives in the region.

- We’ll now explore how this Kyoto opening, and HGV’s broader expansion in Japan, could influence the company’s investment narrative.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Hilton Grand Vacations Investment Narrative Recap

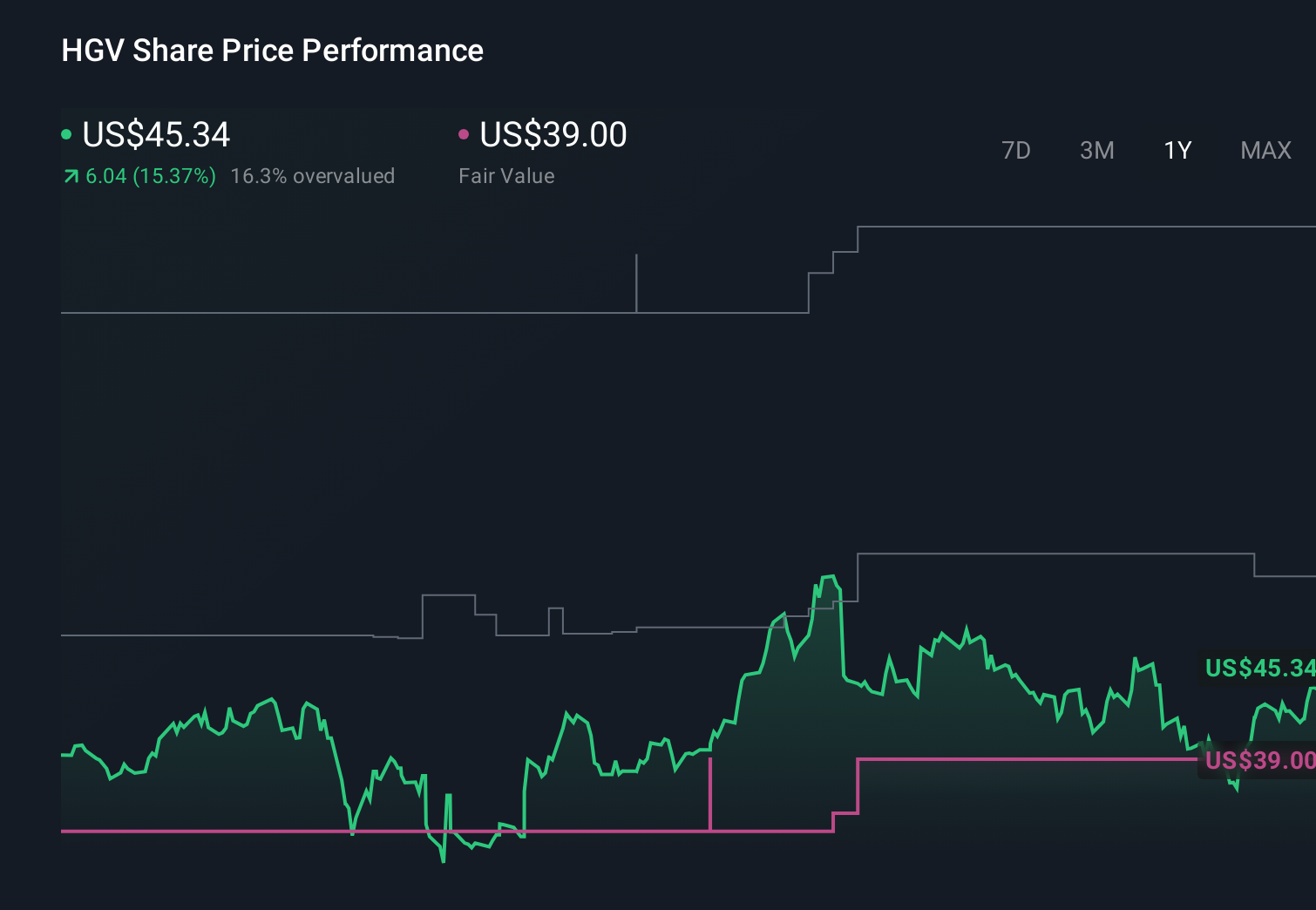

To own Hilton Grand Vacations, you need to be comfortable with a timeshare model that leans on member growth, financing, and large acquisitions like Bluegreen and Diamond. The Kyoto opening broadens HGV’s appeal in Japan but does not directly change the near term focus on integrating acquisitions and managing credit risk in its loan book, where elevated default rates and a sizeable bad debt allowance remain key watchpoints.

Among recent developments, the expanded US$600 million share buyback program stands out alongside Tradimo Kyoto Gojo. For investors, this pairs on the ground growth in Japan with a capital return plan that could influence earnings per share and sentiment around the integration of Bluegreen and Diamond. How well the company balances heavy investment, shareholder returns, and credit quality will matter at least as much as headline openings like Kyoto.

Yet behind the appeal of new resorts, investors should also be aware of rising defaults and a 27 percent bad debt allowance...

Read the full narrative on Hilton Grand Vacations (it's free!)

Hilton Grand Vacations' narrative projects $6.4 billion revenue and $785.5 million earnings by 2028.

Uncover how Hilton Grand Vacations' forecasts yield a $52.00 fair value, a 25% upside to its current price.

Exploring Other Perspectives

While consensus focuses on debt risk and modest revenue growth, the most optimistic analysts once modeled HGV reaching about US$6.4 billion sales and US$962.1 million earnings, which shows how far opinions can stretch and why this Kyoto move could still reshape both the bullish and cautious narratives.

Explore 4 other fair value estimates on Hilton Grand Vacations - why the stock might be worth just $52.00!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Hilton Grand Vacations research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Hilton Grand Vacations research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hilton Grand Vacations' overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com