- In the past week, The Hartford reported Q4 2025 results showing net income rising 33% year over year, supported by 8% growth in property & casualty earned premiums, higher net investment income, and stronger underwriting performance.

- Separately, The Hartford renewed its backing of Active Minds’ “Send Silence Packing” mental health exhibit, underscoring the insurer’s emphasis on workplace and community well-being alongside financial execution.

- With Q4 earnings driven by higher premiums and underwriting improvements, we’ll now examine how this update shapes The Hartford’s investment narrative.

The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Hartford Insurance Group Investment Narrative Recap

To own Hartford, you need to be comfortable with a business that leans heavily on disciplined underwriting and risk selection in property and casualty lines, while accepting exposure to catastrophe events and pricing pressure. The Q4 2025 beat, driven by higher earned premiums and stronger underwriting, supports the near term earnings catalyst but does not remove the central risk around large loss volatility and competitive intensity in commercial and personal insurance markets.

The renewed support for Active Minds’ “Send Silence Packing” exhibit ties into Hartford’s broader focus on workplace resilience, which can matter for long term client relationships and brand strength. While this initiative does not directly change underwriting results or pricing power, it sits alongside the company’s push into technology, data and operational efficiency, all of which underpin the thesis that earnings quality and consistency can improve over time.

Yet investors should also weigh how exposed Hartford still is to elevated catastrophe losses and...

Read the full narrative on Hartford Insurance Group (it's free!)

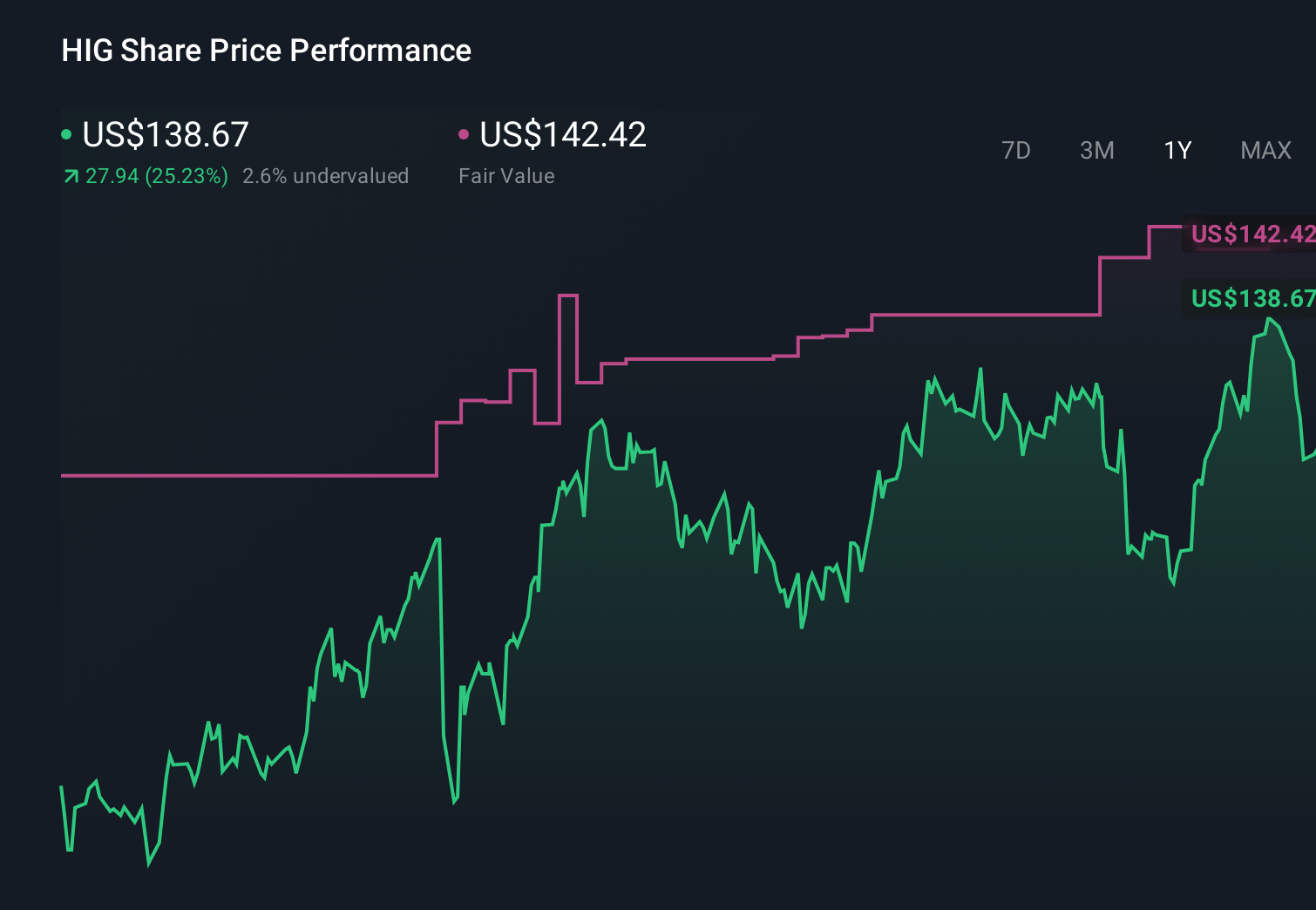

Hartford Insurance Group's narrative projects $32.0 billion revenue and $3.7 billion earnings by 2028. This requires 5.3% yearly revenue growth and about a $0.5 billion earnings increase from $3.2 billion today.

Uncover how Hartford Insurance Group's forecasts yield a $150.85 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently estimate Hartford’s fair value between US$136 and about US$333, reflecting a wide span of individual views. Set those against the central risk that large catastrophe losses and competitive pressures could quickly alter underwriting results and prompt you to compare several different valuation and risk scenarios for this stock.

Explore 5 other fair value estimates on Hartford Insurance Group - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hartford Insurance Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Hartford Insurance Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hartford Insurance Group's overall financial health at a glance.

No Opportunity In Hartford Insurance Group?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 34 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com