Integer Holdings event overview

Integer Holdings (ITGR) has drawn fresh attention after recent share price moves, with the stock down about 3% over the past month and up roughly 15% in the past 3 months.

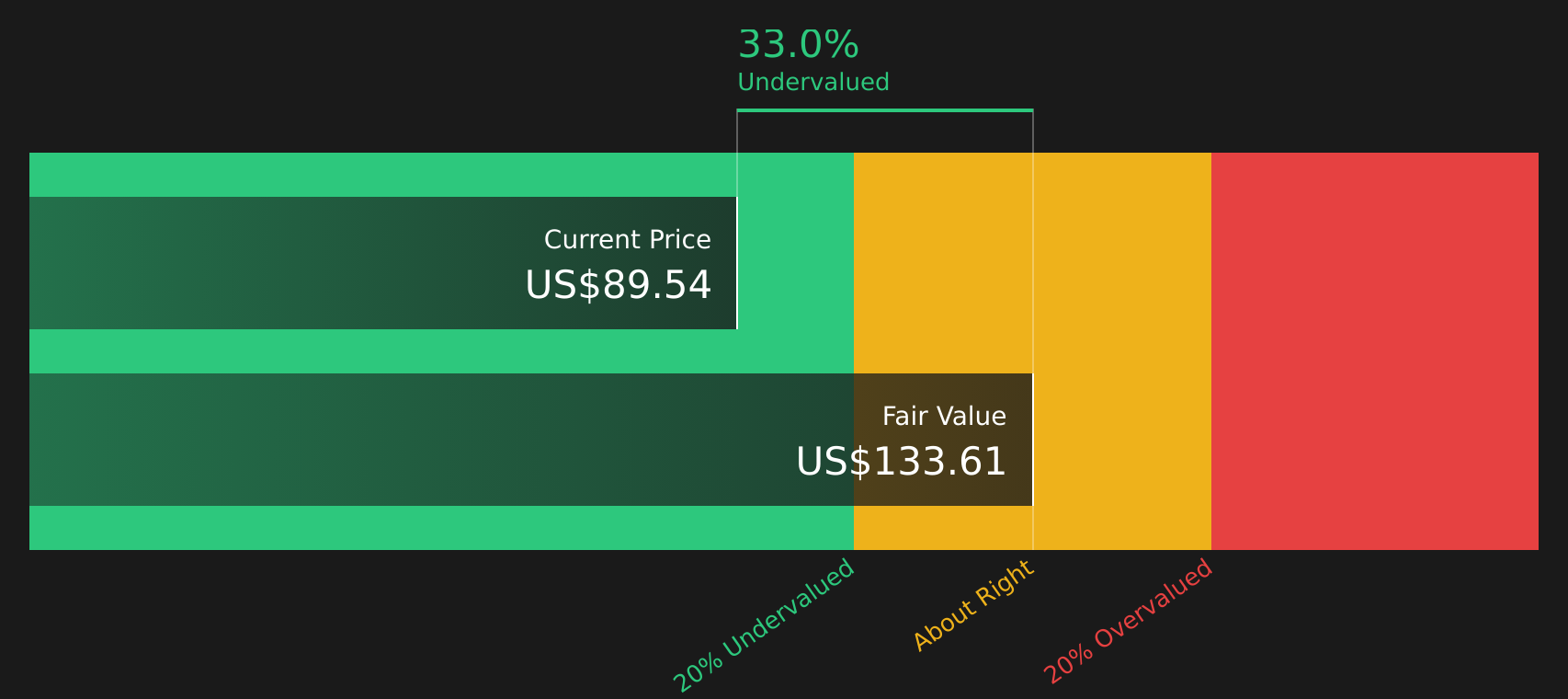

See our latest analysis for Integer Holdings.

The 1-year total shareholder return decline of 29.65% contrasts with the recent 14.55% 90-day share price return. This suggests momentum has picked up after a weaker stretch for long-term holders at the latest share price of US$83.30.

If Integer’s recent rebound has you thinking about where else growth stories might emerge, this could be a good moment to scan 34 healthcare AI stocks for your next idea.

With the shares sitting around US$83.30, an indicated intrinsic discount of about 41% and a value score of 3, should you see Integer as undervalued today or is the recent rebound already pricing in future growth?

Most Popular Narrative: 10.1% Undervalued

Integer Holdings' most followed valuation narrative points to a fair value of about $92.63, compared with the last close at $83.30, framing the current setup as modestly discounted.

The analysts have a consensus price target of $140.875 for Integer Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $155.0, and the most bearish reporting a price target of just $132.0.

Curious what kind of revenue curve and margin rebuild sit behind that valuation gap? The core narrative leans on faster earnings growth and a richer future earnings multiple. The full set of assumptions shows how those pieces are expected to fit together.

Result: Fair Value of $92.63 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are pressure points to watch, including the expected 300 to 400 basis point growth drag from three weaker products and ongoing exposure to foreign exchange swings.

Find out about the key risks to this Integer Holdings narrative.

Another angle on Integer’s valuation

The earlier view leaned on a fair value of $92.63, which puts Integer at roughly a 10% discount to that narrative. Our DCF model is far more generous, with a future cash flow value of about $141.39, implying a much wider gap. Which set of assumptions do you find more realistic?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Does this mix of risk and reward sound balanced enough for you, or a bit stretched? Act while the details are fresh and weigh the trade offs yourself with 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Integer has sharpened your focus, do not stop here. Broaden your watchlist with a few focused stock ideas that match different goals and risk levels.

- Target potential mispricing by scanning our list of 47 high quality undervalued stocks that pair compressed expectations with solid underlying fundamentals.

- Strengthen your income stream by reviewing 15 dividend fortresses, where yields of 5% or more come with an emphasis on resilience.

- Hunt for off-the-radar opportunities using our screener containing 25 high quality undiscovered gems, built to surface quality names that many investors may still be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com