- Goldman Sachs recently reaffirmed its positive stance on Patterson-UTI Energy, highlighting resilient customer activity despite Middle East geopolitical risks, strong adjusted free cash flow in FY 2025, and a 25% increase in the quarterly dividend implemented in early 2026.

- At the same time, Director Tiffany Cepak’s sale of 12,000 shares, leaving her with 161,111 shares amid a pattern of more insider sells than buys over the past year, offers an additional data point on insider behavior for investors to consider.

- With this backdrop of stronger free cash flow supporting a higher dividend, we’ll examine how these developments influence Patterson-UTI Energy’s investment narrative.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

Patterson-UTI Energy Investment Narrative Recap

To own Patterson-UTI Energy, you need to be comfortable with a cyclical, North America focused oilfield services business that depends heavily on drilling and completions activity. The key short term catalyst remains how quickly customer activity holds up or improves, while the biggest risk is a deeper or more prolonged softness in drilling that pressures margins. The latest Goldman Sachs commentary and dividend increase do not materially change either the main catalyst or the core risk.

The most relevant recent announcement here is the 25% increase in the quarterly dividend, funded by strong adjusted free cash flow in FY 2025. For income focused investors, that move signals management’s confidence in cash generation even as the company remains unprofitable on a net income basis. It also ties directly into the catalyst of higher activity and better utilization, since sustaining that higher payout will rely on continued operational and cash flow strength.

Yet alongside the higher dividend, the pattern of insider selling is a reminder that concentration risk in North American shale is something investors should be aware of...

Read the full narrative on Patterson-UTI Energy (it's free!)

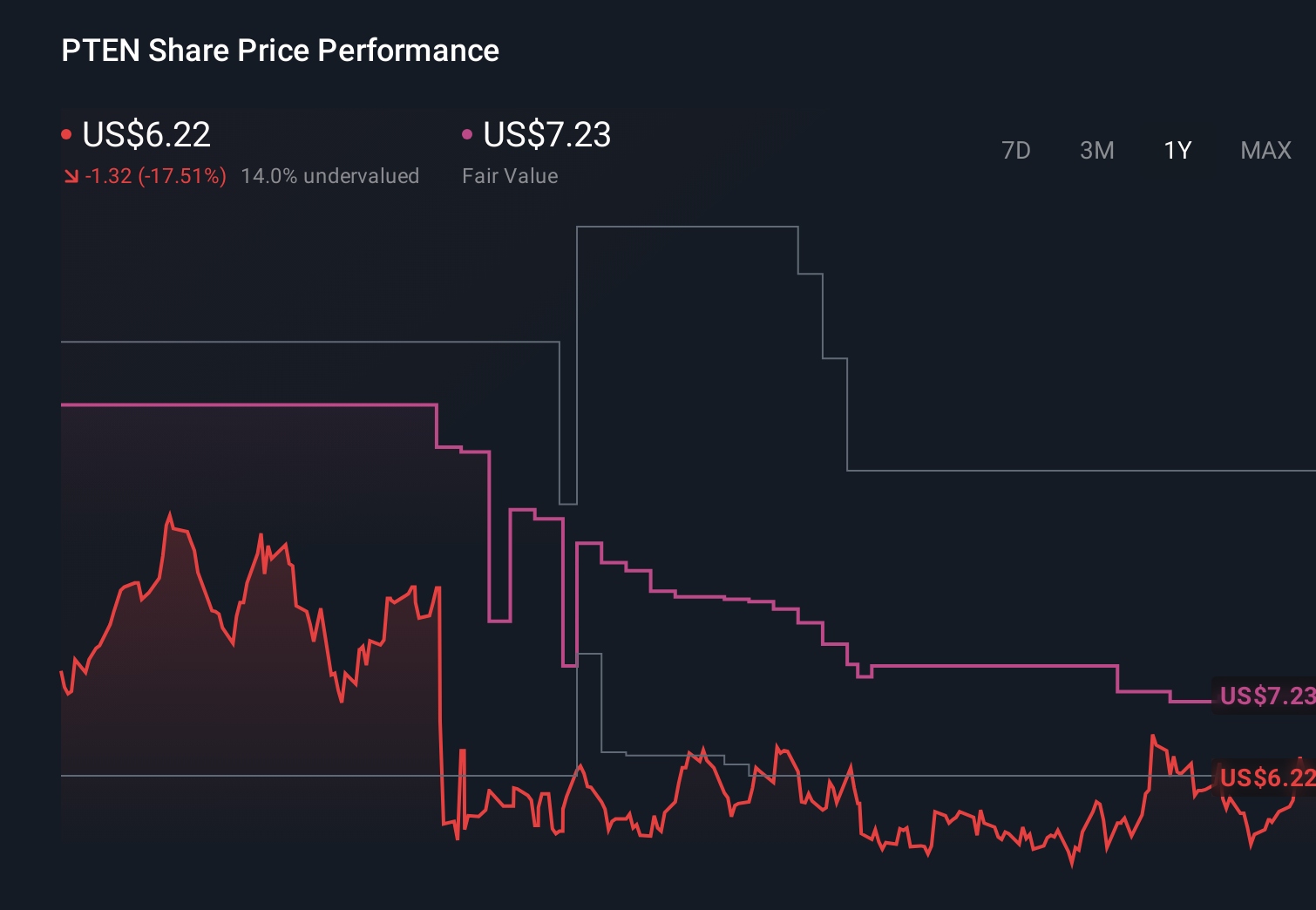

Patterson-UTI Energy's narrative projects $4.8 billion revenue and $337.4 million earnings by 2028. This assumes a 1.3% yearly revenue decline and an earnings increase of about $1.44 billion from current earnings of -$1.1 billion.

Uncover how Patterson-UTI Energy's forecasts yield a $8.84 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Some of the most pessimistic analysts saw revenue shrinking about 3.8% a year and no profitability within three years, so compared with that more cautious view of North American shale volatility, this new free cash flow and dividend story could eventually shift expectations, depending on how the underlying activity trends evolve from here.

Explore 4 other fair value estimates on Patterson-UTI Energy - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Patterson-UTI Energy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Patterson-UTI Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Patterson-UTI Energy's overall financial health at a glance.

No Opportunity In Patterson-UTI Energy?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com