Why TriMas stock is back on investors' radar

TriMas (TRS) has drawn fresh attention after reporting detailed fourth quarter and full year 2025 results, issuing 2026 sales guidance, and updating investors on the scale of its multi year share repurchase activity.

See our latest analysis for TriMas.

Despite the strong earnings headlines, the recent 1 day share price return of 3.23% and 7 day share price return of 4.20% indicate some cooling after a 90 day share price return of 12.23%. At the same time, the 1 year total shareholder return of 55.17% points to momentum that has built over a longer period.

If TriMas has you thinking about where else strong executions and capital returns might be emerging, it could be a good moment to scan our 20 top founder-led companies for fresh ideas beyond this stock.

With TriMas shares at US$37.44, recent earnings progress, active buybacks and guidance for 2026 now in play, the key question is simple: is the stock on sale or is the market already pricing in what comes next?

Most Popular Narrative: 9.8% Undervalued

TriMas is trading at $37.44 against a widely followed fair value estimate of $41.50, which puts the current share price below that narrative anchor.

Investments in automation and alignment with global packaging trends position the company for sustained revenue growth and stronger long term earnings.

Increased investment in automation, advanced IT platforms, and operational best practices is expected to unlock cost efficiencies and productivity gains across all business segments, contributing to sustainable improvements in EBITDA margin and overall profitability.

Want to see how this margin story supports that higher fair value? The narrative leans on faster top line progress, rising profitability, and a very specific earnings multiple. The full breakdown shows exactly how those moving parts are stitched together.

Result: Fair Value of $41.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to watch for slower packaging integration and any sustained weakness in aerospace or industrial demand, as these factors could undercut those optimistic margin assumptions.

Find out about the key risks to this TriMas narrative.

Another angle on valuation

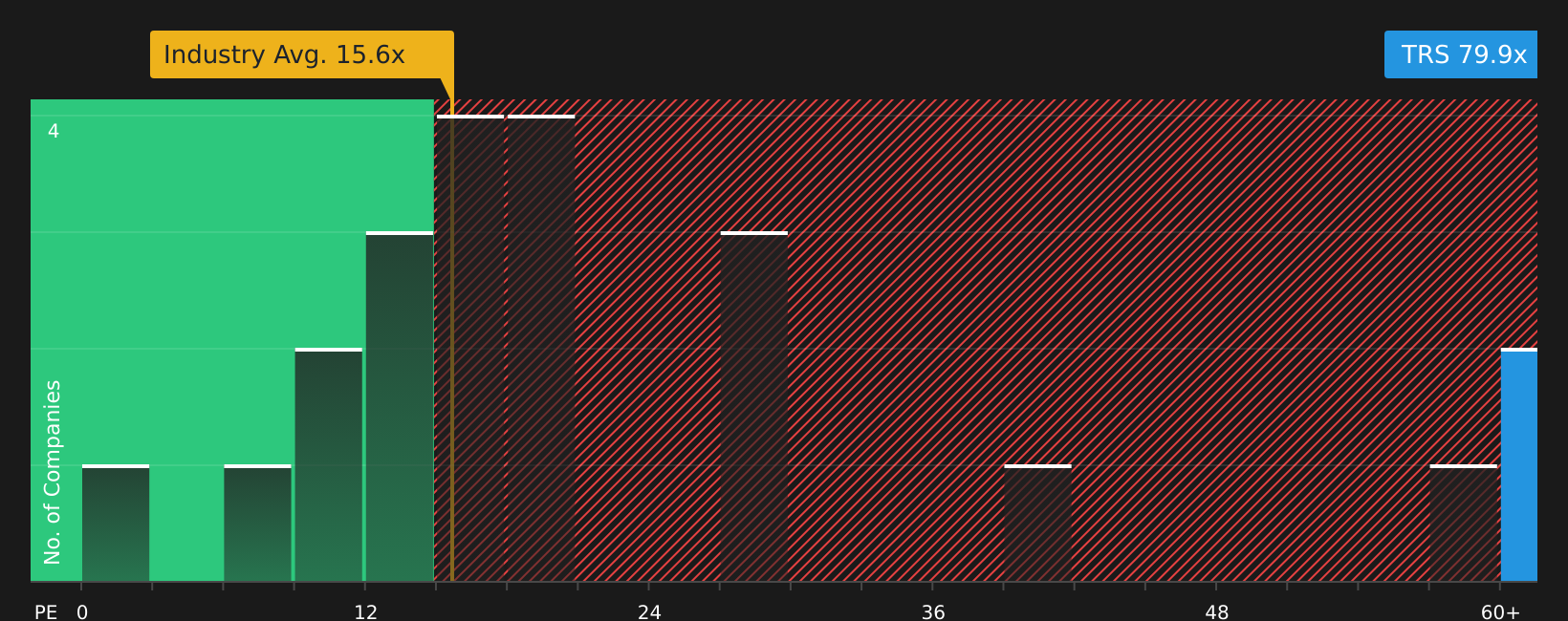

The earlier fair value of $41.50 paints TriMas as 9.8% undervalued, but the earnings multiple sends a different signal. At a P/E of 19.5x, the shares are above the 14.6x fair ratio our model points to and above the global packaging average of 15.9x, even if they sit slightly below peer levels at 20.5x. So is this a discount, or are you paying up for execution risk?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Curious whether the tone of this piece skews too positive or too cautious? Act soon to review the full picture yourself, including 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If this update has sharpened your focus, do not stop with a single stock. Use the Simply Wall Street Screener to spot other opportunities before they move without you.

- Target stability first and see which companies pass our rigorous checks with a 63 resilient stocks with low risk scores that can help you sleep better at night.

- Hunt for value and put underappreciated quality on your radar using our screener containing 24 high quality undiscovered gems before they appear on everyone else's watchlist.

- Build a stronger core and back companies with healthier finances by starting with the solid balance sheet and fundamentals stocks screener (41 results) tailored to resilient fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com