- In late February 2026, Vipshop Holdings reported fourth-quarter 2025 revenue of CNY 32,473.78 million and net income of CNY 2,589.22 million, issued first-quarter 2026 revenue guidance of RMB 26.3 billion to RMB 27.6 billion, declared an annual dividend of US$0.6000 per share, and confirmed substantial progress on its share buyback program.

- An interesting takeaway is that Vipshop slightly improved quarterly profitability despite lower revenue, while simultaneously committing cash to both higher dividends and sizeable repurchases, signalling management’s confidence in its balance sheet and cash generation.

- Next, we will examine how Vipshop’s higher dividend and active share buybacks may influence its income-focused, efficiency-led investment narrative.

We've uncovered the 16 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Vipshop Holdings Investment Narrative Recap

To stay invested in Vipshop, you need to believe its discount-focused model can keep attracting loyal shoppers while preserving healthy profitability, even if top-line growth is modest. The latest results, with slightly higher quarterly net income on lower revenue and relatively flat first quarter guidance, do not materially change that near term earnings execution remains the key catalyst, while competitive and consumer demand pressures in China stay the biggest risk.

Among the new announcements, the accelerated buyback under the existing US$1,000 million program stands out. Repurchasing 8.38% of shares outstanding by the end of 2025 can meaningfully lift earnings per share if profits hold up, reinforcing Vipshop’s income and efficiency narrative, but it also heightens the importance of the company sustaining cash generation in a soft consumer and highly competitive e commerce market.

Yet against that positive capital return story, investors should still be aware of how intensifying competition and shifting shopping habits could...

Read the full narrative on Vipshop Holdings (it's free!)

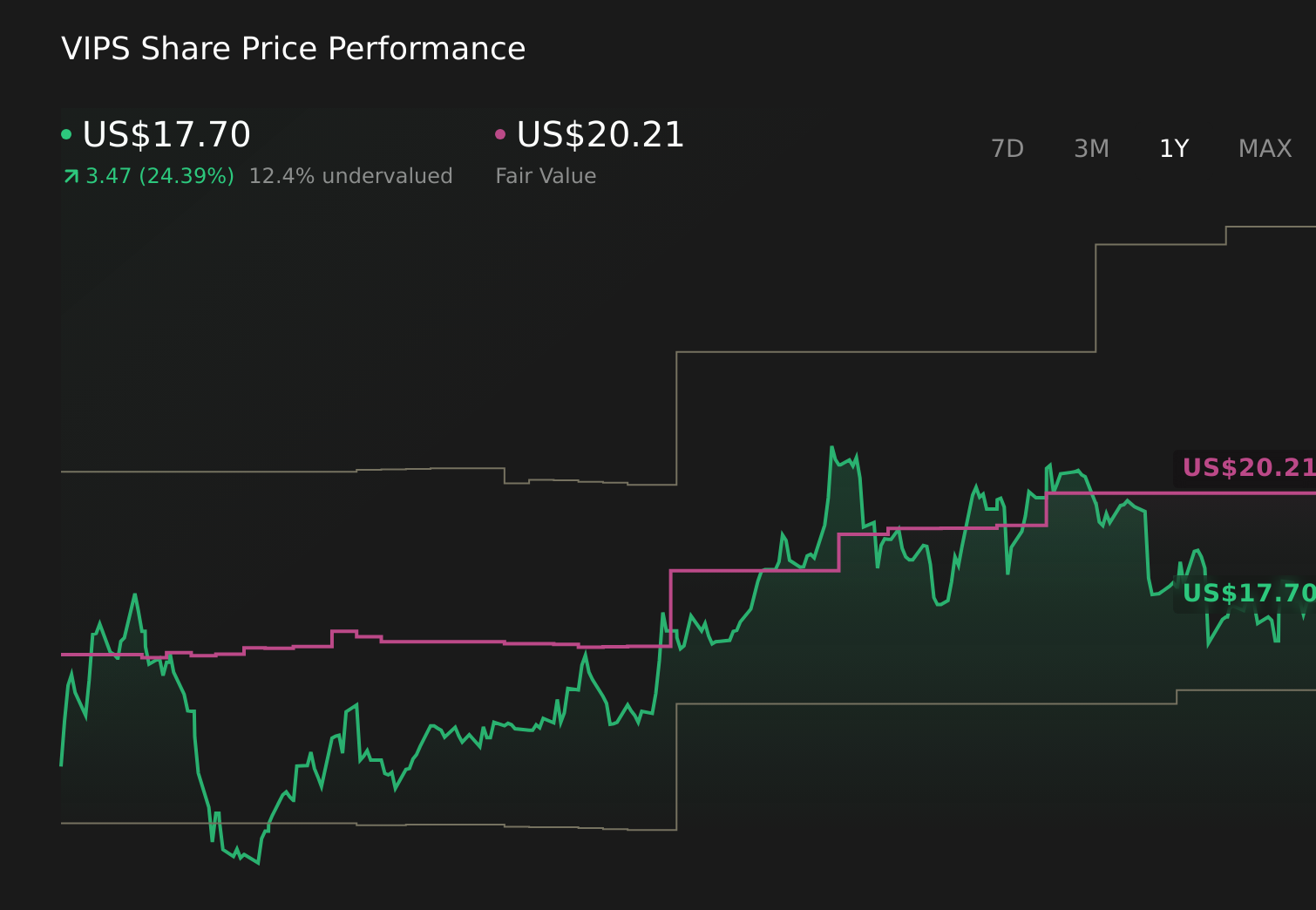

Vipshop Holdings' narrative projects CN¥113.0 billion revenue and CN¥8.2 billion earnings by 2028. This requires 2.2% yearly revenue growth and an earnings increase of about CN¥1.3 billion from CN¥6.9 billion today.

Uncover how Vipshop Holdings' forecasts yield a $20.24 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming only about 1.2 percent annual revenue growth and largely flat earnings around CN¥6.9 billion, so this earnings and guidance update could either ease those worries or reinforce them, depending on how you interpret Vipshop’s buybacks and dividend alongside the risk of tougher e commerce rivalry in China.

Explore 6 other fair value estimates on Vipshop Holdings - why the stock might be worth 27% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Vipshop Holdings research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Vipshop Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vipshop Holdings' overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com