Advanced Drainage Systems (WMS) has drawn attention after recent trading left the shares with a 1 day return of about a 2% decline and a 15% decline over the past week, prompting fresh questions about its valuation.

See our latest analysis for Advanced Drainage Systems.

That sharp 15% 7 day share price decline, alongside a 9% 30 day and 2% year to date share price pullback to about $146, contrasts with a 28% 1 year total shareholder return. This suggests recent momentum is fading after a stronger period.

If this kind of swing has you reassessing your watchlist, it could be a good time to look at 20 top founder-led companies as potential fresh ideas to research next.

So with Advanced Drainage Systems trading around $146 after recent pullbacks, but supported by a 28% 1 year total return and analyst targets at $197.20, is this weakness a buying opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 25.9% Undervalued

Advanced Drainage Systems last closed at about $146, while the most followed narrative sets fair value near $197, framing the recent pullback as a sizeable discount to that estimate.

Ongoing climate change and increasing frequency/severity of extreme weather events are driving up the necessity for advanced stormwater management and resilient drainage infrastructure, underpinning structural, long-term volume growth, supporting sustained revenue acceleration.

Rising regulatory emphasis on water quality and sustainable construction (with more stringent stormwater and pollution controls) is increasing adoption of high-margin, innovative solutions such as the recently launched Arcadia hydrodynamic separator and EcoStream Biofiltration products, which is likely to expand net margins and boost revenue mix over time.

Curious what growth rates, margin shifts and future earnings multiple the narrative uses to reach that near $200 fair value? The full story ties these moving parts together in a way the headline numbers alone do not show.

Result: Fair Value of $197.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this narrative could be knocked off course if construction and infrastructure demand stays weak or if higher raw material costs squeeze margins more than expected.

Find out about the key risks to this Advanced Drainage Systems narrative.

Another Angle On Valuation

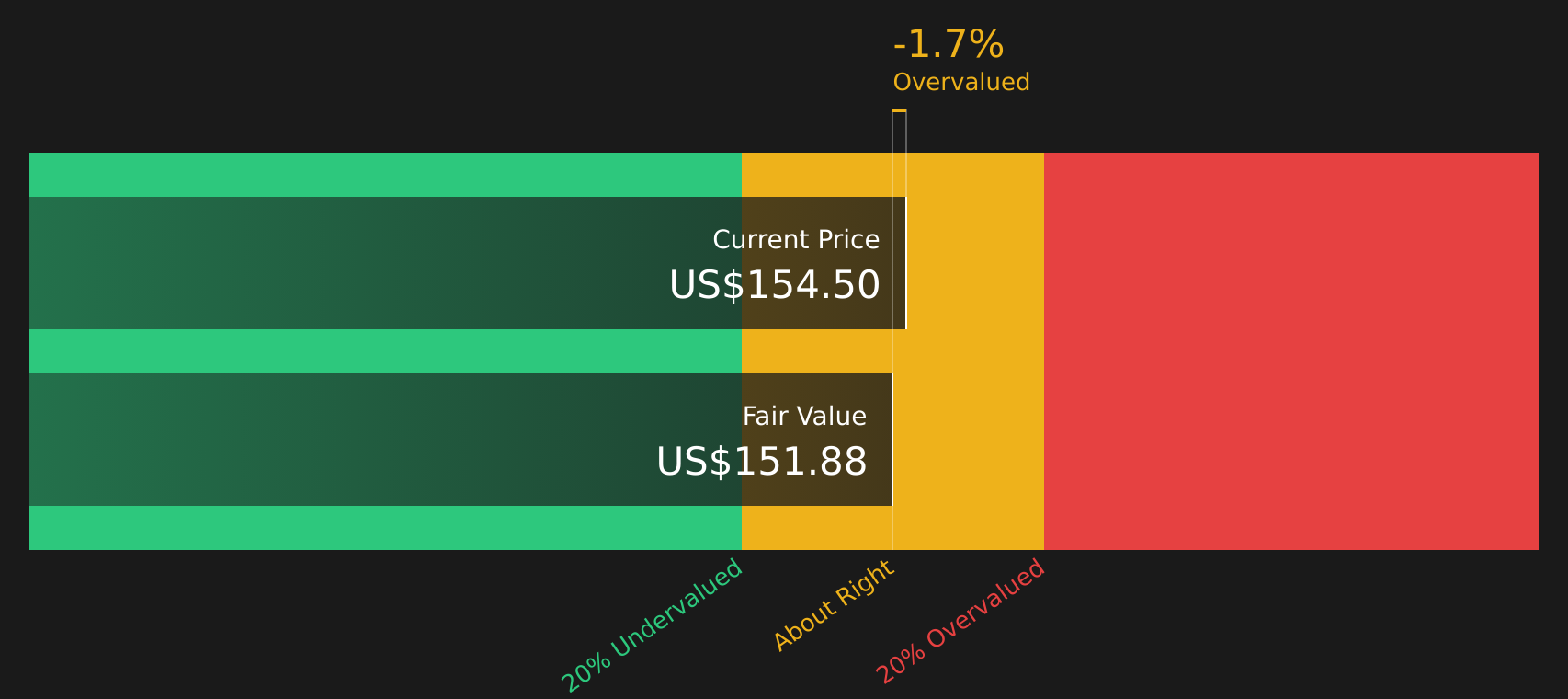

While the popular narrative leans on a fair value of $197.20, the Simply Wall St DCF model lands much lower, at $112.01. On that view, Advanced Drainage Systems at about $146 looks expensive rather than discounted. This raises a simple question for you: are the growth assumptions or the cash flow model more likely to be off?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Advanced Drainage Systems for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals so far, right? If you want to move quickly and form your own view, take a closer look at the company’s 3 key rewards to see what others are optimistic about.

Looking for more investment ideas?

If this update has sharpened your focus on quality, do not stop here. The next opportunity you are glad you found could be one careful screen away.

- Target resilient balance sheets by scanning our solid balance sheet and fundamentals stocks screener (41 results), which filters for companies with financial foundations designed to handle tougher conditions.

- Hunt for pricing gaps using the 49 high quality undervalued stocks, where you can spot companies that screen as higher quality than their current market price suggests.

- Unearth potential future standouts with the screener containing 24 high quality undiscovered gems and get in the habit of researching ideas before they sit on everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com