- In early 2026, The Hartford Insurance Group highlighted its technology-driven transformation, emphasizing AI-enabled improvements in claims, underwriting, and customer interactions, alongside robust Business Insurance performance, leadership in Small Business, expansion of its Personal Insurance agency platform, and plans to increase share buybacks beginning in 2026.

- An interesting dimension of this update is how Hartford is pairing operational AI investments with capital returns, signaling management’s confidence in its business model and digital roadmap.

- Next, we’ll examine how Hartford’s increased use of AI across claims and underwriting may influence its existing investment narrative and outlook.

Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Hartford Insurance Group Investment Narrative Recap

To own Hartford, you need to believe its core insurance franchises can keep earning attractive returns while its technology spending pays off in better efficiency and risk selection. The latest AI-focused update and planned share buybacks support the current catalyst around digital execution and capital returns, but do not materially change the key near term risk that catastrophe losses or pricing pressure could still weigh on margins.

Among recent announcements, Hartford’s decision to increase share buybacks beginning in 2026 stands out alongside its AI investments, tying operational progress to capital return. This matters for investors watching whether Hartford can keep balancing sizeable technology spending with shareholder payouts, while still managing exposure to elevated catastrophe events and competitive pressures in Business and Personal Insurance.

Yet, even with these AI gains and higher buybacks, investors should be aware of the risk that catastrophe losses could still...

Read the full narrative on Hartford Insurance Group (it's free!)

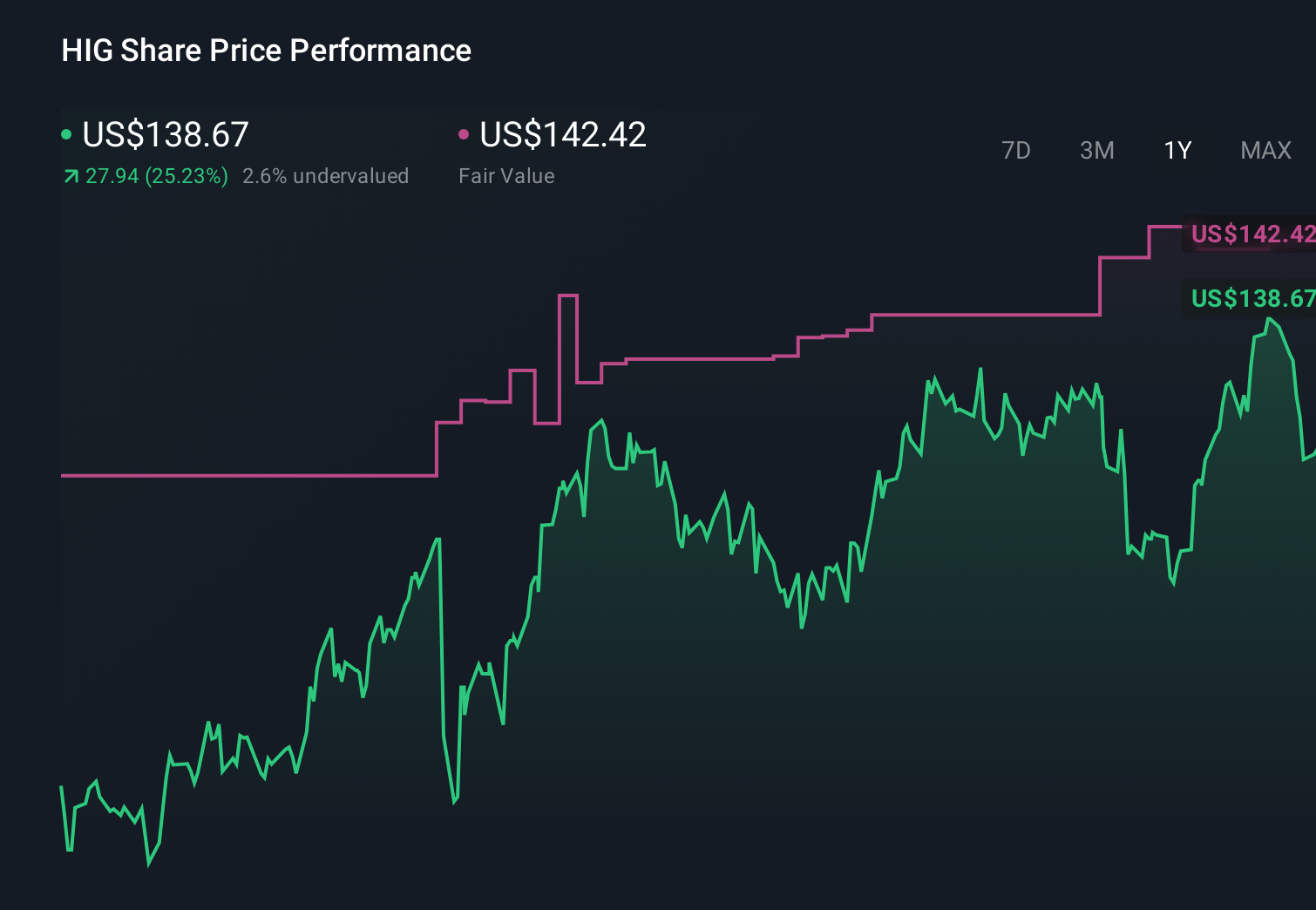

Hartford Insurance Group's narrative projects $32.0 billion revenue and $3.7 billion earnings by 2028. This requires 5.3% yearly revenue growth and a roughly $0.5 billion earnings increase from $3.2 billion today.

Uncover how Hartford Insurance Group's forecasts yield a $150.85 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$141 to US$333 per share, showing how far apart individual views can be. You can weigh this spread against the risk that elevated catastrophe losses may still pressure Hartford’s margins and shape its longer term performance.

Explore 4 other fair value estimates on Hartford Insurance Group - why the stock might be worth just $141.25!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Hartford Insurance Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Hartford Insurance Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hartford Insurance Group's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com