UGI (UGI) is in the spotlight after its latest quarter showed earnings per share moving down while segment EBIT grew, alongside ongoing LPG divestitures, fresh leadership and continued capital returns to shareholders.

See our latest analysis for UGI.

UGI’s share price has been firming up, with an 11.0% 90 day share price return and a 25.29% 1 year total shareholder return. This suggests recent earnings, buybacks and leadership changes are starting to reshape sentiment around the stock’s risk and income profile.

If UGI’s mix of regulated utilities and energy infrastructure has your attention, it could be a good moment to widen your search with our 25 power grid technology and infrastructure stocks.

With earnings per share under pressure, segment EBIT up and the share price already delivering a 25.29% 1 year total return, you have to ask: is UGI still undervalued, or are markets already pricing in future growth?

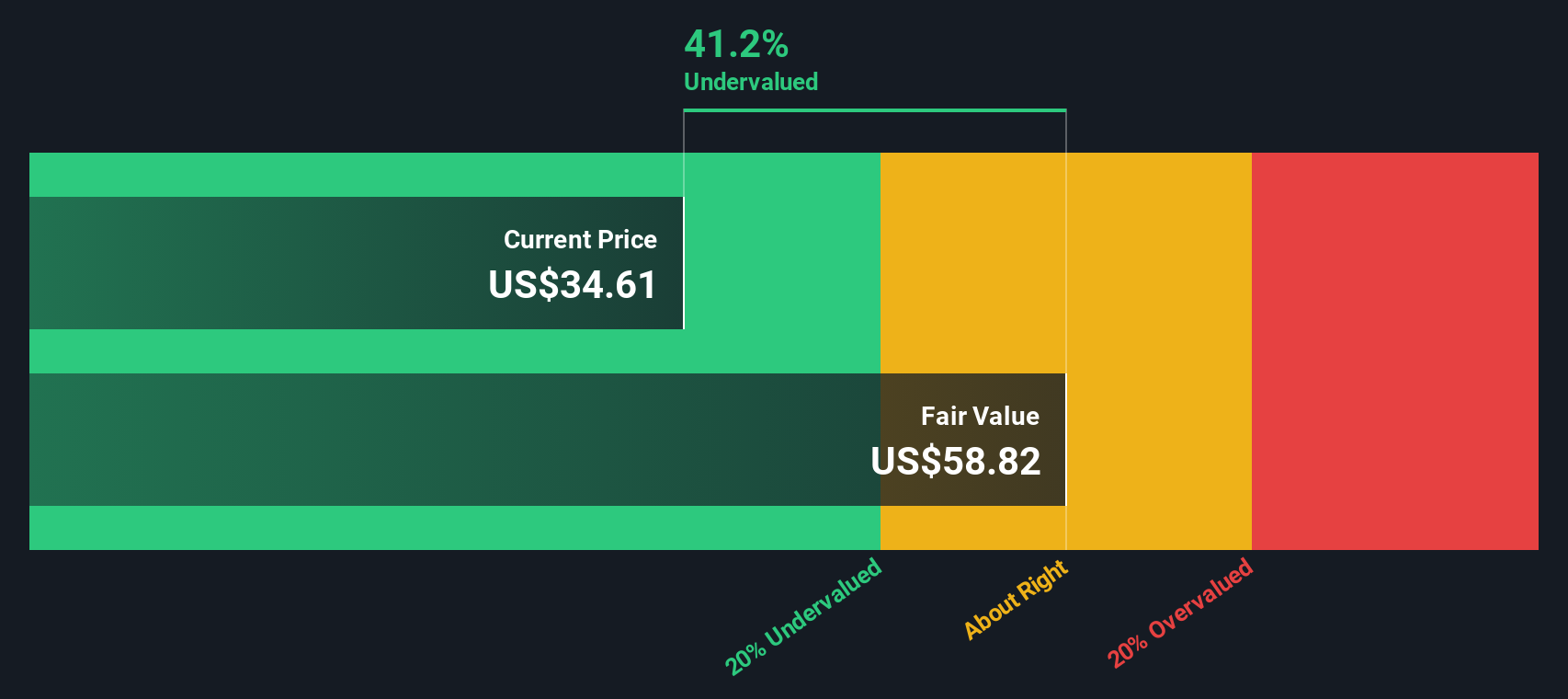

Most Popular Narrative: 12.9% Undervalued

UGI’s most followed narrative pegs fair value at $44.50 versus the recent $38.76 close, framing the stock as modestly undervalued on updated earnings and margin assumptions.

Strategic investments in renewable natural gas (RNG) projects, bonus depreciation potential, and stronger regulatory incentives through recent legislation (e.g., the One Big Beautiful Bill Act) are expected to drive long-term EBITDA growth and improve net margins.

Want to see what powers that $44.50 fair value? The narrative leans heavily on richer margins, steadier revenue and a lower future earnings multiple than many peers. Curious which assumptions do the heavy lifting in this model and how they link to that discount rate of just over 7%? The full narrative lays out the numbers behind that call.

Result: Fair Value of $44.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are clear watchpoints here, including long term pressure on European LPG demand and regulatory or cost headwinds that could squeeze margins and cash flows.

Find out about the key risks to this UGI narrative.

Another View: Cash Flows Paint A Different Picture

While the popular narrative sees UGI as 12.9% undervalued at a $44.50 fair value, our DCF model points the other way. On that cash flow view, fair value sits at $17.58 per share, well below the recent $38.76 price, which screens as overvalued. So which story do you trust more, the earnings path or the cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UGI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 54 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own UGI Narrative

If that fair value story does not quite fit your view, or you would rather put your own assumptions to the test, you can build a custom thesis in minutes and Do it your way.

A great starting point for your UGI research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If UGI has you thinking differently about risk and reward, do not stop here. Use the screener to hunt for other ideas that fit your style.

- Target reliable cash generators by scanning companies with robust payouts through our 13 dividend fortresses that focuses on income strength and resilience.

- Hunt for potential mispriced opportunities using the 54 high quality undervalued stocks to find stocks where quality and price may be out of sync.

- Prioritise sleep at night holdings by checking the 83 resilient stocks with low risk scores and focusing on businesses with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com