Why Materion is on investors’ radar today

Materion (MTRN) has drawn fresh attention after recent trading left the shares with a 1 day return of 0.4%, a past week gain of 5.5% and a past 3 months move of 37.2%.

See our latest analysis for Materion.

Materion’s recent 1 day and 7 day share price returns sit within a stronger trend. The 90 day share price return of 37.18% and 1 year total shareholder return of 65.52% point to building momentum around the US$159.68 stock.

If Materion’s run has you looking for other potential growth stories linked to advanced materials and high tech demand, take a look at our screener of 23 quantum computing stocks as a fresh source of ideas.

With Materion trading at US$159.68, a model-based intrinsic value suggesting roughly a 28.9% discount and analyst targets about 11.7% higher, you have to ask: is there still an entry point here, or is the market already pricing in future growth?

Most Popular Narrative: 5.5% Overvalued

Materion’s most followed narrative pegs fair value at about $151.33, a touch below the recent $159.68 close, which sets up an interesting tension between price and story.

The analysts have a consensus price target of $124.0 for Materion based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analyst's consensus, you would need to believe that by 2028, revenues will be $2.1 billion, earnings will come to $355.2 million, and it would be trading on a PE ratio of 8.8x, assuming you use a discount rate of 7.9%.

It is worth examining how a materials supplier ends up with this kind of earnings curve and profit profile built into the narrative. The revenue assumptions, margin targets, and a rerated P/E multiple all sit under that fair value line. The question is which of those levers really carries the story.

Result: Fair Value of $151.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still have to weigh customer concentration in semiconductors and defense, as well as exposure to beryllium supply and pricing, which could quickly challenge that fair value story.

Find out about the key risks to this Materion narrative.

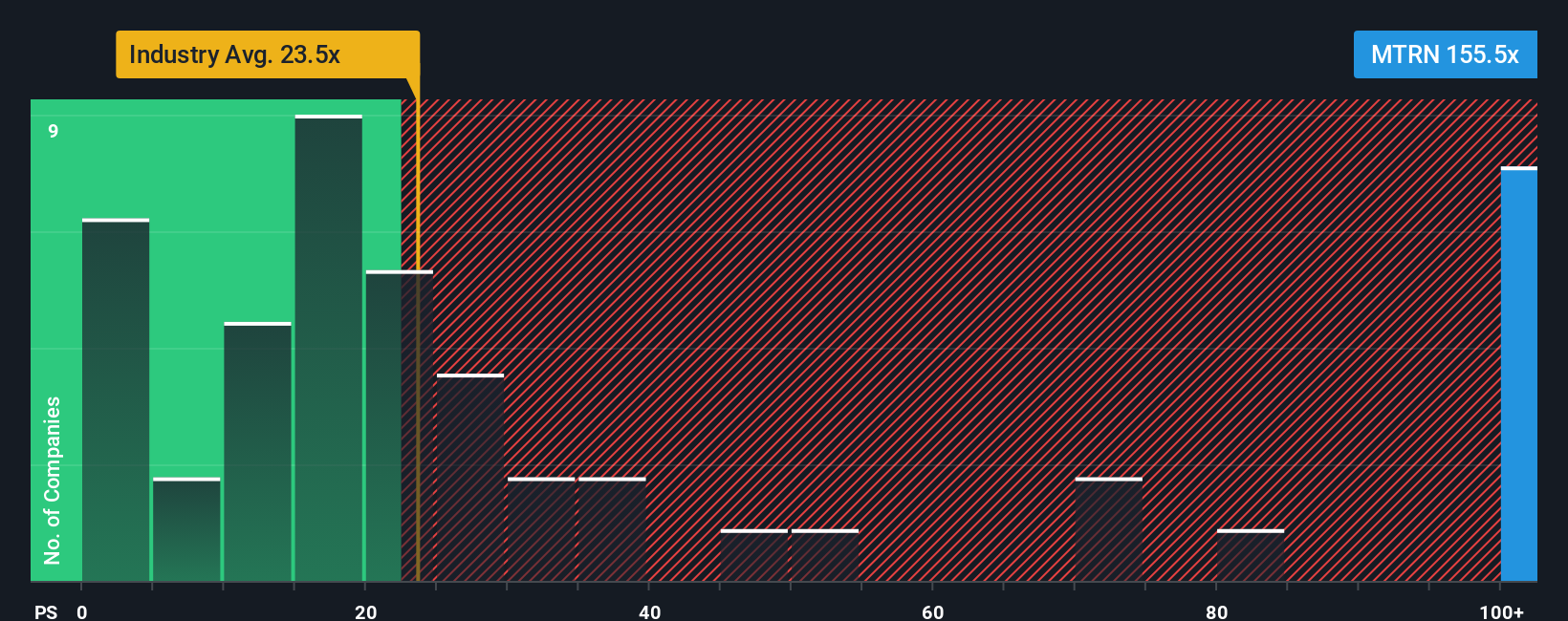

Another Take: Earnings Multiple Sends a Different Signal

Our model based view flags Materion as about 27.9% below fair value, yet the current P/E of 44.2x looks expensive next to the US Metals and Mining average of 26.4x, a peer average of 68.9x, and a fair ratio of 26.5x. Is the market too optimistic about future earnings, or is the model being too cautious?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Materion Narrative

If you look at the numbers and come to a different conclusion, you can stress test every assumption yourself and build a custom view, then Do it your way in under three minutes.

A great starting point for your Materion research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Materion has sharpened your interest, do not stop here. Widen your watchlist with ideas that target quality, resilience and income so you are not relying on one story.

- Target potential value opportunities by checking companies our screener highlights as 53 high quality undervalued stocks with solid fundamentals already in place.

- Prioritise financial strength by focusing on businesses filtered through our solid balance sheet and fundamentals stocks screener (44 results) so you can concentrate on durable balance sheets.

- Boost your income watchlist by reviewing companies in our 13 dividend fortresses that meet a 5%+ yield hurdle with an emphasis on stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com