Quarterly miss, integration costs and deflation in focus

Performance Food Group (PFGC) recently reported quarterly results where profit fell short of market expectations as Cheney Brothers integration costs and deflation in categories like cheese and poultry pressured margins, even as revenue continued to grow.

Management reaffirmed revenue guidance for the upcoming quarter and maintained a positive longer term growth outlook. Analysts noted that higher operating expenses and acquisition related headwinds are currently weighing on near term profitability.

See our latest analysis for Performance Food Group.

Despite the recent earnings miss and higher integration costs, Performance Food Group’s share price has a year to date share price return of 11.30%, while its 1 year total shareholder return is 12.53%. Multi year total shareholder returns suggest that momentum has been building rather than fading.

If this earnings update has you reassessing your watchlist, it could be a good time to scan our 25 power grid technology and infrastructure stocks for other infrastructure linked names that might interest you.

With PFGC trading at $98.00, an implied 19.8% discount to the average analyst target of $117.38 and a modelled intrinsic discount of 29.4%, you have to ask: is there still a genuine entry point here, or is the market already baking in future growth?

Most Popular Narrative: 16.6% Undervalued

With Performance Food Group’s fair value narrative sitting at $117.46 against a last close of $98.00, the current price sits below that story of future cash flows and margins.

The company's robust track record of targeted acquisitions, with a continued focus on disciplined, synergistic M&A and successful integration (as seen with Cheney Brothers and José Santiago), enhances scale, broadens the customer base, and supports higher long-term earnings and cash flow.

Curious what kind of revenue build, margin lift, and earnings power need to line up for that fair value? The narrative leans on meaningful earnings growth assumptions, a richer future profit multiple, and a long runway for foodservice expansion. If you want to see exactly how those ingredients are mixed, the full story is worth a closer read.

Result: Fair Value of $117.46 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if restaurant demand softens further or integration efforts raise costs more than expected, the fair value story the market is watching could be challenged.

Find out about the key risks to this Performance Food Group narrative.

Another Take: High P/E Keeps Things In Check

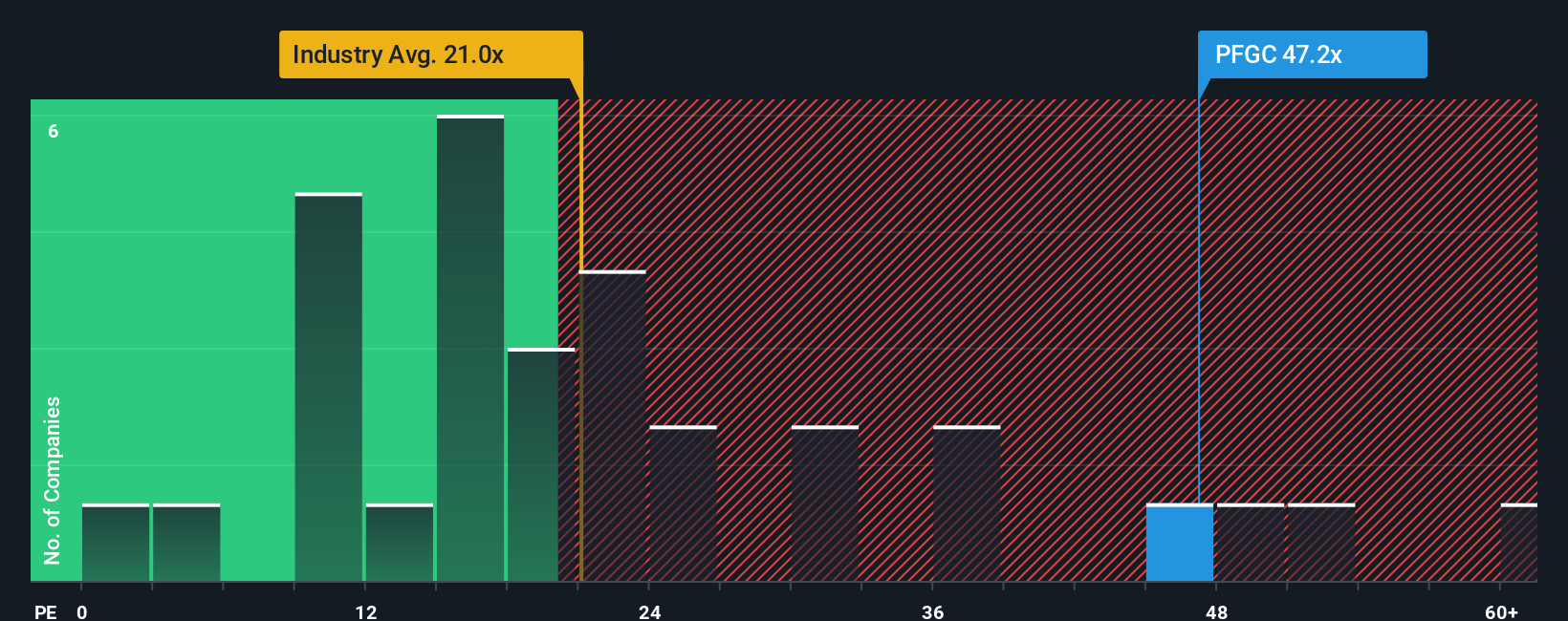

While the fair value work and our DCF view both flag PFGC as trading below estimated worth, the current P/E of 44.6x is almost double the US Consumer Retailing average of 22.9x and above its own 41x fair ratio. That premium can quickly change how comfortable you feel with the upside story.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Performance Food Group Narrative

If you interpret the numbers differently or want to test your own assumptions, you can create a custom view in just a few minutes by starting with Do it your way.

A great starting point for your Performance Food Group research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at a single stock. Use focused stock lists to spot opportunities that others might overlook.

- Target long term compounding potential by scanning companies our screener flags as screener containing 23 high quality undiscovered gems before they attract broad attention.

- Prioritise resilience by checking stocks in the 85 resilient stocks with low risk scores that aim for steadier fundamentals and fewer unpleasant surprises.

- Strengthen your core holdings with companies highlighted in the solid balance sheet and fundamentals stocks screener (44 results) so you can focus on quality when markets get choppy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com