Earnings setback paired with fresh capital returns

J&J Snack Foods (JJSF) has put weaker first quarter results on the table, then followed up with completed and newly authorized share repurchases that are aimed at supporting shareholder value despite softer fundamentals.

See our latest analysis for J&J Snack Foods.

Even after a 3.44% 1 day share price return to US$85.14, J&J Snack Foods is still carrying a weaker 30 day share price return of an 11.03% decline and a 1 year total shareholder return of a 32.78% decline, suggesting momentum has been fading despite the recent dividend affirmation and renewed buyback plans.

If this mix of softer earnings and capital returns has you reassessing your watchlist, it could be a good time to broaden your search with our 23 top founder-led companies.

With J&J Snack Foods trading at US$85.14 and management leaning on dividends and buybacks, the key question is whether the current weakness already reflects its prospects or if the market is still pricing in future growth.

Most Popular Narrative: 23% Undervalued

With J&J Snack Foods last closing at $85.14 against a most-followed fair value of about $110.50, the current pricing sits well below that narrative anchor, putting the underlying growth and margin story in the spotlight.

The company is poised to benefit from increasing demand for convenient, ready-to-eat snacks and higher out-of-home entertainment traffic, as demonstrated by robust performance in foodservice pretzels and Dippin' Dots sales tied to venues and theaters, supporting future revenue growth as consumer routines continue to normalize.

Curious what kind of revenue glide path and margin rebuild are baked into that fair value, and how rich a future earnings multiple the narrative leans on? The full story lays out a detailed mix of moderate growth expectations, firmer profitability assumptions, and a valuation multiple that has been reset lower yet still needs earnings power to do some heavy lifting.

Result: Fair Value of $110.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh risks such as ingredient cost inflation and pressure on the Retail segment, which could challenge the margin and growth assumptions behind that upside story.

Find out about the key risks to this J&J Snack Foods narrative.

Another angle on valuation

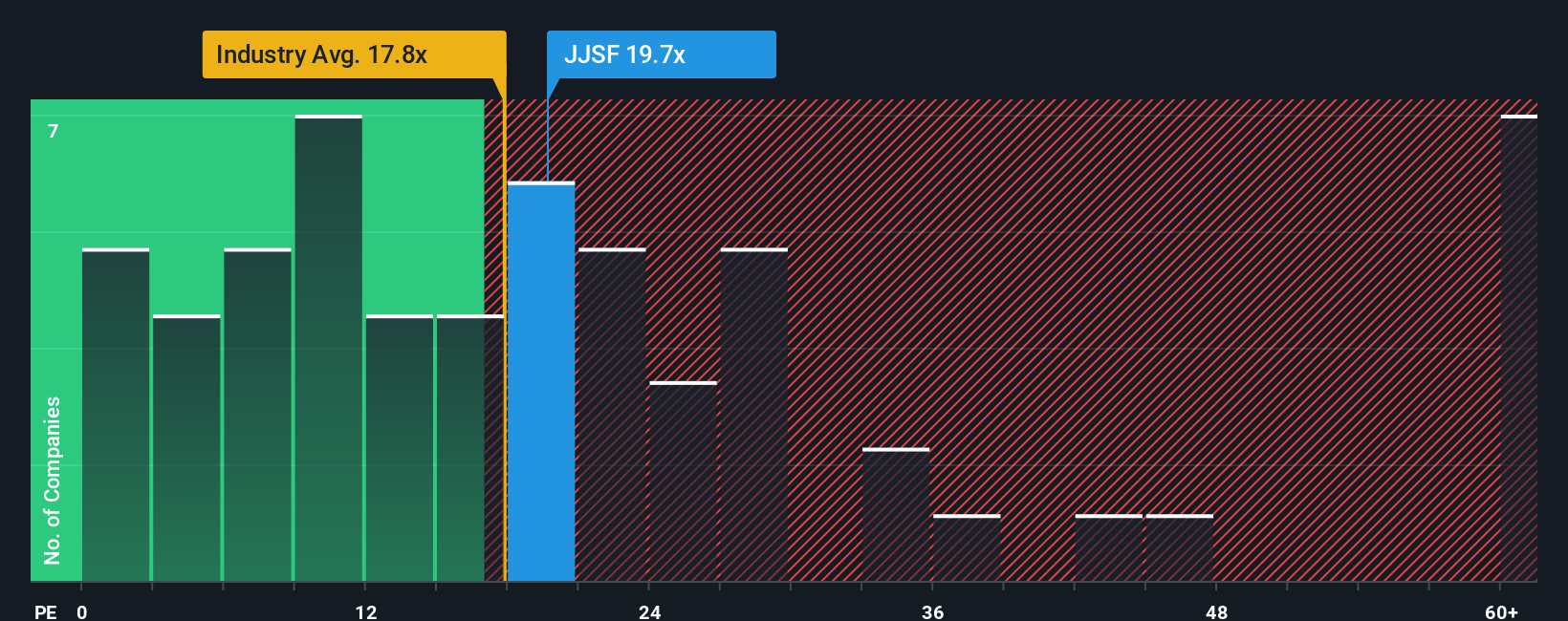

That 23% undervaluation story contrasts with how the market is pricing J&J Snack Foods on earnings today. The current P/E of 26.4x sits above both the US Food industry at 23.9x and the fair ratio of 18.9x, which points to valuation risk if sentiment cools further.

If you prefer to anchor on earnings multiples rather than fair value models, See what the numbers say about this price — find out in our valuation breakdown. can help you see how this sort of gap has played out elsewhere and what other names sit at more restrained levels.

Build Your Own J&J Snack Foods Narrative

If you see the numbers differently or would rather work from your own assumptions, you can quickly build a personalized thesis and test it with our Do it your way.

A great starting point for your J&J Snack Foods research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If J&J Snack Foods is already on your radar, do not stop there. Widen your search now so you are not relying on a single story.

- Spot potential value opportunities early by scanning our 55 high quality undervalued stocks that pairs quality fundamentals with prices that sit below intrinsic estimates.

- Secure income focused ideas through 16 dividend fortresses that highlights companies with higher yields and an emphasis on durability of payouts.

- Prioritize capital protection with our 85 resilient stocks with low risk scores that filters for companies assessed to have more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com