Why Ralph Lauren’s latest earnings and outlook update matter for investors

Ralph Lauren (RL) just delivered quarterly results that topped earlier commitments and lifted its full year revenue and operating margin guidance, while also flagging upcoming margin pressure from higher tariffs and heavier marketing spend.

For you as an investor, that mix of raised full year expectations and near term cost headwinds puts the focus on how durable the company’s current momentum really is across regions, channels, and product categories.

See our latest analysis for Ralph Lauren.

Ralph Lauren’s recent earnings beat, higher full year guidance, and ongoing share repurchases sit against a share price of $342.89, with a 90 day share price return of 2.44% and a 1 year total shareholder return of 29.10%. This suggests momentum that has cooled a little in the very short term but remains strong over multi year periods, including a very large 3 year total shareholder return and 5 year total shareholder return.

If this update has you thinking beyond a single fashion name, it could be a good moment to broaden your horizon with our list of 22 top founder-led companies.

With Ralph Lauren trading at $342.89 against an average analyst price target in the low $400s, along with years of buybacks and upgraded guidance in play, you have to ask: is there still a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 15% Undervalued

Ralph Lauren’s widely followed narrative puts fair value around $404 versus the last close at $342.89, framing the recent guidance upgrade against a richer long term earnings story.

Significant investments in technology, AI-driven inventory management, and automated supply chain operations are driving greater operating efficiencies, setting the stage for improved operating margins and inventory turns as scale increases.

Curious what kind of revenue trajectory and margin profile has to line up for that fair value to hold? The narrative leans on compounding earnings, richer profitability, and a higher future earnings multiple built into its discounted cash flow framework, without assuming extreme growth.

Result: Fair Value of $403.58 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to watch for tariff driven margin pressure and any slowdown in Europe, as both could challenge the higher earnings and valuation narrative.

Find out about the key risks to this Ralph Lauren narrative.

Another View: Is Ralph Lauren Already Priced For Quality?

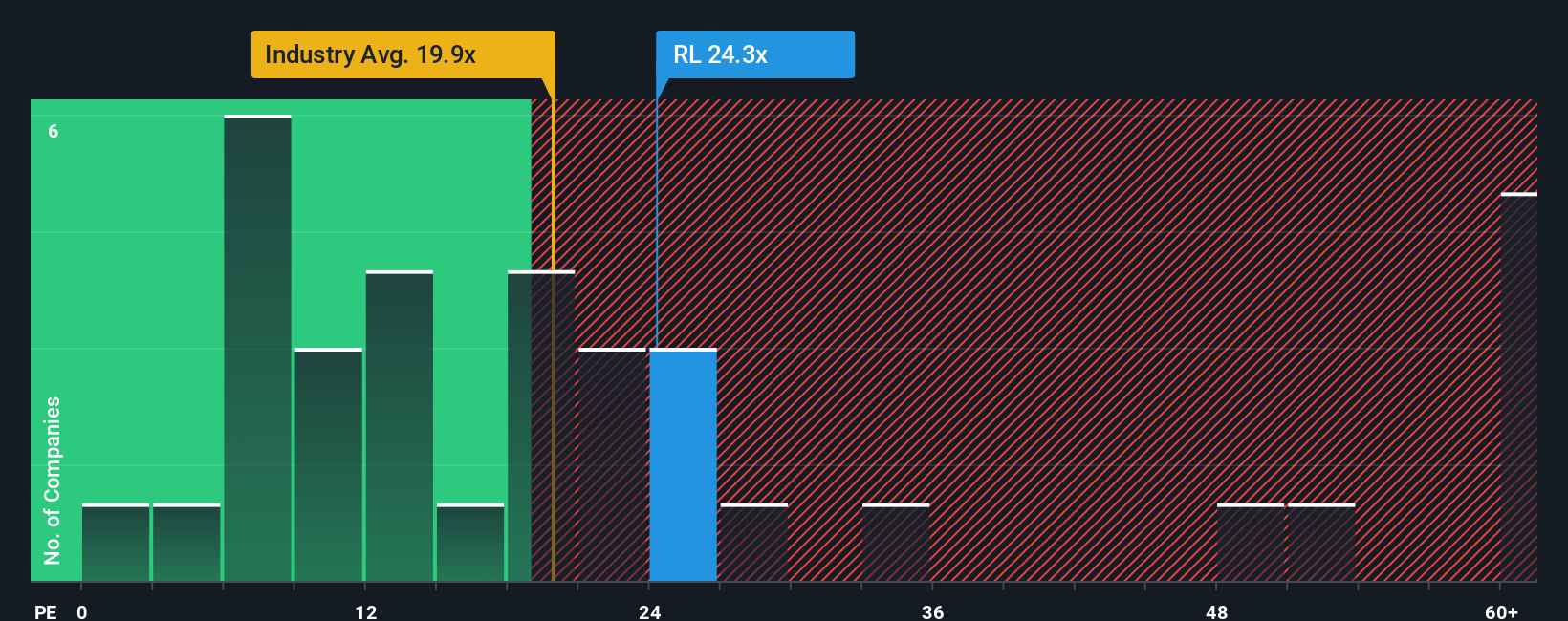

While the popular narrative points to around 15% undervaluation based on a richer earnings story, the picture looks different when you look at the P/E. At 22.6x, Ralph Lauren trades above its 18.6x fair ratio and the US Luxury industry at 20.9x, although below peer average at 38.4x. That mix suggests you are paying a premium for quality rather than getting an obvious bargain, so the real question is whether you think the brand and earnings profile justify staying at the higher end of the range.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Ralph Lauren Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a Ralph Lauren view in minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Ralph Lauren.

Looking for more investment ideas?

If Ralph Lauren has sharpened your thinking, do not stop here. Use the Simply Wall St screener to spot other opportunities that fit your style in minutes.

- Target potential mispricings by reviewing companies our tools highlight as 52 high quality undervalued stocks that may warrant a closer look.

- Strengthen your income focus by scanning for 14 dividend fortresses that could help anchor a portfolio with regular cash returns.

- Limit surprises by filtering for 82 resilient stocks with low risk scores that align with a steadier, more controlled approach to building wealth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com