Unum Group (UNM) just rolled out a new share repurchase plan of up to $1 billion, a strong signal about how management views the stock, even as short interest has recently ticked higher.

See our latest analysis for Unum Group.

That confidence backed by the $1 billion buyback comes on top of a steady climb, with the share price at $77.91 and a solid year to date share price return. The three year and five year total shareholder returns suggest long term momentum is very much intact.

If this kind of capital return story has your attention, it could be a great moment to look beyond insurance and explore fast growing stocks with high insider ownership for other potential standouts.

But with Unum trading below analyst targets and our estimates of intrinsic value, yet facing rising short interest, is the market overlooking a value opportunity here or already baking in the company’s future growth?

Most Popular Narrative: 16.3% Undervalued

With Unum Group closing at $77.91 against a narrative fair value near the low $90s, the story frames the stock as mispriced strength.

The analysts have a consensus price target of $93.077 for Unum Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $108.0, and the most bearish reporting a price target of just $79.0.

Curious how relatively modest revenue growth, slightly lower margins, and shrinking share count still add up to a richer future earnings multiple than today? The narrative walks through a step by step roadmap from current profits to that higher valuation bar, including the discount rate and the exact earnings level it expects Unum to hit along the way.

Result: Fair Value of $93.08 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent elevated benefit ratios or renewed long term care reserve pressures could quickly undermine today’s margin assumptions and derail the undervaluation narrative.

Find out about the key risks to this Unum Group narrative.

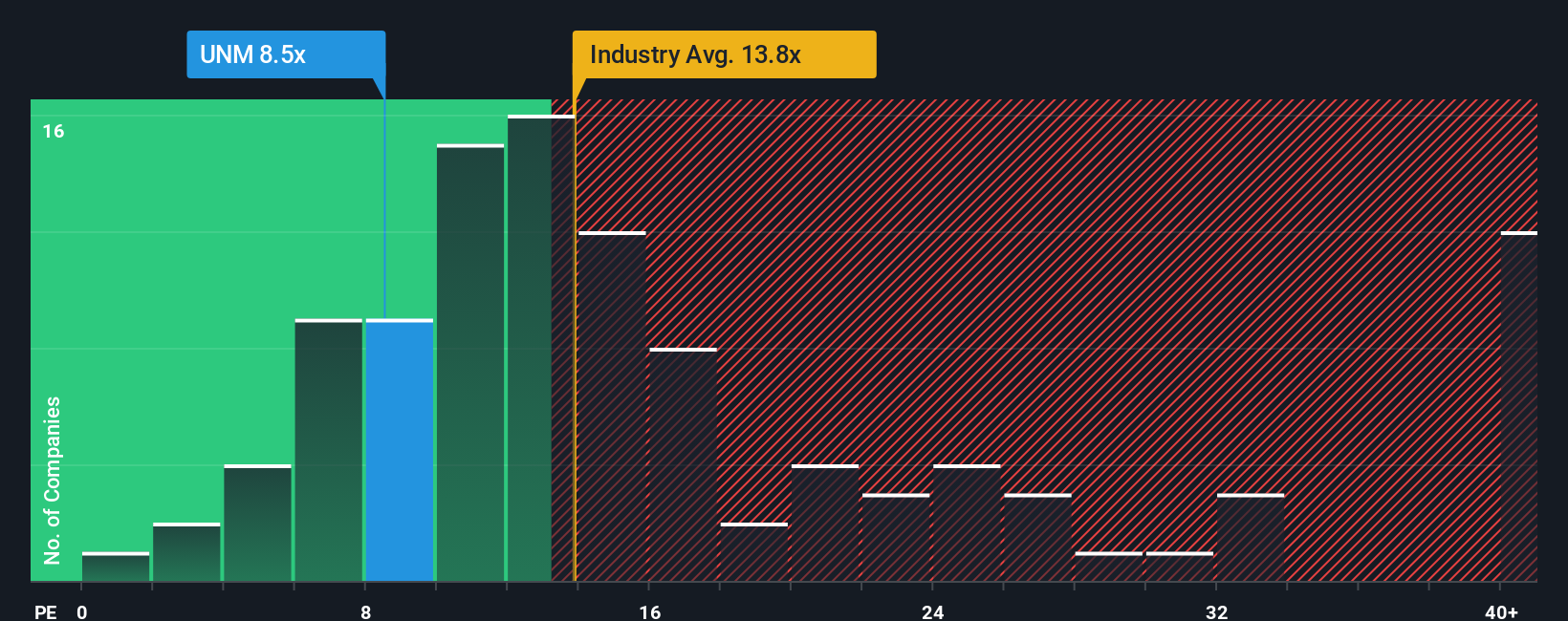

Another View: Market Ratios Flash Caution

While the narrative fair value suggests upside, the market ratio picture is less generous. Unum trades on a 14.3x earnings multiple, richer than both peers at 9.5x and the insurance industry at 13.4x, even though our fair ratio points higher at 18.8x.

This gap implies investors already pay a premium versus competitors. However, the price could still climb if sentiment ever matches that fair ratio benchmark, raising the stakes on any earnings wobble. Is this a smart value entry or a crowded quality trade with limited room for error?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Unum Group Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in minutes: Do it your way.

A great starting point for your Unum Group research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop with a single opportunity when you can quickly compare dozens of high potential setups tailored to your strategy using the Simply Wall Street Screener.

- Capture potential multi baggers early by scanning these 3640 penny stocks with strong financials that pair tiny market caps with real financial strength instead of speculation alone.

- Position ahead of the next tech wave by targeting these 26 AI penny stocks that blend scalable business models with meaningful exposure to artificial intelligence.

- Identify quality at potentially attractive entry points by filtering for these 908 undervalued stocks based on cash flows where robust cash flows support a margin of safety.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com