- Earlier this week, CNO Financial Group reported strong third-quarter 2025 operating earnings, highlighted by a large earnings-per-share beat and a surge in new premium production, while also exiting lower-growth fee services in its Worksite business to refocus on core insurance offerings.

- At the same time, Jefferies and other analysts turned more positive on CNO’s outlook, pointing to improving return on equity supported by new business growth, capital optimization, and continued dividends and share buybacks as reasons for greater confidence in the company’s direction.

- Next, we’ll examine how Jefferies’ ROE-focused upgrade and CNO’s exit from fee services could reshape the company’s investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

CNO Financial Group Investment Narrative Recap

To own CNO today, you need to believe its middle‑income retirement and insurance franchise can convert modest premium growth into better returns on equity, even as competition and regulation remain live risks. The latest earnings beat and Jefferies’ upgrade reinforce return on equity as the key near term catalyst, while recent insider selling and CNO’s history of flat premium demand may temper enthusiasm but do not fundamentally alter that core thesis.

The most relevant recent development is CNO’s strong Q3 2025 operating earnings, with earnings per share of US$1.29 versus a US$0.92 forecast and higher revenue, alongside a move to exit lower growth Worksite fee services. Together, these updates focus attention on how a more streamlined, insurance centric business mix could support the return on equity improvement that Jefferies and other analysts are now highlighting as central to CNO’s story.

Yet against this improving return story, investors should be aware of the recent pattern of insider selling and what it could mean for …

Read the full narrative on CNO Financial Group (it's free!)

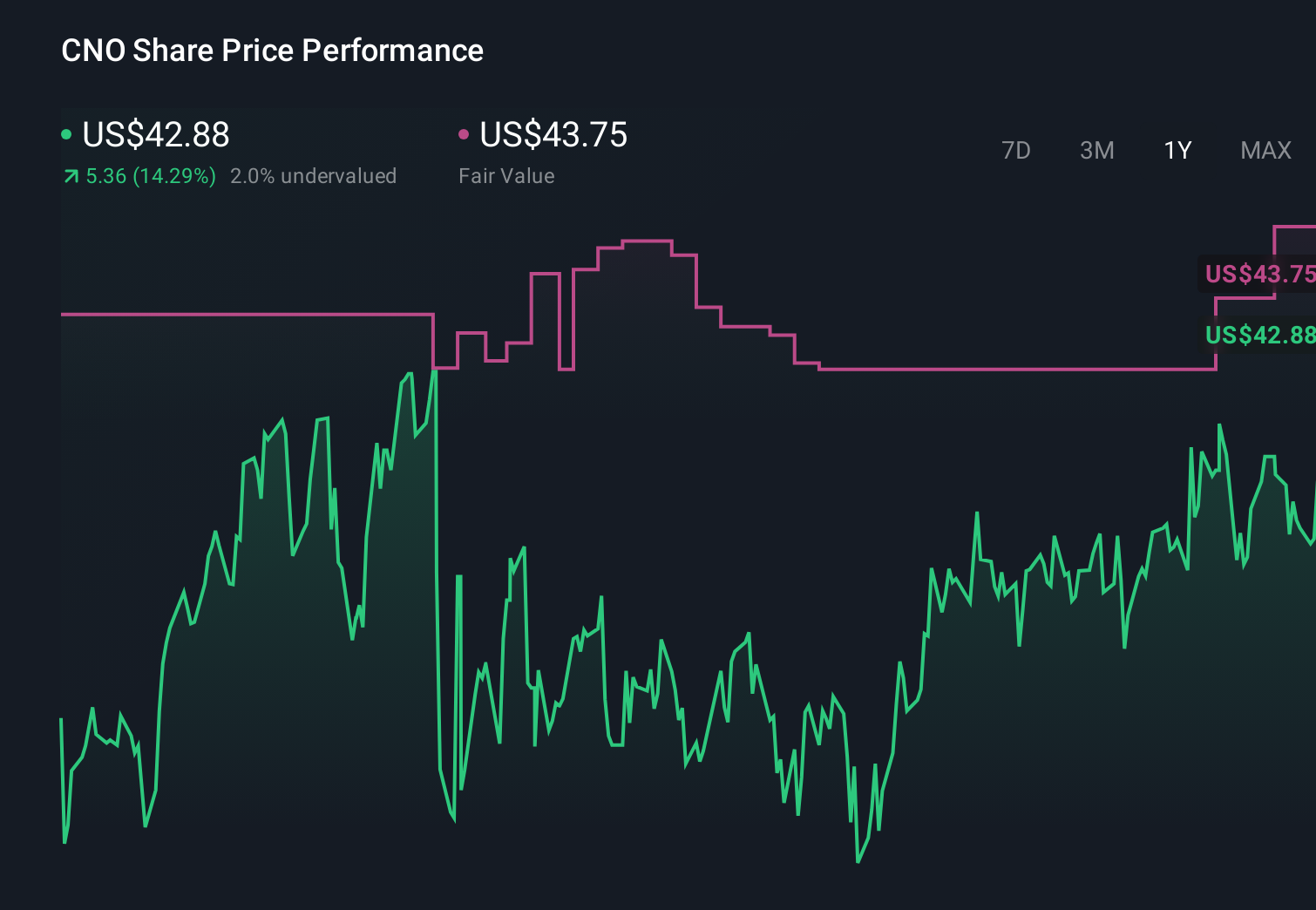

CNO Financial Group's narrative projects $4.3 billion revenue and $432.2 million earnings by 2028. This implies a 0.8% yearly revenue decline and a $143.5 million earnings increase from $288.7 million today.

Uncover how CNO Financial Group's forecasts yield a $43.75 fair value, in line with its current price.

Exploring Other Perspectives

The Simply Wall St Community’s single fair value estimate of US$43.75 shows how individual views can cluster tightly, even when opinions often differ widely. Set against analysts’ focus on return on equity improvements and modest premium growth, this gives you another lens on how expectations for CNO’s performance might evolve.

Explore another fair value estimate on CNO Financial Group - why the stock might be worth as much as $43.75!

Build Your Own CNO Financial Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CNO Financial Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CNO Financial Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNO Financial Group's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 33 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com