- If you are wondering whether Bunge Global at around $94 is still a smart buy or if the easy money has already been made, you are not the only one asking that question. This article will dig into what the numbers really say about its value.

- The stock has been a steady compounder, up 21.7% year to date and 67.5% over five years, even though it has cooled slightly with a 2.2% dip over the last week and a flat 0.5% move over the past month.

- Recent headlines have focused on Bunge Global's role in global agricultural supply chains, including its progress integrating past acquisitions and expanding its presence in key export regions. This helps explain why investors have been willing to pay up for the stock. At the same time, ongoing geopolitical tensions and shifting trade flows have kept sentiment mixed and added nuance to those price swings.

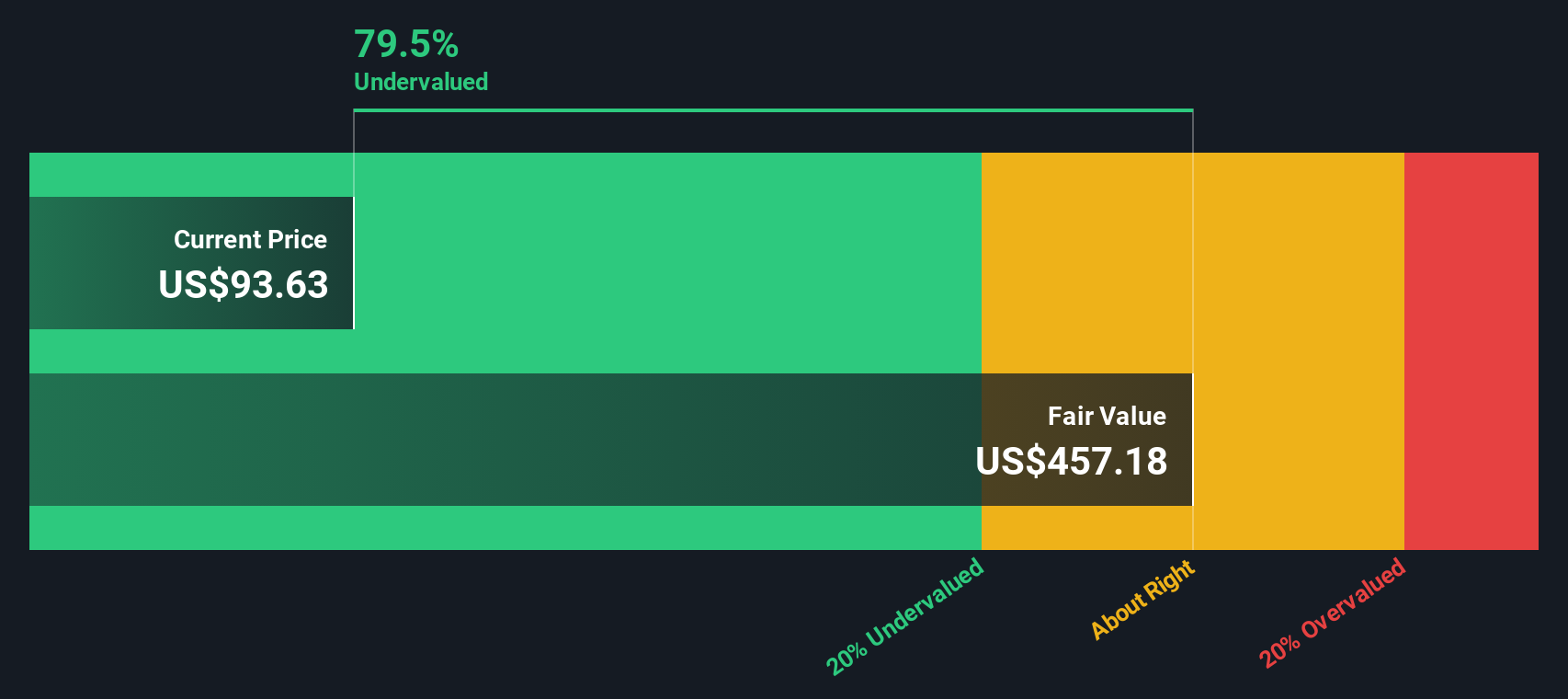

- Right now Bunge Global scores a solid 5/6 on our valuation checks, suggesting it looks undervalued on most of the metrics we track. Next we will break down the different valuation methods behind that number before finishing with a more holistic way to think about what the stock is really worth.

Approach 1: Bunge Global Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth today by projecting its future cash flows and discounting them back into present dollar terms. For Bunge Global, the 2 Stage Free Cash Flow to Equity model starts with the latest twelve month Free Cash Flow of around $0.78 billion in the red, then assumes a recovery and growth path based on analyst forecasts and longer term extrapolations.

Analysts see Free Cash Flow reaching about $1.99 billion by 2026 and $2.50 billion by 2027, with Simply Wall St extending this trajectory to roughly $4.62 billion by 2035. When all those projected cash flows are discounted back, the model arrives at an estimated fair value of about $456 per share.

Compared with the current share price near $94, the DCF suggests Bunge Global is trading at roughly a 79.3% discount to its intrinsic value. This implies the market is pricing in a far weaker future than this model assumes.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Bunge Global is undervalued by 79.3%. Track this in your watchlist or portfolio, or discover 914 more undervalued stocks based on cash flows.

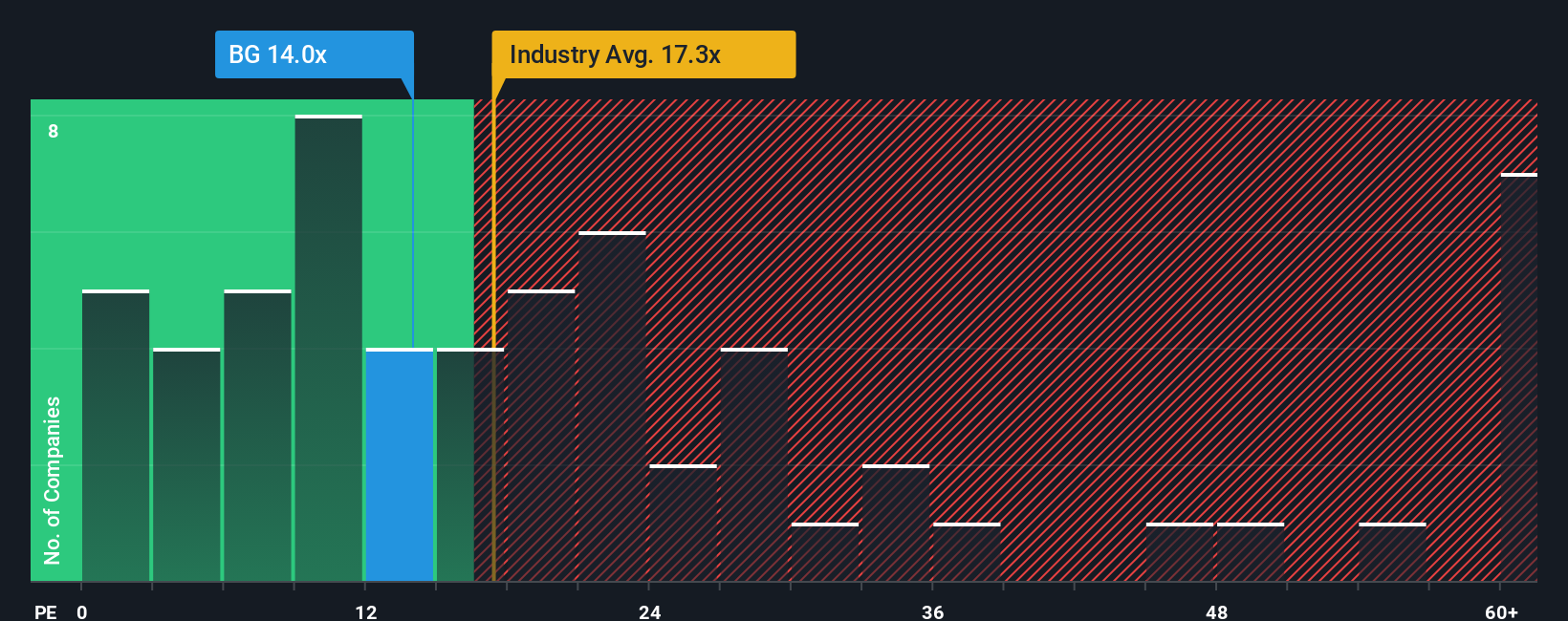

Approach 2: Bunge Global Price vs Earnings

For profitable companies like Bunge Global, the price to earnings, or PE, ratio is a useful way to gauge how much investors are paying for each dollar of current earnings. In general, faster expected growth and lower perceived risk justify a higher PE, while slower growth or greater uncertainty usually cap what the market is willing to pay.

Bunge Global currently trades on a PE of about 13.8x, which sits well below the wider Food industry average of roughly 20.4x and the peer group average near 27.6x. At first glance, that discount suggests the market is applying a fairly conservative view to its earnings, despite its strategic role in global agriculture.

Simply Wall St’s Fair Ratio framework goes a step further by calculating what PE you would reasonably expect for Bunge Global, given its earnings growth prospects, profit margins, industry, market cap and risk profile. That Fair Ratio comes out at around 34.4x, compared with the current 13.8x. On this basis, the stock appears meaningfully undervalued on earnings, even allowing for sector and risk considerations.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

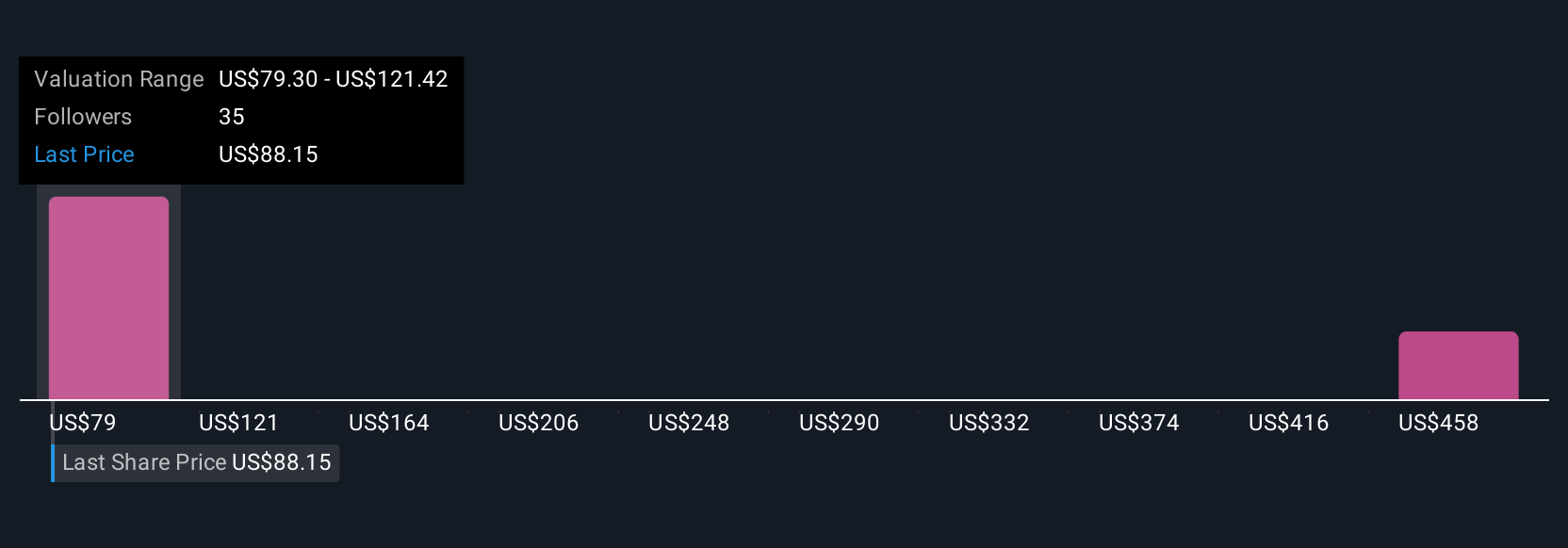

Upgrade Your Decision Making: Choose your Bunge Global Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply the stories investors tell about a company, backed by their assumptions for future revenue, earnings, margins and therefore fair value.

Instead of only looking at static ratios like PE, a Narrative connects three pieces together: the business story you believe, the financial forecast that follows from that story, and the fair value that drops out of that forecast, so you can see clearly whether the current price looks attractive or stretched.

On Simply Wall St, Narratives are an easy, accessible tool on the Community page used by millions of investors. Each Narrative turns someone’s view of a company into a transparent set of numbers that can be compared directly with today’s share price to help guide investment decisions.

Because Narratives update dynamically as new information comes in, such as Bunge Global’s buybacks, index removal or changing growth and margin expectations, you can see why one Narrative might justify a fair value near the most bullish target of $100 while another, more cautious view, lands closer to the most bearish $74, and then decide which story you find more convincing.

Do you think there's more to the story for Bunge Global? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com