- On July 29, Unum Group reported second quarter 2025 earnings that fell short of analyst expectations, and management updated its 2025 share repurchase guidance to the upper end of the prior US$500 million–US$1.00 billion range.

- An interesting insight is that while operational results were softer, Unum’s willingness to accelerate share buybacks highlights management’s focus on capital return, even amid earnings pressure.

- We'll examine how Unum's raised share repurchase outlook could influence the company's investment narrative and future capital allocation priorities.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

Unum Group Investment Narrative Recap

To be a Unum Group shareholder, you need confidence in the company’s ability to manage benefit ratios, drive premium growth through employer-sponsored benefits, and translate operational scale into consistent returns. The recent softer quarterly earnings do not appear to materially shift the short-term catalysts or primary risks; the main focus remains on consistent capital returns versus volatility in core insurance lines and the legacy LTC block.

Among recent announcements, the updated guidance to repurchase shares at the upper end of the US$500 million to US$1.00 billion range stands out. This move underscores the company’s continued emphasis on shareholder returns even as earnings soften, and may provide some short-term support to earnings per share, though it does not directly address the core risks tied to claims experience in group insurance or the Closed Block.

In contrast, investors should be aware that higher-than-expected claim costs in group insurance could...

Read the full narrative on Unum Group (it's free!)

Unum Group's forecast projects $14.5 billion in revenue and $1.6 billion in earnings by 2028. This outlook implies a 4.0% annual revenue growth rate and a $0.1 billion increase in earnings from the current $1.5 billion.

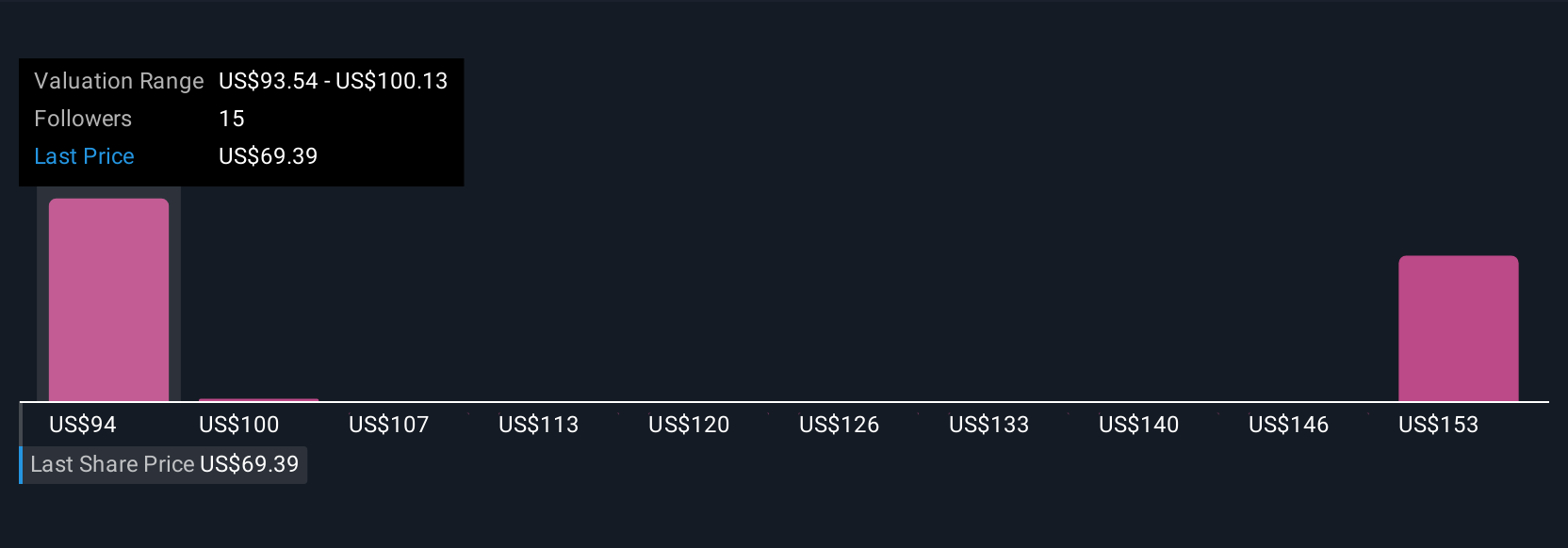

Uncover how Unum Group's forecasts yield a $93.08 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Four community members from Simply Wall St provided fair value estimates for Unum Group, ranging from US$93 to US$159 per share, highlighting wide differences in outlook. While some see significant undervaluation, persistently elevated benefit ratios in core group insurance remain a central concern with the potential to affect future earnings and capital flexibility.

Explore 4 other fair value estimates on Unum Group - why the stock might be worth just $93.08!

Build Your Own Unum Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Unum Group research is our analysis highlighting 6 key rewards that could impact your investment decision.

- Our free Unum Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Unum Group's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find companies with promising cash flow potential yet trading below their fair value.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com