- Travel + Leisure Co. recently completed a US$500 million private offering of 6.125% senior secured notes due 2033, with proceeds allocated to refinancing higher-rate debt and strengthening its balance sheet.

- This move reflects proactive debt management aimed at reducing interest costs and may enhance financial flexibility for ongoing operations and growth initiatives.

- We’ll explore how Travel + Leisure’s major debt refinancing could reshape its investment outlook and support long-term earnings stability.

Find companies with promising cash flow potential yet trading below their fair value.

Travel + Leisure Investment Narrative Recap

To own Travel + Leisure shares, you need to be confident in the company’s ability to grow its vacation ownership and travel membership businesses despite industry consolidation and shifting consumer trends. The recent US$500 million debt refinancing at 6.125% may help reduce short-term interest expenses, but its impact on near-term revenue drivers and earnings remains limited, as the main catalyst continues to be sustained demand for timeshare products and membership growth; the biggest risk is ongoing pressure in the Travel and Membership segment from evolving market structures and competition, which could weigh on total company performance if not addressed.

One relevant recent announcement is the company’s regular cash dividend of US$0.56 per share, declared just days after the refinancing, which maintains a steady shareholder return. This underscores management’s intent to balance capital allocation between strengthening the balance sheet and rewarding investors, especially as demand trends and ongoing business initiatives remain the focal point for future growth.

Yet, it’s important for investors to note, in contrast, that persistent structural headwinds in the Travel and Membership segment could continue to pose challenges for overall growth if they are not resolved...

Read the full narrative on Travel + Leisure (it's free!)

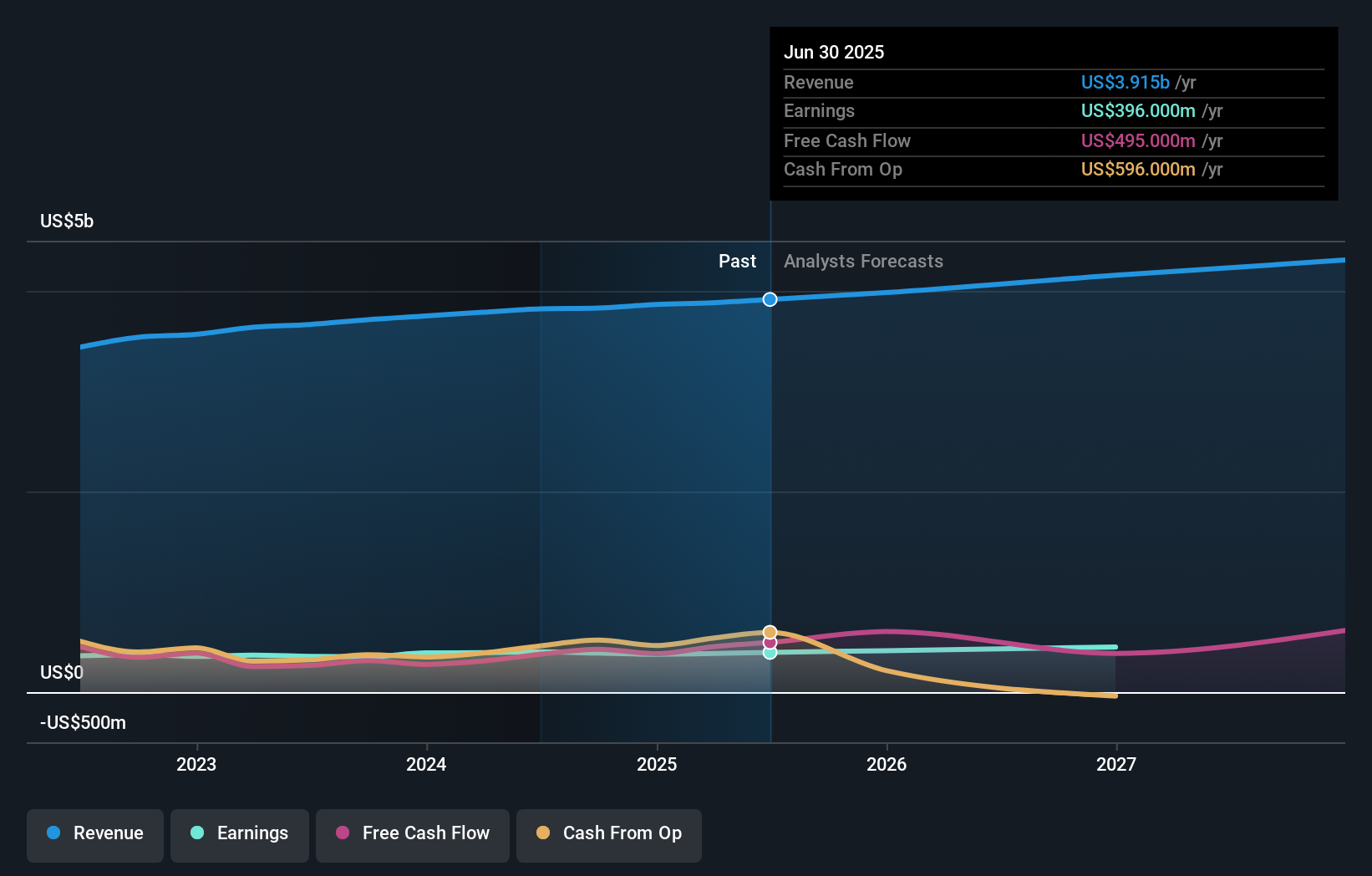

Travel + Leisure's projections indicate $4.4 billion in revenue and $509.8 million in earnings by 2028. This outlook relies on 3.9% annual revenue growth and a $113.8 million increase in earnings from the current $396.0 million.

Uncover how Travel + Leisure's forecasts yield a $67.67 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members provided four fair value estimates for Travel + Leisure, ranging from US$43.13 to US$61,186.95. While some expect substantial upside, ongoing competition in vacation ownership models may continue to influence company prospects, so consider how different assumptions affect the business outlook.

Explore 4 other fair value estimates on Travel + Leisure - why the stock might be a potential multi-bagger!

Build Your Own Travel + Leisure Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Travel + Leisure research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Travel + Leisure research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Travel + Leisure's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com