- Crown Holdings recently reported strong second quarter results, surpassing analysts' estimates on revenue, EBITDA, and adjusted operating income.

- This performance highlights how eco-friendly packaging trends are shaping the industry and driving innovation among packaging suppliers.

- We'll now examine how Crown Holdings' better-than-expected quarterly performance may influence its investment narrative and future outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Crown Holdings Investment Narrative Recap

To be a Crown Holdings shareholder, you need to believe that the consumer transition to eco-friendly packaging fuels consistent long-term demand, and that the company’s capacity expansion and product innovation can offset industry headwinds. The recent earnings beat reflects strong underlying demand, but it does not materially shift the main short-term catalyst, rising beverage and food can volumes, nor does it fully address the biggest risk of geographic concentration and margin pressures in regions like Asia and Europe.

A recent announcement about the new high-speed production line in Brazil stands out, as it directly links to Crown’s strategy to expand capacity in growth markets. Increasing output from the Ponta Grossa plant should help capture higher can volumes if demand holds, supporting the main short-term catalyst referenced above, though global market uncertainties remain crucial to monitor.

On the other hand, investors should also pay close attention to the persistent risk of margin pressure in Crown’s Asian and European operations, where...

Read the full narrative on Crown Holdings (it's free!)

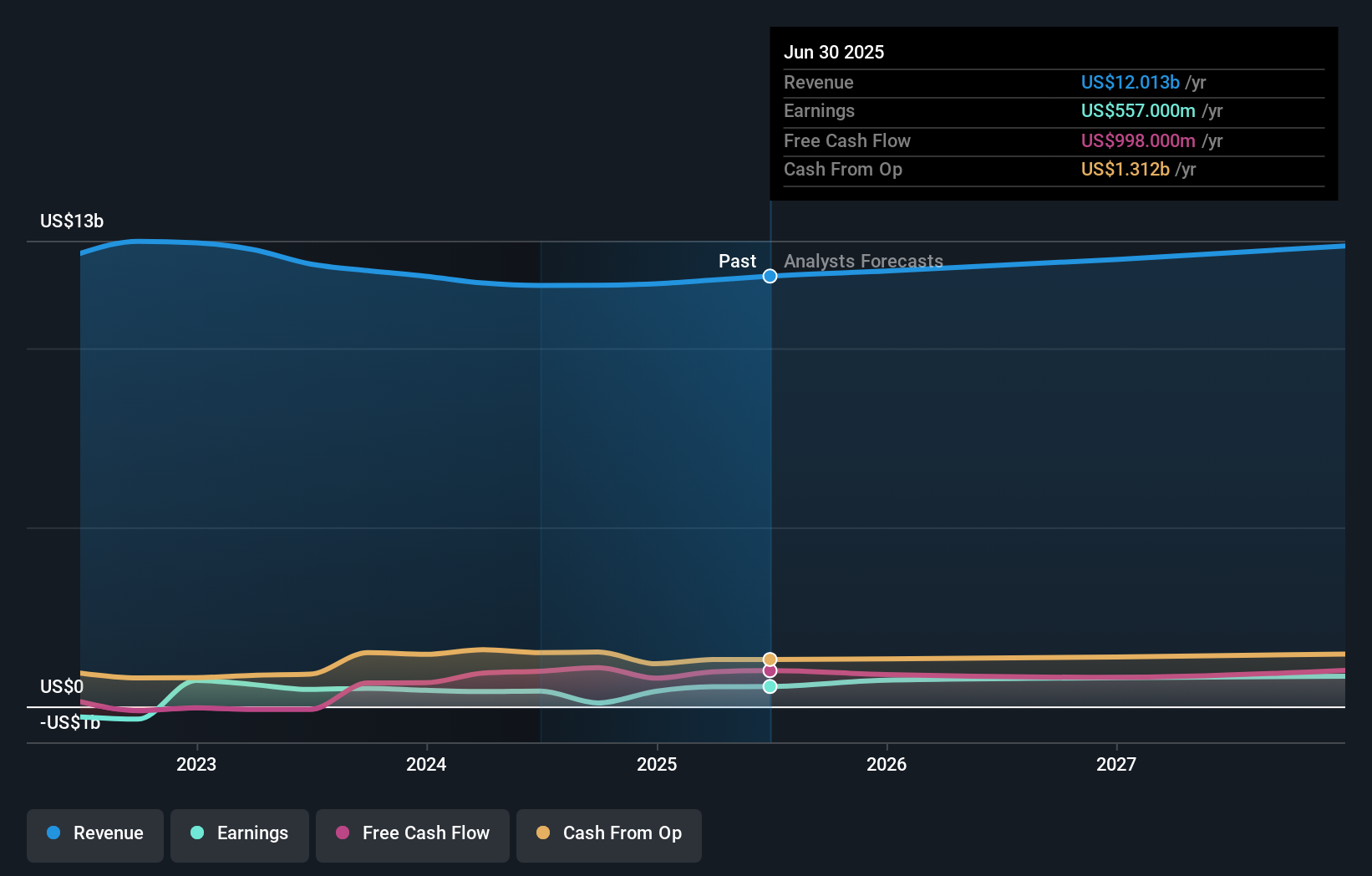

Crown Holdings' outlook envisions $13.3 billion in revenue and $886.4 million in earnings by 2028. This rests on a projected 3.3% annual revenue growth rate and a $329.4 million increase in earnings from the current $557.0 million.

Uncover how Crown Holdings' forecasts yield a $123.36 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members provided 2 fair value estimates for Crown Holdings, ranging from US$123.36 to US$221.01 per share. While opinions are broad, many watch ongoing investments in capacity expansion as a key influence for long-term outcomes.

Explore 2 other fair value estimates on Crown Holdings - why the stock might be worth just $123.36!

Build Your Own Crown Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Crown Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Crown Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crown Holdings' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com