- Earlier in August 2025, Ball Corporation reported a strong second quarter with sales of US$3.34 billion and net income of US$212 million, and completed a significant share buyback, repurchasing nearly 13.9 million shares for US$731.35 million as part of its ongoing capital return program.

- The company raised its full-year 2025 guidance for comparable diluted earnings per share growth to 12%–15%, highlighting improved operational efficiency and confidence in sustained growth momentum.

- We'll explore how Ball's raised earnings outlook and robust buyback activity may reshape the investment narrative moving forward.

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Ball Investment Narrative Recap

For shareholders, the core investment case in Ball centers on continued demand for recyclable aluminum packaging and operational gains driving earnings growth. The strong Q2 results and continued share buybacks support near-term confidence, but do not eliminate risks around input cost volatility, which remains the biggest variable that could disrupt earnings momentum in the short term.

The most relevant recent announcement is Ball’s completion of its share repurchase program, retiring nearly 4.89% of outstanding shares for US$731.35 million. While this signals a commitment to shareholder returns, catalysts like growing market demand for sustainable packaging remain far more critical to the company’s medium-term growth story.

Yet, despite Ball’s improved outlook, input cost swings, particularly for aluminum, remain a variable investors need to watch...

Read the full narrative on Ball (it's free!)

Ball's outlook anticipates $14.2 billion in revenue and $1.1 billion in earnings by 2028. This assumes an annual revenue growth rate of 4.6% and a $519 million increase in earnings from the current $581.0 million.

Uncover how Ball's forecasts yield a $64.29 fair value, a 17% upside to its current price.

Exploring Other Perspectives

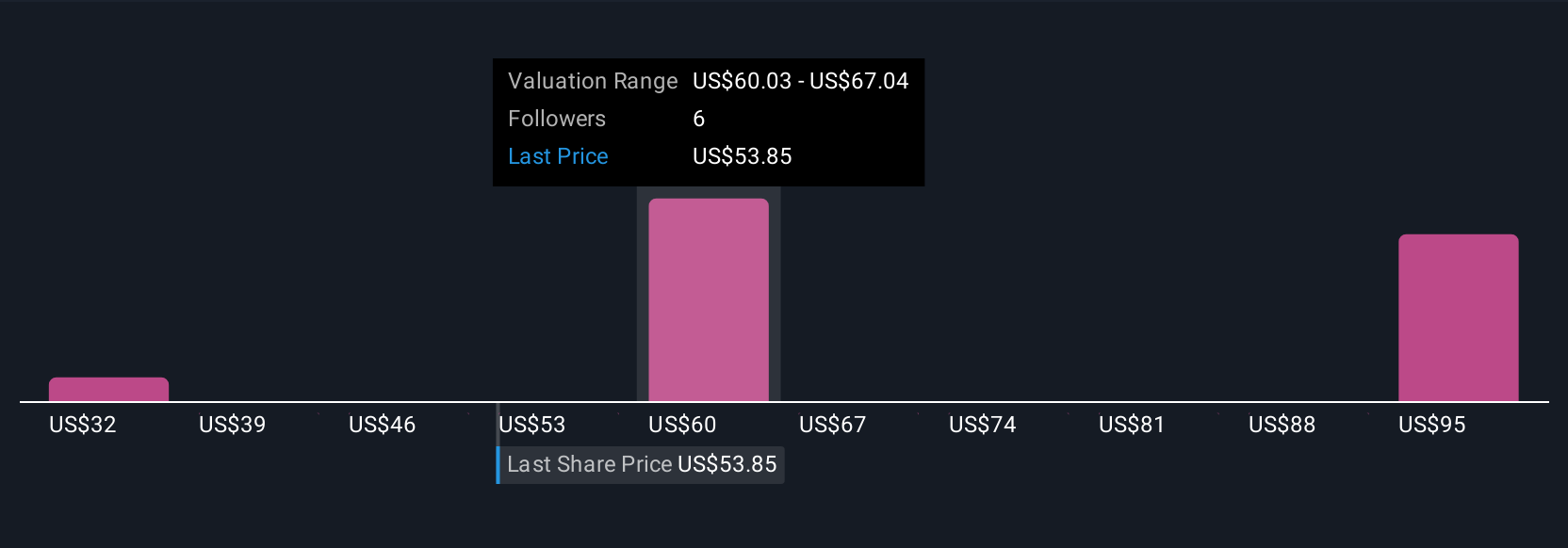

Three fair value estimates from the Simply Wall St Community range from US$32 to US$101.85, highlighting widespread differences on Ball’s potential. With input cost fluctuations still a known risk, take time to explore several viewpoints before forming your outlook.

Explore 3 other fair value estimates on Ball - why the stock might be worth as much as 86% more than the current price!

Build Your Own Ball Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ball research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Ball research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ball's overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com