- Coty Inc. announced the resignation of board member Johannes Huth, effective July 14, 2025, alongside expectations of revenue declines in its upcoming fourth-quarter fiscal 2025 report due to challenges in China, Travel Retail Asia, and U.S. Consumer Beauty.

- Despite these headwinds, Coty's ongoing investments in expanding their prestige fragrance portfolio and cost-saving efforts are anticipated to cushion margins, even though analysts expect continued earnings pressure from increased advertising spending and currency fluctuations.

- We'll explore how the anticipated revenue softness, particularly in key Asian and U.S. markets, could influence Coty's investment narrative and outlook.

The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Coty Investment Narrative Recap

To own shares in Coty right now, you need to believe that the company’s push into prestige fragrances and operational efficiencies can offset the revenue pressure in its critical Asian and U.S. beauty markets. The resignation of Johannes Huth is not expected to materially affect Coty’s most immediate catalyst, which involves weathering current headwinds and aiming for margin improvement, but earnings risk due to spending and currency swings remains a concern.

Among recent announcements, Coty’s launch of Origen, a new consumer beauty fragrance brand, stands out as most relevant given the spotlight on product innovation as a linchpin for demand recovery. Fresh product launches like Origen are directly related to the company’s efforts to stimulate growth and reinforce its positioning in the segments where demand has softened.

Yet, in contrast to new innovation, inventory and replenishment challenges in the U.S. are something investors should watch out for...

Read the full narrative on Coty (it's free!)

Coty's narrative projects $6.3 billion revenue and $443.4 million earnings by 2028. This requires 1.6% yearly revenue growth and an $852.6 million earnings increase from -$409.2 million.

Uncover how Coty's forecasts yield a $6.41 fair value, a 32% upside to its current price.

Exploring Other Perspectives

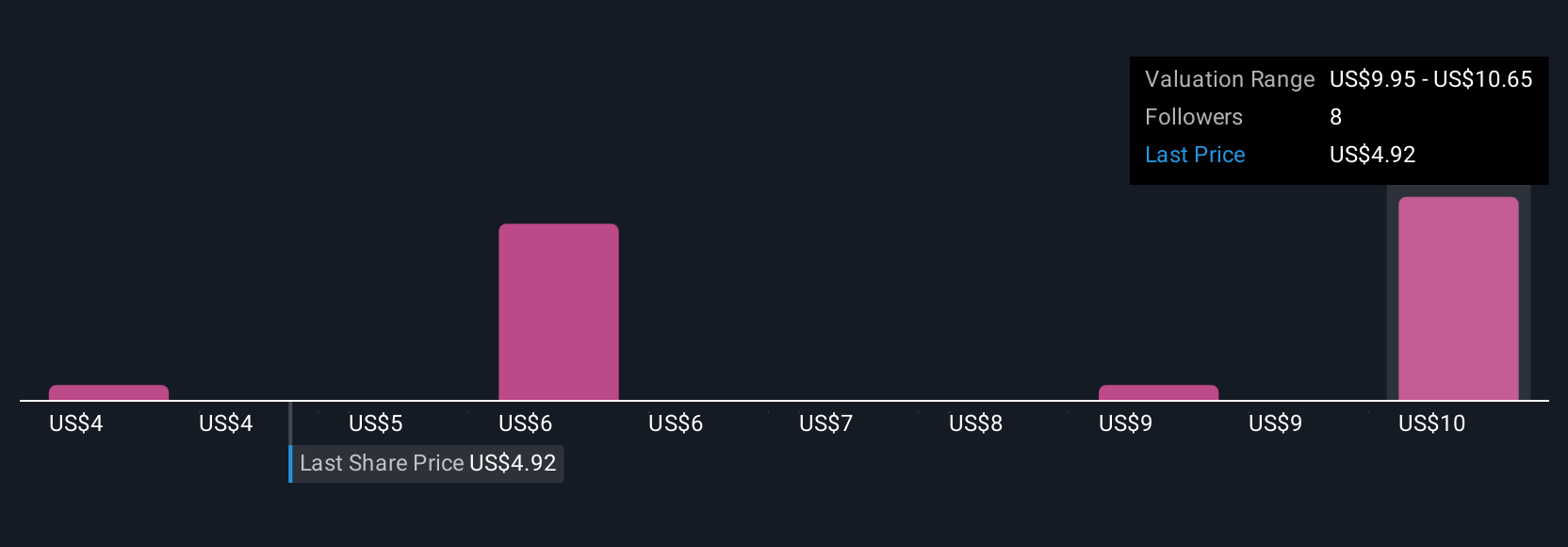

Simply Wall St Community members provided 5 fair value estimates for Coty shares ranging from US$3.69 to US$10.50. While opinions on valuation differ, the company’s exposure to continued softness in China and competition in the U.S. will shape the debate on future performance.

Explore 5 other fair value estimates on Coty - why the stock might be worth 24% less than the current price!

Build Your Own Coty Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Coty research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Coty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Coty's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com