- Sealed Air Corporation recently reported its second quarter 2025 earnings, revealing quarterly sales of US$1.34 billion and the appointment of Kristen Actis-Grande as the incoming Chief Financial Officer starting August 25, 2025.

- While quarterly sales and net income saw modest declines from the previous year, the company's first-half results improved and its updated full-year revenue outlook provides important context for future performance.

- We'll examine how Sealed Air's updated financial guidance and new CFO appointment may influence its growth and margin improvement narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Sealed Air Investment Narrative Recap

To hold Sealed Air shares, investors need confidence that the company can realize longer-term margin and revenue improvements through sustainable packaging innovations and international expansion, despite current cyclical pressures. The latest quarterly results, modest year-over-year sales and earnings declines, a steady dividend, and reaffirmed full-year revenue guidance, suggest the recent news flow does not materially shift the near-term outlook. The most important short-term catalyst remains stabilization in packaging volumes, while persistent volume and margin pressures in the Food segment stand as the biggest risk right now.

Among recent announcements, the appointment of Kristen Actis-Grande as incoming CFO is most relevant. A change at the finance helm could help drive operational discipline as the business targets margin recovery and better capital allocation amidst ongoing input cost and volume headwinds. The leadership update, paired with unchanged financial guidance, puts even more focus on whether core end-market demand will recover as anticipated.

But investors should also be mindful that, in contrast, ongoing challenges in North American beef could prolong revenue headwinds if protein recovery stalls ...

Read the full narrative on Sealed Air (it's free!)

Sealed Air's outlook anticipates $5.7 billion in revenue and $538.6 million in earnings by 2028. Achieving this would mean a 2.4% annual revenue growth rate and a $239.2 million increase in earnings from the current $299.4 million.

Uncover how Sealed Air's forecasts yield a $39.14 fair value, a 31% upside to its current price.

Exploring Other Perspectives

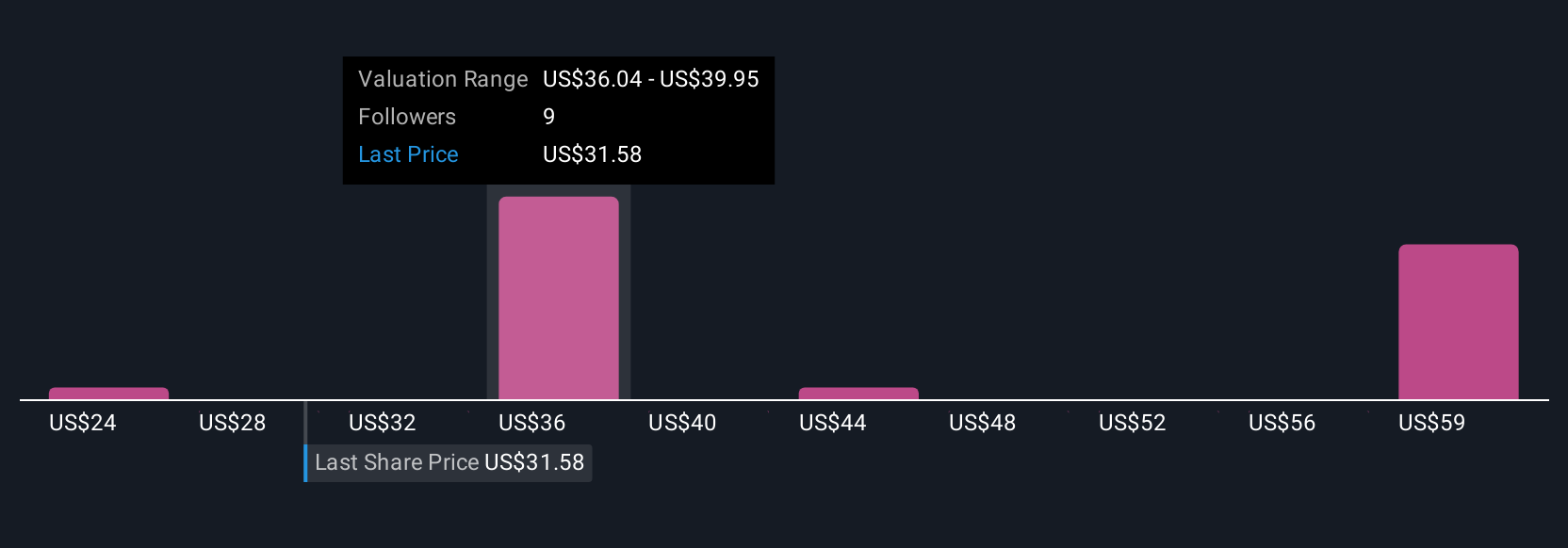

Four Simply Wall St Community members estimate Sealed Air’s fair value between US$24.33 and US$62.34 per share. While some anticipate the company’s sustainable packaging push to support growth, others highlight margin risk if the food segment weakness persists.

Explore 4 other fair value estimates on Sealed Air - why the stock might be worth 19% less than the current price!

Build Your Own Sealed Air Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Sealed Air research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Sealed Air research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sealed Air's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com