- Westlake Corporation recently announced a regular dividend of US$0.53 per share for the second quarter of 2025, payable on September 4 to shareholders of record as of August 19, while also reporting a net loss of US$142 million on sales of US$2.95 billion for the quarter ended June 30, 2025.

- Despite this quarterly loss and no share repurchases during the period, Westlake's Board continued its dividend distribution, underscoring management's commitment to returning capital to shareholders even amid earnings challenges.

- We'll examine how Westlake's shift from profit to quarterly net loss could reshape its investment outlook amid ongoing industry headwinds.

Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

Westlake Investment Narrative Recap

To be a shareholder in Westlake today, you need confidence in its ability to navigate industry headwinds, such as persistent oversupply and margin pressure, while leveraging trends in U.S. infrastructure spending and housing. The recent announcement of a maintained dividend, even as Westlake reported a quarterly net loss, does not materially change the importance of margin recovery as the key short-term catalyst or the risk posed by continued pricing pressure and global cost volatility.

Among the recent news, the Q2 earnings announcement stands out: Westlake shifted from a US$313 million profit to a US$142 million loss year-over-year, with sales and margins both declining. This underscores the challenge the company faces from shrinking profitability amidst ongoing industry weakness, placing even more emphasis on future cost-reduction efforts as a potential catalyst for earnings recovery.

Yet, despite dividends holding steady, investors should be watching closely for signs that industry overcapacity and weak pricing could...

Read the full narrative on Westlake (it's free!)

Westlake's outlook projects $13.5 billion in revenue and $1.1 billion in earnings by 2028. This relies on a 4.8% annual revenue growth rate and a $1.17 billion increase in earnings from a current loss of $70 million.

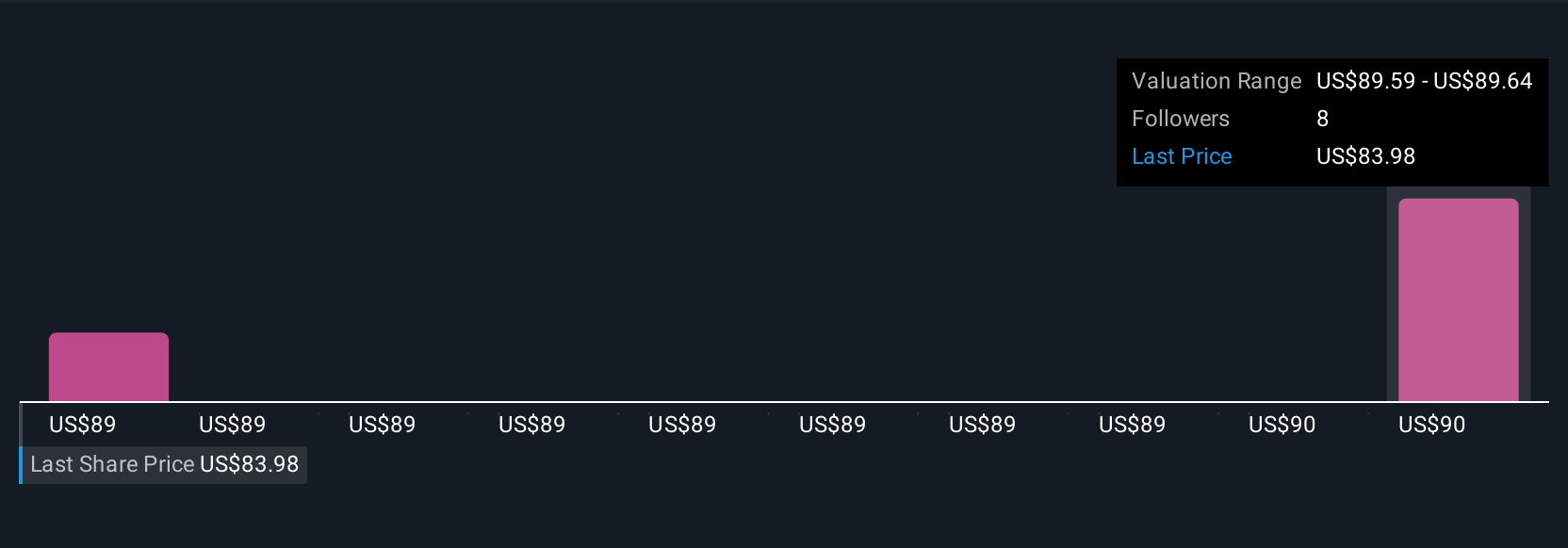

Uncover how Westlake's forecasts yield a $90.00 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community range from US$87.38 to US$90, reflecting different views on Westlake’s prospects. While some see long-term opportunity in U.S. infrastructure demand, the immediate challenge remains ongoing margin pressure from global oversupply, see how your expectations compare to these perspectives.

Explore 2 other fair value estimates on Westlake - why the stock might be worth as much as 14% more than the current price!

Build Your Own Westlake Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Westlake research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Westlake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westlake's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com