- Kiniksa Pharmaceuticals International recently announced its second quarter and first half 2025 results, reporting a sharp increase in revenue to US$156.8 million for the quarter and a turnaround to net income of US$17.83 million, alongside a new annual revenue forecast of US$625 million to US$640 million.

- This marked improvement in profitability and upwardly revised revenue guidance reflects management's increased confidence in demand trends and the company's operational execution in the evolving biopharmaceutical market.

- We'll explore how Kiniksa's return to profitability and raised 2025 revenue outlook may reshape its investment narrative in light of increasing ARCALYST adoption.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Kiniksa Pharmaceuticals International Investment Narrative Recap

To be a Kiniksa Pharmaceuticals shareholder today, you need to believe that continued ARCALYST adoption can drive both short- and long-term growth, with solid revenue expansion offsetting uncertainty from competition and payer dynamics. The company’s latest earnings surge and higher 2025 revenue forecast reinforce the near-term catalyst of broadening ARCALYST use, but heightened competitive threats from new therapies remain the core risk to watch, recent results do not fundamentally alter this risk profile.

The most relevant announcement to this outlook is Kiniksa's decision to raise its 2025 revenue guidance to a range of US$625 million to US$640 million, following another profitable quarter. This adjustment underscores management’s positive read on ARCALYST's growth trajectory and the potential for continued market share gains in recurrent pericarditis, though the pace and durability of these gains are still subject to competitive developments within the sector.

On the other hand, investors should keep in mind that the threat of new oral therapies entering the market could...

Read the full narrative on Kiniksa Pharmaceuticals International (it's free!)

Kiniksa Pharmaceuticals International's narrative projects $992.0 million in revenue and $188.6 million in earnings by 2028. This requires 23.3% yearly revenue growth and an earnings increase of $183.8 million from $4.8 million currently.

Uncover how Kiniksa Pharmaceuticals International's forecasts yield a $46.50 fair value, a 42% upside to its current price.

Exploring Other Perspectives

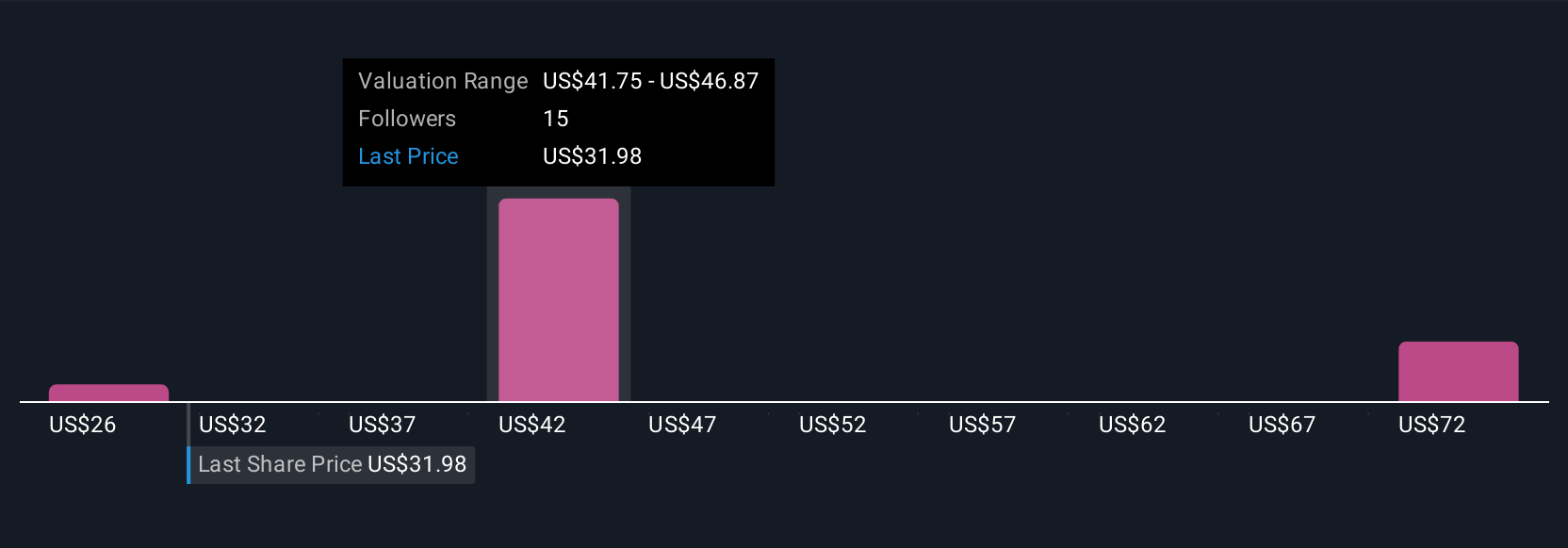

Simply Wall St Community members offer fair value estimates for Kiniksa Pharmaceuticals from US$26.39 up to US$88.64, based on four distinct perspectives. While enthusiasm for ARCALYST expansion is reflected in company forecasts, future competitive pressures could significantly impact these individual outlooks, explore a range of investor viewpoints to see how expectations compare.

Explore 4 other fair value estimates on Kiniksa Pharmaceuticals International - why the stock might be worth 19% less than the current price!

Build Your Own Kiniksa Pharmaceuticals International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kiniksa Pharmaceuticals International research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Kiniksa Pharmaceuticals International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kiniksa Pharmaceuticals International's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com