- Builders FirstSource recently reported its second quarter 2025 results, noting a decline in net sales to US$4,234.06 million and net income to US$185.03 million compared to the previous year, while also updating progress on its share repurchase program and providing full-year sales guidance.

- Alongside continued share buybacks, the company is actively seeking acquisitions despite ongoing challenges from weaker sales and lower profitability over the past two years.

- We’ll examine how persistent revenue and earnings declines, despite continued buybacks and M&A efforts, impact Builders FirstSource’s investment narrative.

Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

Builders FirstSource Investment Narrative Recap

Investors in Builders FirstSource need to believe that the company's long-term focus on digital transformation, operational efficiency, and industry consolidation will outweigh current headwinds from weak housing demand and falling earnings. The latest quarterly update, highlighting ongoing share buybacks and an acquisition appetite even as sales and profit continue to decline, does not materially alter the key near-term catalyst: stabilization in housing starts. The biggest risk remains exposure to single-family construction cycles and volatile commodity prices, which continue to pressure margins.

Of all recent announcements, the completion of over US$908 million in share repurchases stands out, as it underscores management’s commitment to shareholder returns despite a period of reduced profitability. However, with ongoing sales declines and earnings under pressure, these capital returns are most relevant in the context of whether underlying business momentum can recover meaningfully in the near term.

By contrast, investors should be aware of the elevated financial risk from high leverage and ongoing acquisition activity if core markets remain soft...

Read the full narrative on Builders FirstSource (it's free!)

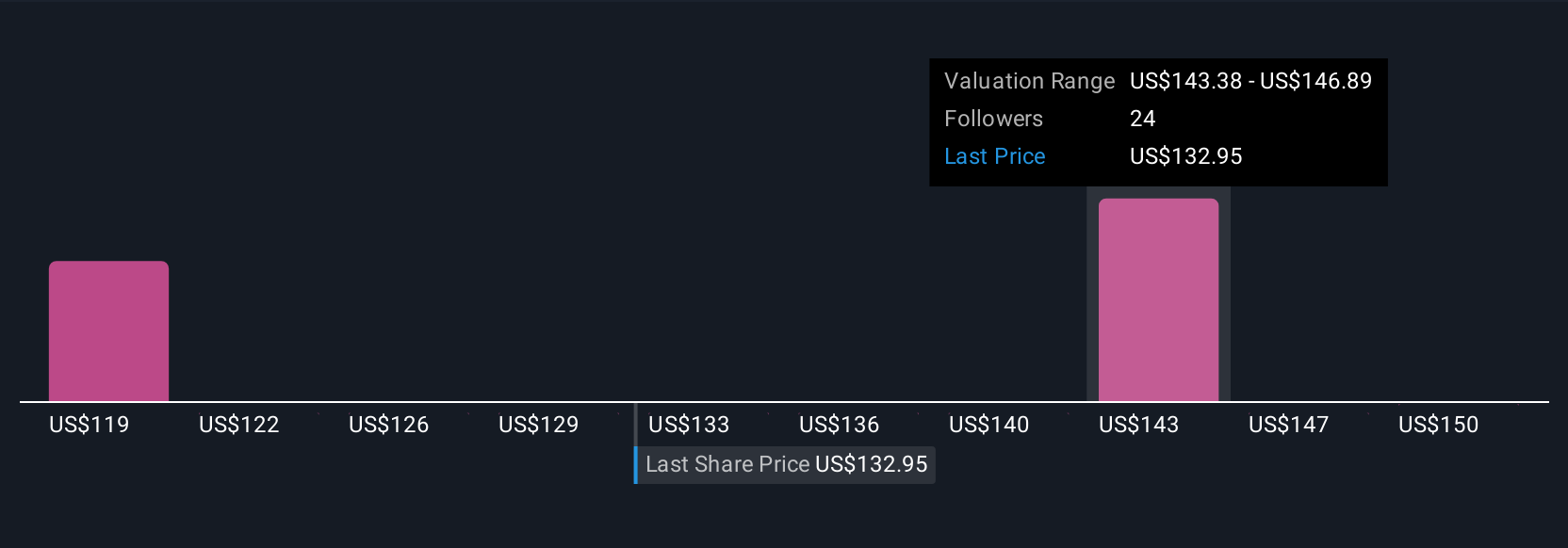

Builders FirstSource's outlook forecasts $16.4 billion in revenue and $684.5 million in earnings by 2028. This scenario assumes a 0.9% annual revenue decline and a $71.9 million decrease in earnings from current earnings of $756.4 million.

Uncover how Builders FirstSource's forecasts yield a $139.00 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community estimated fair values for Builders FirstSource stock in a wide range between US$119 and US$154. Many remain focused on the persistent softness in single-family housing, reminding you that outlooks can vary widely and merit further exploration.

Explore 3 other fair value estimates on Builders FirstSource - why the stock might be worth 10% less than the current price!

Build Your Own Builders FirstSource Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Builders FirstSource research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Builders FirstSource research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Builders FirstSource's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com