- Criteo reported its second quarter 2025 earnings, showing year-over-year sales growth to US$482.67 million despite a decline in quarterly net income, alongside announcing executive promotions and new partnerships, including with WPP Media to boost commerce intelligence on Connected TV.

- An important insight is that Criteo continued its aggressive share buyback, completing over a third of its program since 2021, while elevating leaders to accelerate AI-driven Retail and Performance Media initiatives in the evolving digital advertising landscape.

- We'll now consider how the WPP Media partnership to expand commerce intelligence for Connected TV could reshape Criteo's investment narrative.

The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Criteo Investment Narrative Recap

To be a Criteo shareholder, you need to believe in the company’s capacity to translate its data and AI innovations into sustained commercial value, even as digital ad markets shift toward Retail Media, Connected TV, and outcome-based advertising. The newly announced WPP Media partnership directly supports Criteo’s efforts to win incremental spend in fast-growing CTV, but it does not substantially alter the near-term need for top-line growth, still the most important catalyst, and client concentration risk, which remains one of the biggest concerns now.

Among recent announcements, Criteo’s decision to repurchase over a third of its shares since 2021 stands out, highlighting management’s focus on capital discipline and shareholder returns. However, this does not fully offset the potential drag from slow ramp-ups in new digital channels, which are critical to addressing stagnant client spending and future revenue growth.

Yet, investors should be mindful that despite these aggressive investments and partnerships, pressure from larger tech rivals with more extensive first-party data…

Read the full narrative on Criteo (it's free!)

Criteo's narrative projects $1.0 billion in revenue and $147.8 million in earnings by 2028. This requires a 19.2% annual revenue decline and a $11.3 million earnings increase from $136.5 million today.

Uncover how Criteo's forecasts yield a $38.17 fair value, a 59% upside to its current price.

Exploring Other Perspectives

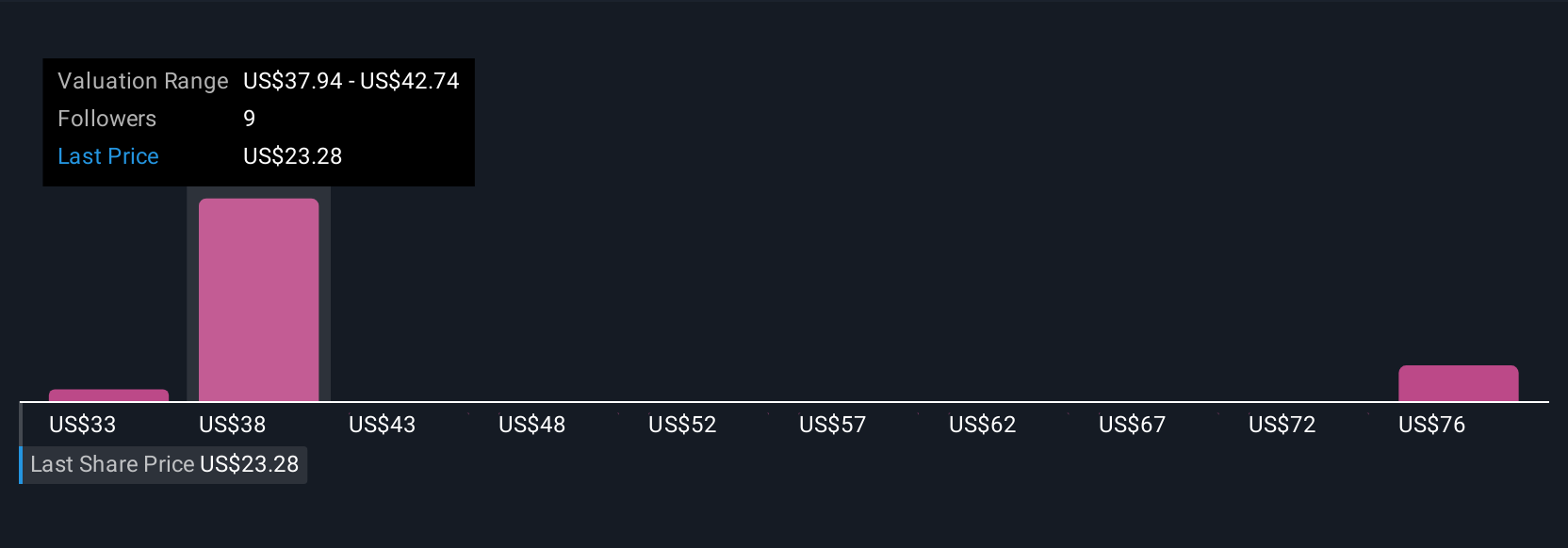

Community fair value estimates for Criteo range from US$33.14 to US$97.23 across three Simply Wall St Community perspectives, far above the recent share price. Many market participants are watching if Criteo’s efforts to accelerate growth in Retail Media and CTV can counteract concerns about client concentration and margin pressures, be sure to explore the full breadth of viewpoints on where the business could go next.

Explore 3 other fair value estimates on Criteo - why the stock might be worth just $33.14!

Build Your Own Criteo Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Criteo research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Criteo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Criteo's overall financial health at a glance.

No Opportunity In Criteo?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com