- Willis Towers Watson reported strong earnings for the second quarter of 2025, with net income rising to US$331 million on sales of US$2.26 billion and confirmed positive revenue guidance for the second half of the year, citing increased demand for compensation benchmarking and regulatory support.

- An important driver of future growth comes from services supporting clients' preparations for the EU Pay Transparency Directive, highlighting regulatory change as a catalyst for the company's evolving advisory offerings and revenue streams.

- We'll explore how strong quarterly earnings and anticipated regulatory-driven growth impact Willis Towers Watson's investment narrative moving forward.

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Willis Towers Watson Investment Narrative Recap

To be a shareholder of Willis Towers Watson, you need to believe in the company's ability to translate strong advisory demand, driven by regulatory change such as the EU Pay Transparency Directive, into sustainable growth. The recent earnings report confirms robust profitability, but with sales stable year-on-year, the most important short-term catalyst remains successful execution in regulatory-driven consulting, while the biggest risk continues to be margin pressure from rising compliance demands and industry competition. The impact of this quarter's results and outlook on those factors appears moderately favorable, signaling progress but not yet eliminating the core risks.

Of the recent announcements, the company's July 31 guidance update stands out for its relevance to these catalysts. Willis Towers Watson sees a lift in second-half 2025 revenue from seasonal surveys and client demand tied to new European pay transparency rules, sharpening the focus on its ability to monetize regulatory shifts and underscoring the importance of execution in this evolving area.

But against this backdrop, investors should also keep in mind the persistent challenge of fee compression from digital automation, especially as broader industry trends accelerate...

Read the full narrative on Willis Towers Watson (it's free!)

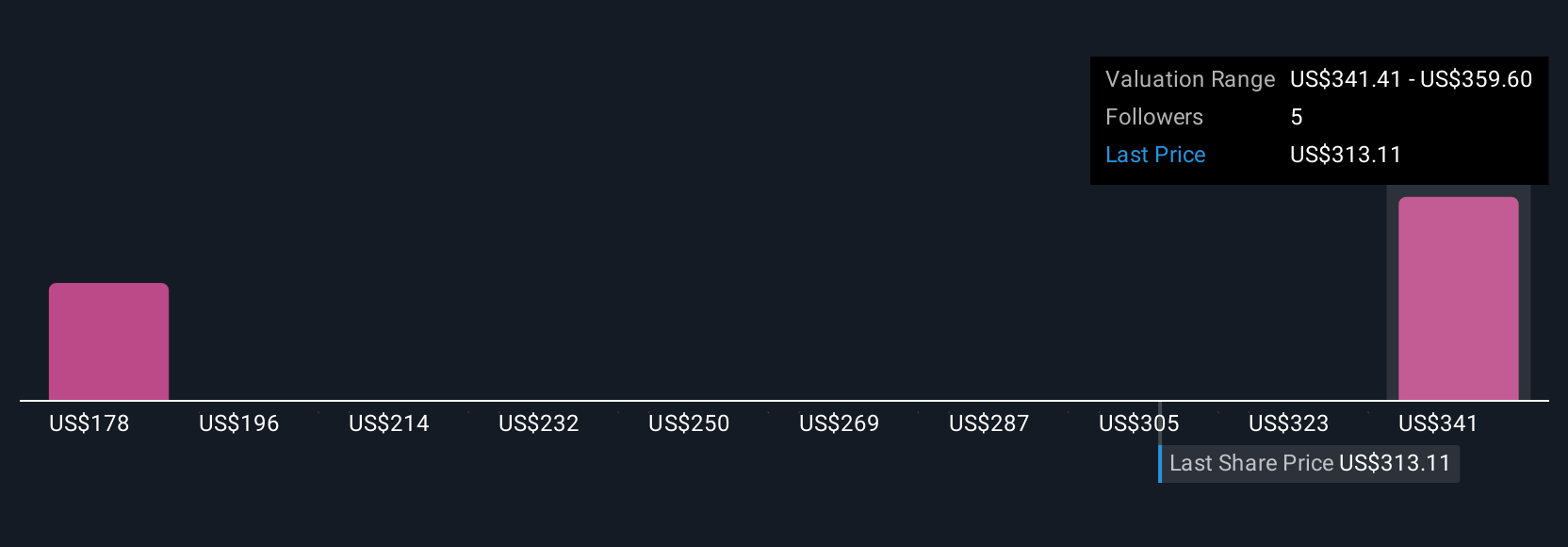

Willis Towers Watson's narrative projects $10.9 billion revenue and $2.8 billion earnings by 2028. This requires 3.5% annual revenue growth and a $2.66 billion increase in earnings from the current $137.0 million.

Uncover how Willis Towers Watson's forecasts yield a $364.06 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members submitted two fair value estimates for Willis Towers Watson, ranging widely from US$168.70 to US$364.06 per share. As regulatory-driven advisory demand grows, opinions on future profit resilience vary, so be sure to review a spectrum of viewpoints from the community.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth as much as 11% more than the current price!

Build Your Own Willis Towers Watson Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com