- CNO Financial Group recently declared a quarterly cash dividend of US$0.17 per share and completed a US$57.50 million shelf registration for a 1,600,000 share ESOP-related common stock offering, alongside reporting quarterly earnings and share repurchases.

- The company’s coordinated capital management activities, including dividends, repurchases, and equity offerings, reflect a multifaceted approach to returning value and managing growth.

- We will explore how CNO’s continued dividend payments highlight its shareholder return priorities and influence the broader investment outlook.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

CNO Financial Group Investment Narrative Recap

To own CNO Financial Group stock, an investor needs to be confident in the company’s ability to grow its insurance and annuity offerings, while steadily returning value to shareholders through dividends and share buybacks. The recent shelf registration filing and ESOP-related offering do not appear to impact the foremost near-term catalyst, which is accelerating digital direct-to-consumer growth, nor do they significantly affect the primary risks related to regulatory changes and interest rate pressures.

Among the latest announcements, CNO’s second quarter 2025 earnings release is particularly relevant, it showcased higher year-over-year revenue but lower net income and EPS. These results point toward the balancing act between supporting top-line expansion through digital sales momentum and managing margin compression, a key concern in a competitive market.

However, investors should also be aware that if regulatory or healthcare policy shifts intensify, requiring costly operational adjustments and increasing business model uncertainty, the company’s ability to...

Read the full narrative on CNO Financial Group (it's free!)

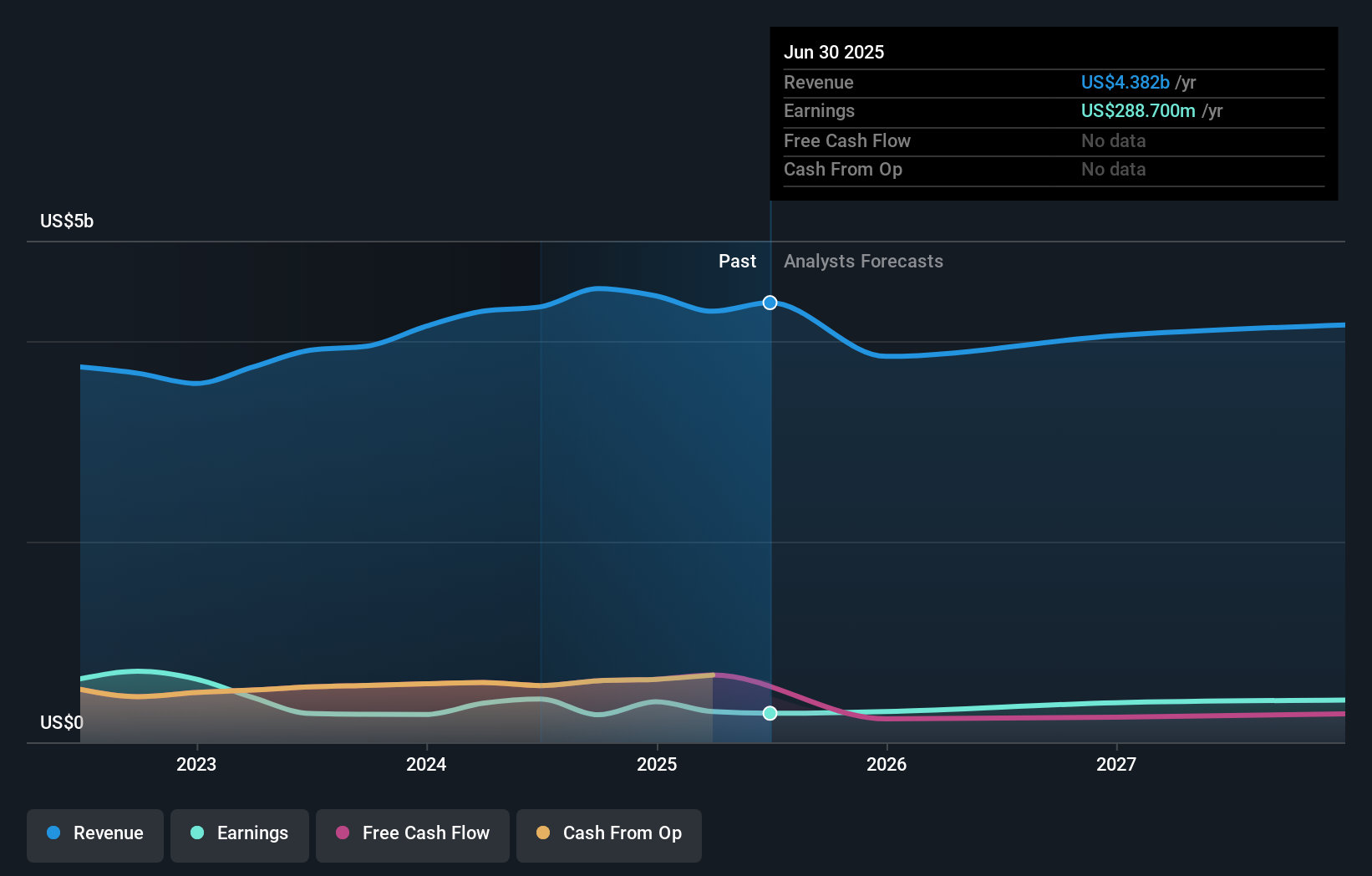

CNO Financial Group is projected to generate $4.3 billion in revenue and $435.2 million in earnings by 2028. This outlook incorporates an annual revenue decline of 0.8% and a $146.5 million increase in earnings from the current $288.7 million.

Uncover how CNO Financial Group's forecasts yield a $42.40 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members provided 1 estimate for CNO’s fair value, all at US$42.40 per share. While opinions may align on current valuation, intensifying competition in the annuities market could influence the company’s long-term revenue growth, so check out diverse perspectives before deciding.

Explore another fair value estimate on CNO Financial Group - why the stock might be worth as much as 16% more than the current price!

Build Your Own CNO Financial Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CNO Financial Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CNO Financial Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNO Financial Group's overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 26 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com