- CONMED Corporation recently declared a quarterly cash dividend of US$0.20 per share, payable on October 3, 2025, to shareholders of record as of September 15, 2025, and updated its guidance with raised full-year revenue forecasts and new expectations for the third quarter.

- These updates highlight the company's continued commitment to shareholder returns and reflect management's confidence amid recent analyst earnings estimate increases and strong positioning in minimally invasive surgical markets.

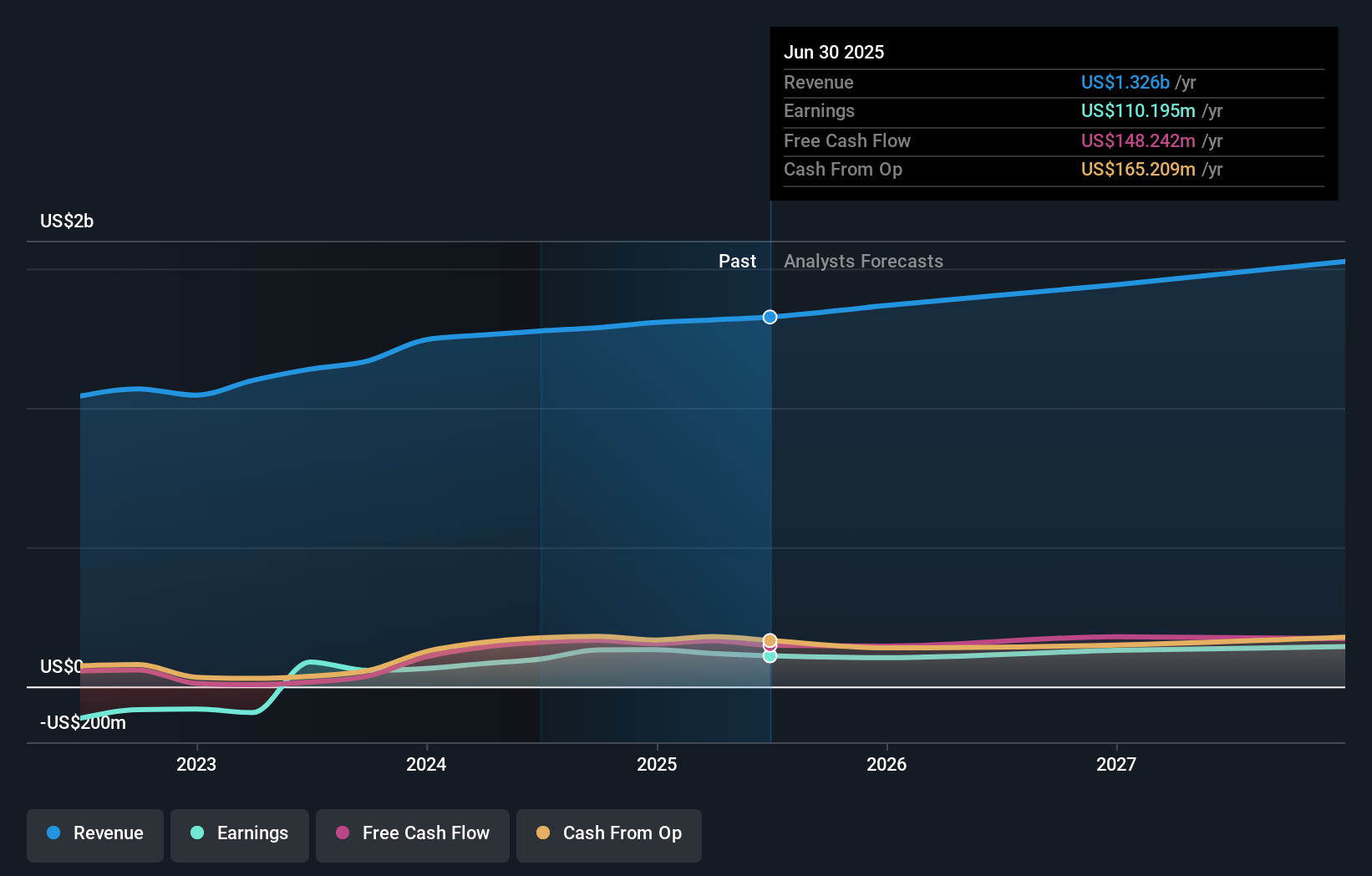

- We'll examine how the raised full-year revenue guidance signals confidence in CONMED's ongoing growth and updates the investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

CONMED Investment Narrative Recap

To be a CONMED shareholder, you need to believe in the ongoing adoption of minimally invasive and robotic-assisted surgeries and the company's positioning in this market. The recent dividend declaration and updated revenue guidance reinforce business confidence, but their direct impact on the main short-term catalyst, orthopedic supply chain recovery, remains limited, with supply challenges still representing the most important risk to watch.

The raised full-year 2025 revenue guidance is the most relevant recent announcement, reflecting slightly improved visibility into near-term sales amid FX tailwinds. However, the incremental revenue range increase is modest and does not materially shift the investment thesis or address lingering execution risks tied to cost discipline and hospital capital spending cycles.

By contrast, with orthopedic supply chain constraints still unresolved, investors should be aware that ...

Read the full narrative on CONMED (it's free!)

CONMED's narrative projects $1.6 billion revenue and $154.0 million earnings by 2028. This requires 5.7% yearly revenue growth and a $43.8 million earnings increase from $110.2 million today.

Uncover how CONMED's forecasts yield a $61.00 fair value, a 12% upside to its current price.

Exploring Other Perspectives

One member of the Simply Wall St Community set a fair value of US$61.00 for CONMED, showing a single viewpoint. Against modestly increased revenue guidance, opinions on future performance can vary widely, see how others in the Community weigh this risk and opportunity.

Explore another fair value estimate on CONMED - why the stock might be worth as much as 12% more than the current price!

Build Your Own CONMED Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CONMED research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CONMED research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CONMED's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 26 companies in the world exploring or producing it. Find the list for free.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com