- Grand Canyon Education reported second quarter 2025 earnings earlier this week, revealing net income of US$41.55 million, up from US$34.88 million last year, and raised its full-year service revenue and earnings per share outlook.

- The earnings beat and positive guidance were supported by a 10.3% increase in partner enrollments and operational improvements resulting from contract changes with university partners.

- We'll now examine how these record quarterly results and improved outlook influence Grand Canyon Education's investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Grand Canyon Education Investment Narrative Recap

To be a Grand Canyon Education shareholder, you need conviction in the company's ability to capitalize on online enrollment growth and operational efficiencies, while staying alert to student funding risks and evolving contract structures. The recent earnings beat and raised outlook reinforce the short-term catalyst of rising enrollments and margin expansion but do not materially address the risk of future federal funding changes, which still lingers as a key uncertainty for the business.

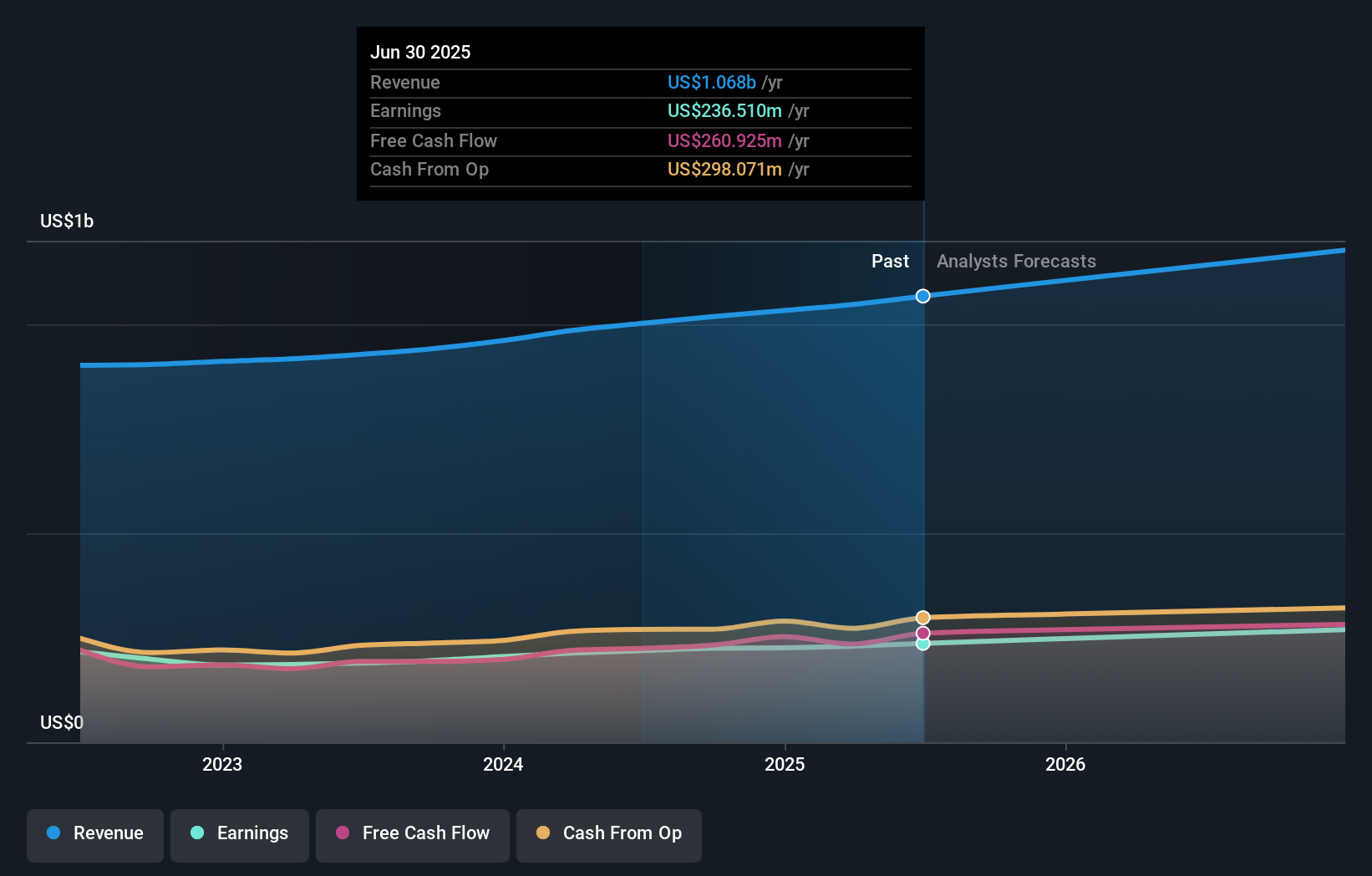

Among recent corporate developments, the company’s updated full-year 2025 guidance, calling for service revenue between US$1,100.3 million and US$1,107.3 million and diluted EPS of US$8.75 to US$8.90, is highly relevant given its alignment with improved enrollment trends and operational performance. This forecast supports the near-term bull case now that enrollment momentum and contract changes are producing tangible financial gains.

However, with improved guidance and short-term optimism, investors must still be aware that should federal student aid policy shift or campus enrollment soften, the next chapter could look very different...

Read the full narrative on Grand Canyon Education (it's free!)

Grand Canyon Education's outlook anticipates $1.3 billion in revenue and $280.4 million in earnings by 2028. This scenario requires 6.1% annual revenue growth and a $50.6 million increase in earnings from the current $229.8 million.

Uncover how Grand Canyon Education's forecasts yield a $213.33 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community estimates for Grand Canyon Education’s fair value span US$213 to US$265, based on 2 member forecasts. While momentum is building from higher enrollments and margin gains, views on the company’s value vary widely, take time to review alternative perspectives.

Explore 2 other fair value estimates on Grand Canyon Education - why the stock might be worth as much as 34% more than the current price!

Build Your Own Grand Canyon Education Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Grand Canyon Education research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Grand Canyon Education research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Grand Canyon Education's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 26 companies in the world exploring or producing it. Find the list for free.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com