- On August 7, 2025, FedEx's Board of Directors declared a quarterly cash dividend of $1.45 per share, payable on October 1, 2025, to shareholders of record as of September 8, 2025.

- This move reflects FedEx’s ongoing commitment to returning value to shareholders, even as the company pursues efficiency initiatives and explores a potential spin-off of its FedEx Freight unit.

- We will now examine how this dividend declaration, which highlights FedEx's financial discipline, shapes the company's longer-term investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 26 companies in the world exploring or producing it. Find the list for free.

FedEx Investment Narrative Recap

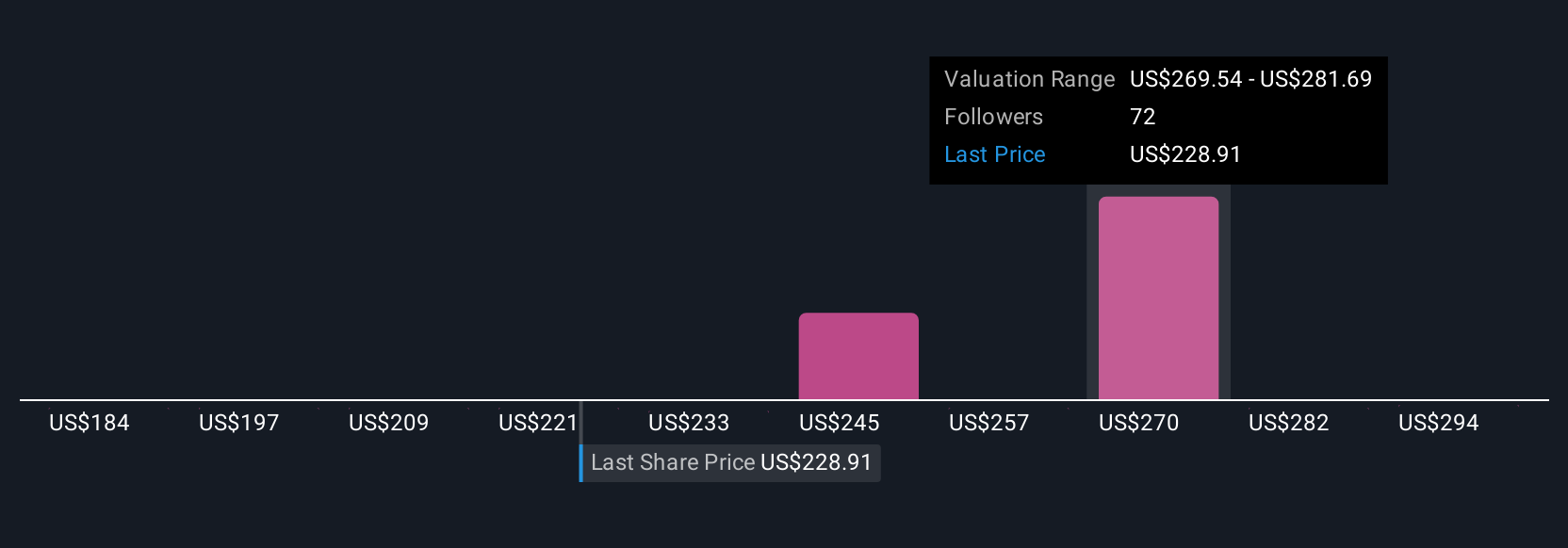

To be a FedEx shareholder, you need confidence in its ability to translate efficiency initiatives and e-commerce exposure into resilient earnings, despite industrial softness and freight market headwinds. The recent dividend declaration reinforces FedEx’s shareholder focus but does not significantly shift the biggest short-term catalyst: successful execution of cost-saving programs, or the key risk: volatility from freight restructuring and market pressures. For those tracking catalysts, the company’s recent share buyback program provides a relevant signal of financial discipline, capital allocation priorities, and confidence from management amid restructuring and market uncertainties.

In contrast, investors should be aware that FedEx’s restructuring of its Freight business may introduce additional costs and operational risks that...

Read the full narrative on FedEx (it's free!)

FedEx's narrative projects $95.3 billion revenue and $5.2 billion earnings by 2028. This requires 2.7% yearly revenue growth and a $1.1 billion earnings increase from $4.1 billion today.

Uncover how FedEx's forecasts yield a $266.40 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Nine Simply Wall St Community fair value estimates for FedEx range from US$231.87 to US$406.50 per share. These varied views reflect diverse growth assumptions, but ongoing cost-cutting and Freight unit changes may continue to shape performance outcomes, explore how your own outlook compares.

Explore 9 other fair value estimates on FedEx - why the stock might be worth as much as 78% more than the current price!

Build Your Own FedEx Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your FedEx research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free FedEx research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FedEx's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com