- Innospec announced in August 2025 that it had completed the repurchase of 123,878 shares for US$11.53 million under its March 2025 buyback plan, while also reporting second quarter sales of US$439.7 million and net income of US$23.5 million, both showing modest changes compared to the previous year.

- This combination of share buybacks and softer earnings results reflects a mixed picture of capital allocation and ongoing operational challenges within the business.

- With second quarter net income down from the prior year, we'll examine how the latest earnings update influences Innospec's investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

Innospec Investment Narrative Recap

To be a shareholder in Innospec, an investor needs to believe in the company’s ability to shift its portfolio toward higher-value, sustainable chemicals while maintaining strong operational discipline. The recent news of completed share buybacks alongside modest revenue growth and a dip in net income in the second quarter does not materially shift the investment narrative’s most important short-term catalyst: the margin recovery expected from operational efficiency initiatives. However, it reaffirms the persistent risk that sustained margin compression in Performance Chemicals could challenge future earnings consistency if raw material costs persistently outpace price increases.

Among recent announcements, the company’s March 2025 buyback program, which resulted in the repurchase of 123,878 shares by the end of June 2025, stands out given its timing amid softening profits. While the buybacks may indicate confidence in long-term value creation, the greater immediate focus remains the effectiveness of ongoing initiatives to improve operational margins, given the current headwinds affecting earnings and segment profitability.

By contrast, investors should be aware of the ongoing volatility in raw material costs and the challenge of passing through price increases to customers, as this factor...

Read the full narrative on Innospec (it's free!)

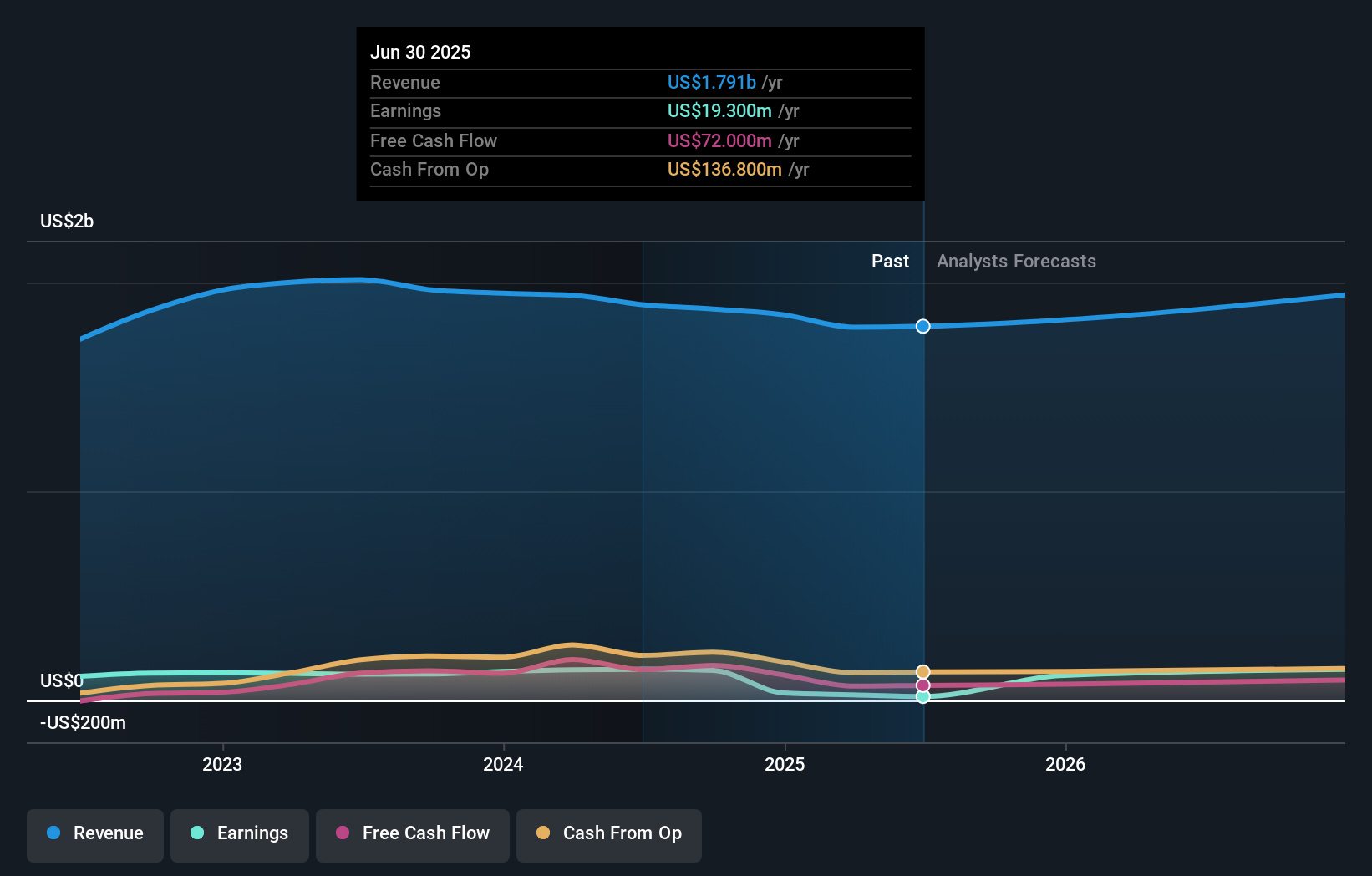

Innospec's outlook anticipates $2.1 billion in revenue and $447.4 million in earnings by 2028. This is based on a 5.4% annual revenue growth rate and a $428.1 million increase in earnings from the current $19.3 million.

Uncover how Innospec's forecasts yield a $115.00 fair value, a 44% upside to its current price.

Exploring Other Perspectives

One US$59.46 fair value estimate from the Simply Wall St Community reveals a singular view, yet hints at potential overvaluation given recent earnings trends. Investors may want to weigh this against the ongoing risk of margin compression when considering various viewpoints about Innospec’s outlook.

Explore another fair value estimate on Innospec - why the stock might be worth 25% less than the current price!

Build Your Own Innospec Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Innospec research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Innospec research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Innospec's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 18 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com