- Interparfums, Inc. recently announced its second quarter results, posting sales of US$333.94 million and net income of US$31.99 million, both decreasing from the same period last year, alongside a regular quarterly dividend declaration and reaffirmed full-year guidance for 2025.

- Despite the year-over-year earnings dip, management's decision to maintain its sales and earnings outlook for 2025 signals confidence in its operational trajectory and future prospects.

- We'll explore how Interparfums' reaffirmed guidance and steady dividend policy influence its long-term growth thesis and risk profile.

AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Interparfums Investment Narrative Recap

To be a shareholder in Interparfums, you need to believe in its ability to leverage a portfolio of prestigious fragrance licenses and digital expansion efforts to deliver steady, long-term growth despite licensing concentration and consumer trends toward sustainability. The recent dip in second-quarter earnings was largely anticipated and, with management reaffirming its full-year guidance, doesn't materially affect expectations for key upcoming product launches or the central risk stemming from license partner dynamics.

The most relevant announcement is the reaffirmed 2025 guidance, with management expecting net sales of US$1.51 billion and earnings per diluted share of US$5.35, which underscores continued confidence in the company's ability to drive growth through brand launches and expansion into higher-margin digital channels. This steady outlook, despite temporary headwinds, will be closely watched in the context of ongoing innovations and channel shifts across the global fragrance sector.

Yet, investors should be aware that despite this optimism, any disruption to a major licensing agreement could change the outlook significantly...

Read the full narrative on Interparfums (it's free!)

Interparfums' outlook anticipates $1.7 billion in revenue and $205.0 million in earnings by 2028. This reflects an annual revenue growth rate of 4.9% and a $44.0 million increase in earnings from the current $161.0 million.

Uncover how Interparfums' forecasts yield a $163.33 fair value, a 35% upside to its current price.

Exploring Other Perspectives

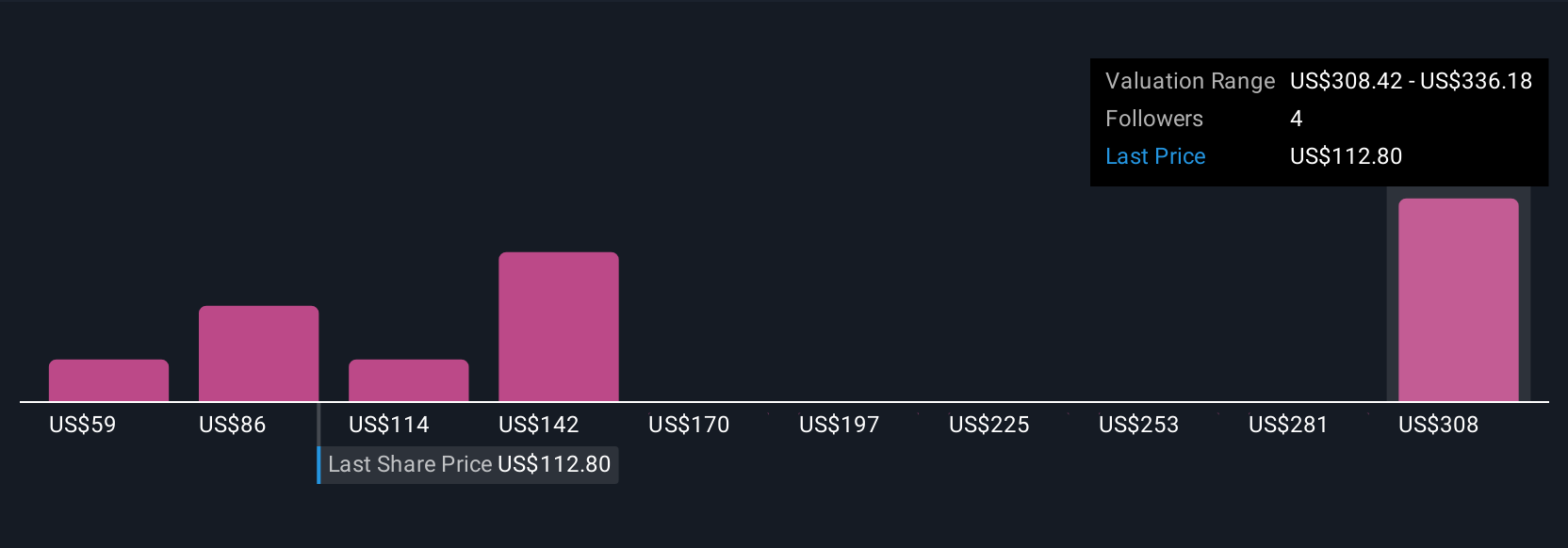

Six members of the Simply Wall St Community estimate Interparfums’ fair value between US$58.55 and US$339.37. While opinions vary, keep in mind that earnings remain reliant on key brand licenses, which could affect results as market conditions shift.

Explore 6 other fair value estimates on Interparfums - why the stock might be worth less than half the current price!

Build Your Own Interparfums Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Interparfums research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Interparfums research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Interparfums' overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com