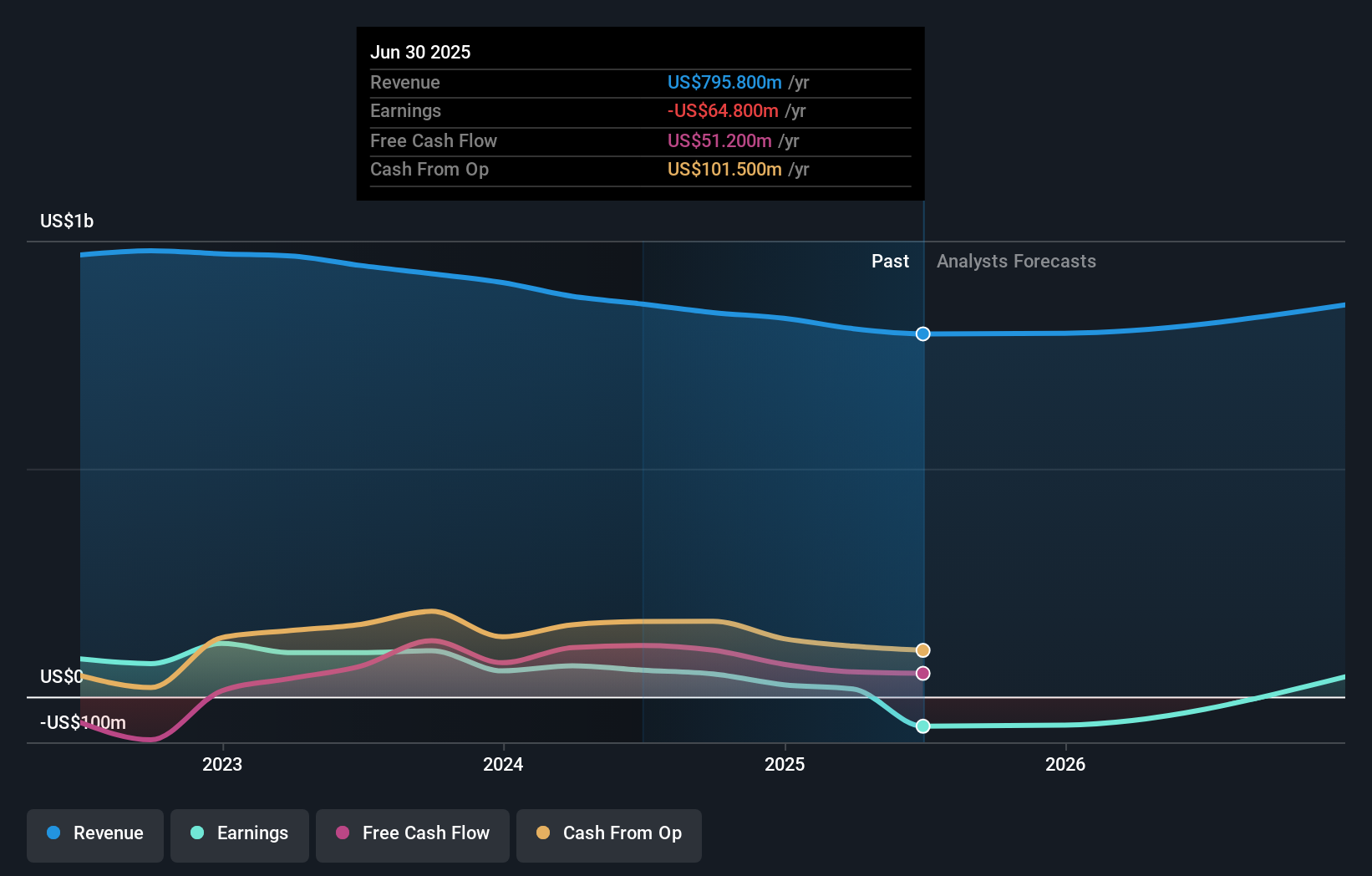

- Rogers Corporation recently reported lower second quarter earnings, with sales of US$202.8 million and a net loss of US$73.6 million compared to a profit a year earlier, and issued cautious third-quarter guidance expecting net sales between US$200 million and US$215 million and diluted earnings per share between US$0.00 and US$0.40.

- This combination of weaker results and modest guidance highlights ongoing operational and financial pressures for the company amidst a challenging market backdrop.

- We'll examine how Rogers Corporation's cautious forward guidance may influence the outlook for its earnings growth narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Rogers Investment Narrative Recap

To confidently hold Rogers stock, an investor needs to believe in the company’s ability to reverse recent losses and reignite growth through supply chain localization, pipeline expansion in China, and cost optimization. The latest weak earnings and cautious outlook may limit near-term optimism, shining a spotlight on gross margin challenges as the top short-term risk, while progress on China expansion remains the most important catalyst; the impact of recent results is material to both.

Among recent announcements, the appointment of Ali El-Haj as interim CEO stands out following the latest earnings report, as leadership transition during a period of pressure could influence both execution of cost reductions and progress with new business opportunities in China, two key factors in restoring confidence in the company’s growth narrative.

However, despite optimism around future catalysts, investors should be aware that persistent gross margin weakness could...

Read the full narrative on Rogers (it's free!)

Rogers' narrative projects $865.7 million revenue and $83.6 million earnings by 2028. This requires 2.4% yearly revenue growth and a $66.7 million earnings increase from $16.9 million today.

Uncover how Rogers' forecasts yield a $82.50 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Fair value estimates for Rogers from two members of the Simply Wall St Community span from US$58.39 to US$82.50. While investors weigh this broad range, the company’s ongoing gross margin pressure may continue to shape expectations for future profitability and risk, explore these varied perspectives to better understand the full story.

Explore 2 other fair value estimates on Rogers - why the stock might be worth 13% less than the current price!

Build Your Own Rogers Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- Our free Rogers research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Rogers' overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com