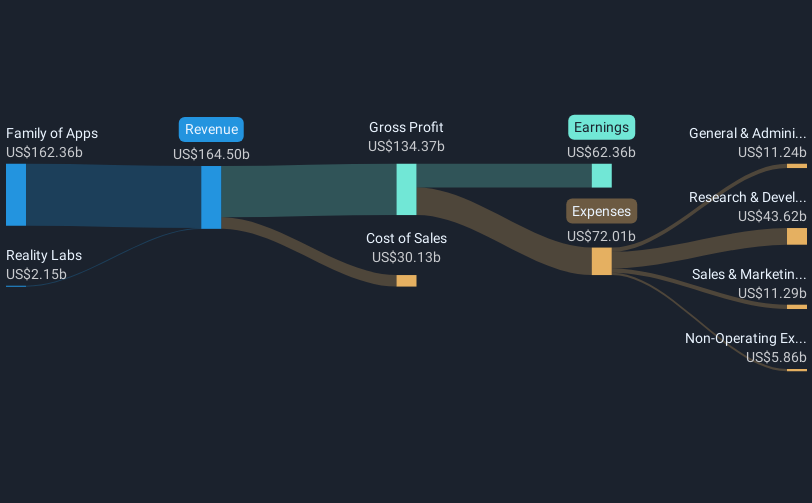

Meta Platforms (NasdaqGS:META) recently collaborated with Adapture Renewables on solar projects and integrated Threads API with Innovid, highlighting sustainability and marketing advancements. These strategic moves align with Meta’s commitment to renewable energy and technological innovation, supporting its stock's impressive 18% rise over the last quarter. The company’s strong Q1 earnings, with a significant rise in sales and net income, also played a crucial role. Though the market itself grew 12% over the past year, Meta's advances in AI, data centers, and energy partnerships reinforced its resilience and potential for long-term growth.

You should learn about the 1 weakness we've spotted with Meta Platforms.

The recent collaborations with Adapture Renewables and integration of Threads API with Innovid mark Meta Platforms' continued emphasis on sustainability and technological innovation. These initiatives could bolster Meta's narrative of expanding digital engagement through AI-driven advertising and business messaging improvements. By leveraging AI advancements, Meta aims to enhance ad targeting efficiency and user interaction, potentially driving revenue growth and aligning with the forecasted increase of US$244.1 billion in future revenue. The focus on AI could counteract any potential revenue declines from operational challenges in Europe and streamline profit margins, which analysts predict may decrease slightly over the next three years.

Over the longer-term period, Meta's total shareholder return, including share price appreciation and dividends, was 334.65% over three years, reflecting its strong performance in the market. Over the past year, Meta's stock outperformed the US Interactive Media and Services industry, which registered an 8.6% return, and the broader market's 12% growth. Analysts have set a median price target of US$721.43 for Meta, just 1.3% above its current price of US$712.20, suggesting the stock is viewed as fairly priced on average.

The company's collaborations and AI integration could influence revenue and earnings forecasts. Analysts project earnings of US$85.9 billion by June 2028, with a slight decrease in profit margins to 35.2%. However, the anticipated PE ratio of 25.8x by 2028 exceeds the industry average, which could impact investor sentiment. Potential fluctuations in AI development costs and compliance modifications in Europe might affect cash flows, but the initiatives in AI stand to significantly expand Meta’s market presence and drive future growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com