David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Albertsons Companies, Inc. (NYSE:ACI) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

How Much Debt Does Albertsons Companies Carry?

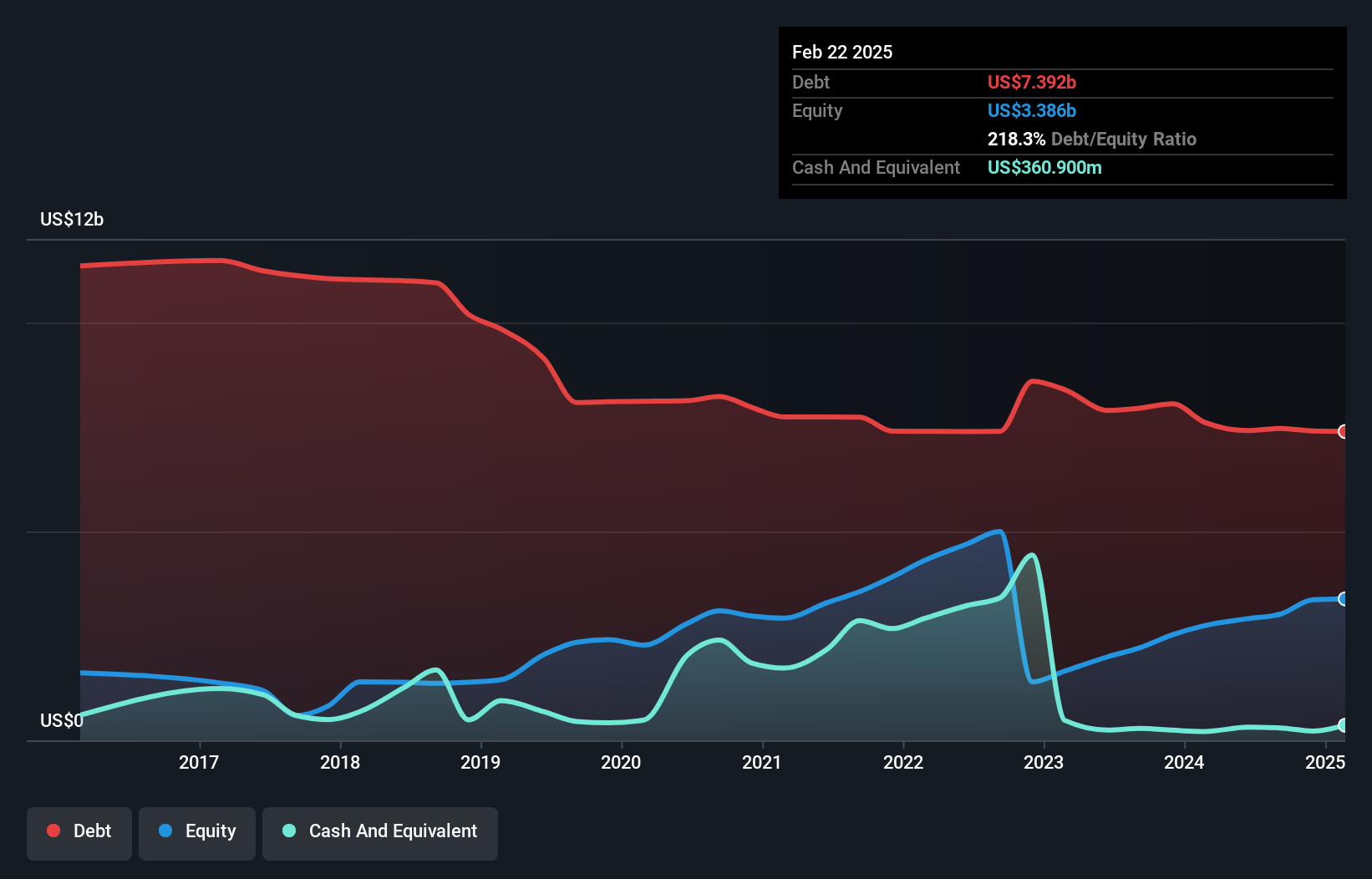

The chart below, which you can click on for greater detail, shows that Albertsons Companies had US$7.39b in debt in February 2025; about the same as the year before. On the flip side, it has US$360.9m in cash leading to net debt of about US$7.03b.

A Look At Albertsons Companies' Liabilities

We can see from the most recent balance sheet that Albertsons Companies had liabilities of US$7.25b falling due within a year, and liabilities of US$16.1b due beyond that. On the other hand, it had cash of US$360.9m and US$834.8m worth of receivables due within a year. So it has liabilities totalling US$22.2b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$12.2b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Albertsons Companies would probably need a major re-capitalization if its creditors were to demand repayment.

See our latest analysis for Albertsons Companies

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Albertsons Companies's net debt is sitting at a very reasonable 1.9 times its EBITDA, while its EBIT covered its interest expense just 4.4 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. The bad news is that Albertsons Companies saw its EBIT decline by 15% over the last year. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Albertsons Companies can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent three years, Albertsons Companies recorded free cash flow of 31% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

Mulling over Albertsons Companies's attempt at staying on top of its total liabilities, we're certainly not enthusiastic. But at least its net debt to EBITDA is not so bad. After considering the datapoints discussed, we think Albertsons Companies has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Albertsons Companies you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.